Market volatility lifts on US growth fears heading into February Non-Farm Payrolls data

Market uncertainty grows as US economic data signals a slowdown ahead of February’s Non-Farm Payrolls report.

The markets head into the February Non-Farm Payrolls release with palpable nervousness about the US economic outlook. Recent economic figures have shown a moderation in economic activity, with forward looking data suggesting looming downside risks stemming from US trade policy and, to a lesser extent, lay-offs and spending cuts linked to the so-called Department of Government Efficiency. A spate of consumer confidence surveys have revealed a drop in household sentiment due to the Trump administration’s policy agenda, with there already signs the uncertainty is crimping consumer spending. Meanwhile, business activity surveys have shown an emerging weakness in demand with corporates pulling back on employment and new orders. Importers are also trying to get ahead of potential tariffs by forward buying products, with the subsequent deepening of the trade deficit mechanically weakening future GDP estimates.

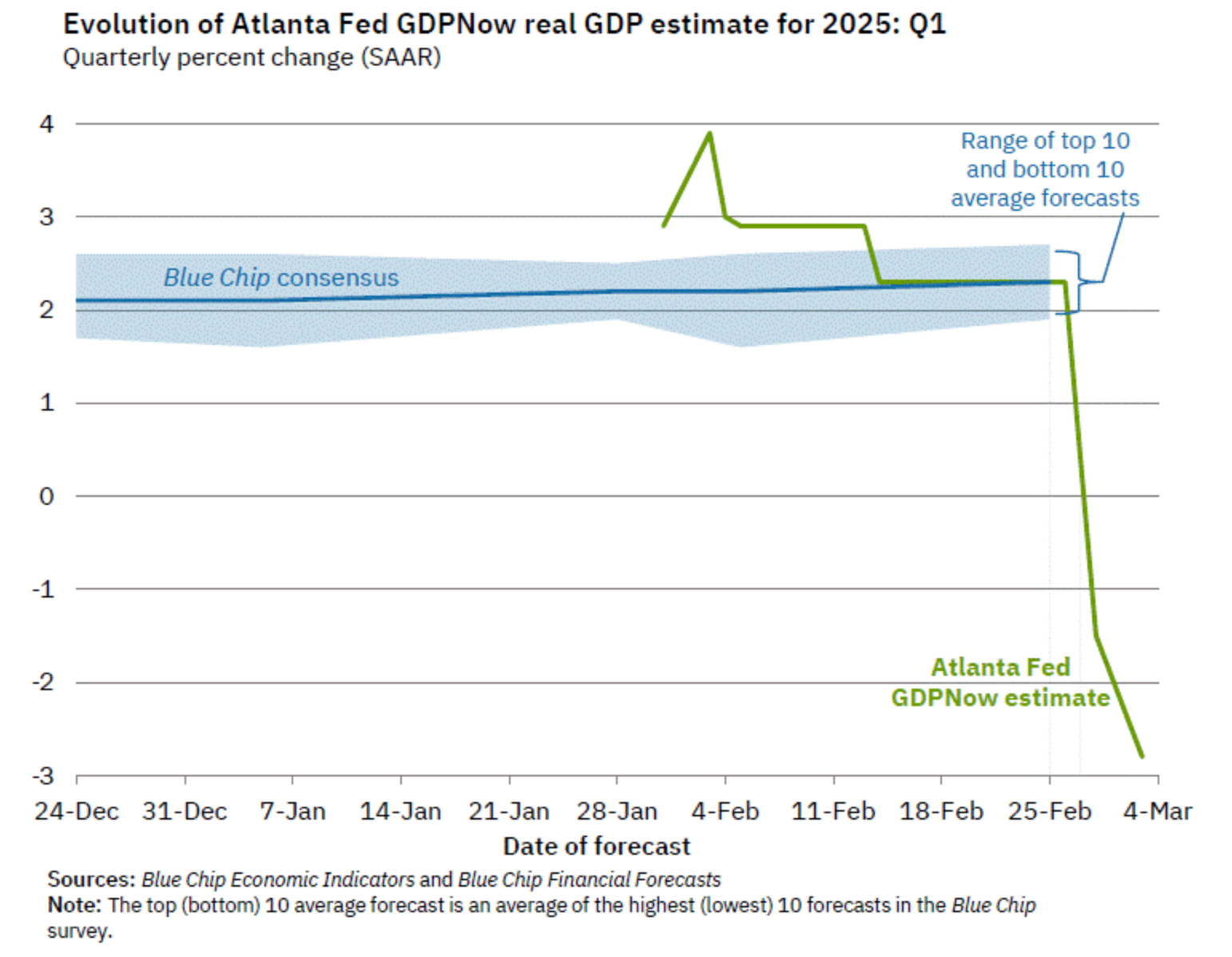

The merging storm clouds over the US economy is drawing people’s attention to the Atlanta Fed’s GDP Nowcast – a model projecting the annualised US growth rate for the quarter. The measure is pointing to a precipitous decline in US economic activity, plunging to -2.8%. While partially due to nominal drivers of a big increase in the trade deficit – greater imports over exports contracts from GDP growth – a significant portion of the decline is because of growing signs of flat consumer spending and business spending growth in Q1.

(Source: Atlanta Fed)

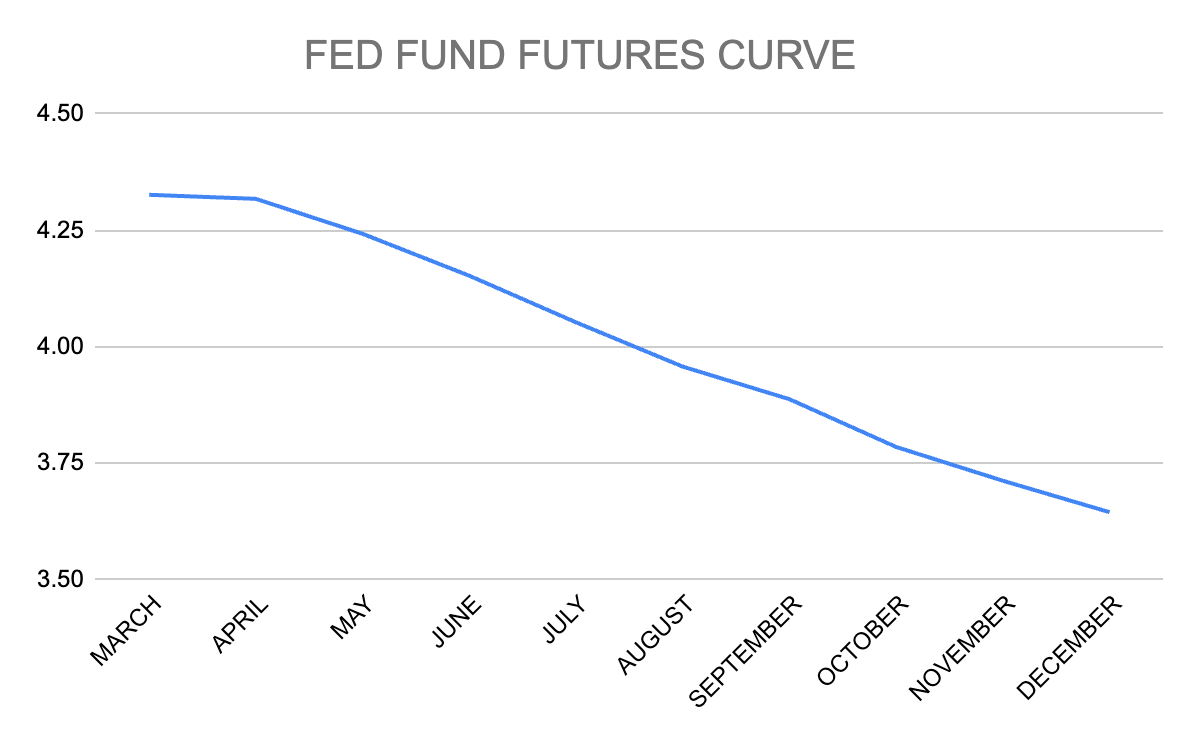

The Non-Farm Payroll data isn’t expected to capture this looming economic slowdown and there remains speculation about when DOGE related job losses will begin to manifest in the official data. The consensus estimate amongst economists suggests the US economy added 160,000 jobs in February, with the unemployment rate holding steady at 4.0%. Meanwhile, annual average hourly earnings growth is forecast to hold at a relatively elevated 4.1%. In total, such figures would reinforce the view of a resilient if not robust labour market that does not require the immediate support of further rate cuts from the US Federal Reserve. The timing of the next rate cut from the US Federal Reserve has been brought forward to the middle of the year following the recent spate of weaker than expected US data.

(Source: CME Group, Capital.com)

US Dollar drops as US economic exceptionalism diminishes

The US Dollar has receded from its highs primarily due to fears about the impact US trade policy and cuts to the public sector will have on domestic economic activity and subsequently US Federal Reserve interest rate policy. A stronger Euro has compounded the dynamic, which has emerged indirectly as a response to Trump foreign policy, with the European Union and its member states flagging greater spending on defense as it looks to offset reduced military support from the US.

The USD/JPY remains an interest rate differential play as the markets price-in further hikes from the Bank of Japan and looming cuts from the US Federal Reserve. The pair is currently range trading between 148.60 and 151. A break above the latter, which is also converging with the pair’s 20-day MA, could herald a further push towards downward sloping trendline resistance. Meanwhile, a breakthrough the former could see its downtrend extend.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)