New highs for the Nasdaq 100: Intel–Nvidia deal lights the fuse

The Nasdaq 100 breaks to new highs as technology stocks celebrate the Fed's commitment to lower rates and Nvidia's investment in Intel

The Nasdaq 100 has hit a new high this week after what seemed like a dragged-out climb to reach the previous high just below the 24,000 level. The momentum has been classic one-two punch of AI/chip strength plus easier Fed policy.

First, the mega cap tech bid never really left: chipmakers and AI infrastructure names have been the key drivers of market strength, and it intensified after Nvidia said it will invest $5B in Intel, igniting a broad semiconductor rally. That single headline has helped push the Nasdaq to fresh records as it reinforced the market’s core narrative that AI capex isn’t slowing—it's broadening into new CPU+GPU designs and PC refresh cycles. In other words, the deal signalled more monetizable product roadmaps ahead, which is a key part of what pushes a growth-heavy index to new highs.

Intel corporation (INTC) daily chart

Past performance is not a reliable indicator of future results.

Furthermore, the collaboration also eases a key investor worry—supply and platform concentration. Nvidia is pairing its own platforms with Intel’s x86 and custom silicon, while still relying on TSMC for manufacturing of some parts, so the takeaway is that this is a capacity plus product expansion rather than a zero-sum shift.

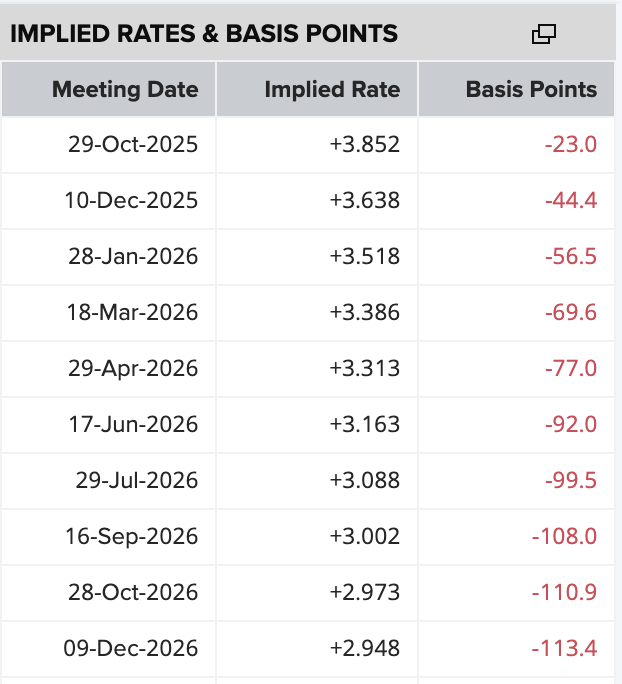

Second, policy and macro have turned from headwind to tailwind. The Fed’s 25 bp cut and hints it could ease again gave equities cover, even as Powell avoided an ultra-dovish script. Lower expected policy rates—paired with evidence of a cooling labour market—supported multiples and the long-duration growth trade, allowing stocks to print additional record highs after the meeting. This is partly because markets expect the new Fed governor that will replace Jerome Powell next year will be significantly more dovish, as evidenced by Stephen Miran’s dissent to vote for a 50bps cut at this week’s meeting. So, stocks did wobble on Wednesday as the outlook was less dovish than priced in, but there are hopes that the course will be corrected in the post-Powell era.

Source: refinitiv

Source: refinitiv

However, the move goes beyond the Nasdaq 100, with the broader US stock market printing new highs. The Fed’s 25 bp cut and the acknowledgement it will most likely ease again lowered the hurdle for risk. This saw the major indexes print fresh intraday records, while the Russell 2000 jumped as lower expected policy rates helped the domestic, rate-sensitive cohort, even in a seasonally tricky September. Breadth also seems to have improved, which takes some pressure off the too narrow/concentration narrative that has limited some of the upside in recent months.

So, all in all, easier policy, softer labour signals and calmer financial conditions have given the rally a wider base than just the mega-caps. Near-term, the same drivers will matter: the path of rates, bond yields, and whether AI spending headlines keep flowing into actual orders and earnings beats.