Market analysis: US CPI and PPI

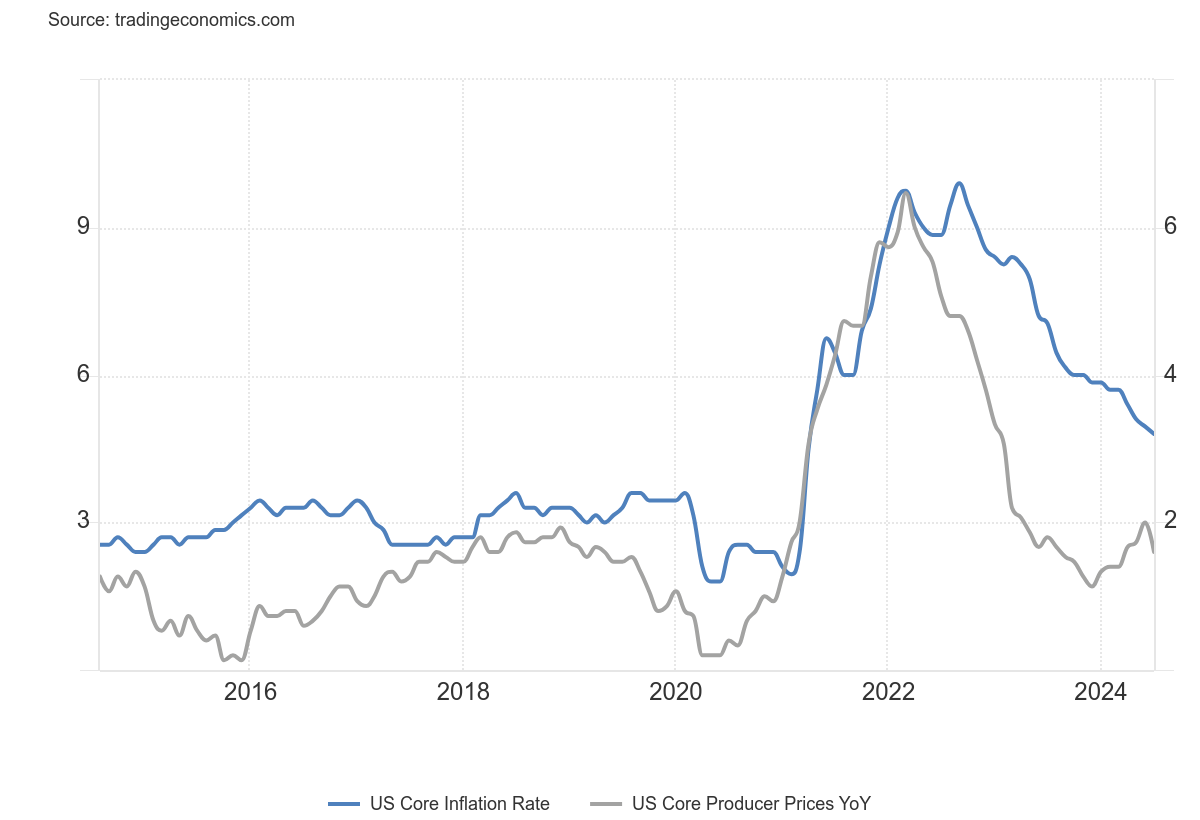

Overview of upcoming US inflation data for August, with expectations for a year-over-year CPI drop to 2.6% and core CPI holding steady at 3.2%. Markets will also focus on U.S. PPI data, which is forecasted to show mild growth, reinforcing potential easing inflationary pressures.

As we head into the critical US CPI release this week, the market narrative has shifted from upside risks to inflation to downside risks for the US labour market. On Wednesday, we’ll get fresh inflation data for August, with the consensus expecting a year-over-year headline CPI to ease to 2.6%, down from July’s 2.9%. Core inflation is expected to remain relatively sticky, holding steady at 3.2% year-over-year. The month-over-month figures will also be closely scrutinised, with both headline and core CPI forecast to rise by 0.2%. This would be in line with July’s data and signal that inflation may be stabilising at higher levels than the Fed is comfortable with.

Meanwhile, the U.S. Producer Price Index (PPI) data for August is set to be released on Thursday. Markets are expecting producer prices to reflect moderate growth, with forecasts suggesting a year-over-year increase of around 1.8% to 2.0%. This would mark a continuation of the subdued inflationary pressure in the pipeline, with the month-over-month PPI likely to come in at 0.2%, consistent with prior months. A mild PPI print could reinforce the notion that inflationary pressures are easing across the supply chain, which might support the Federal Reserve's gradual shift towards more accommodative monetary policy.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)

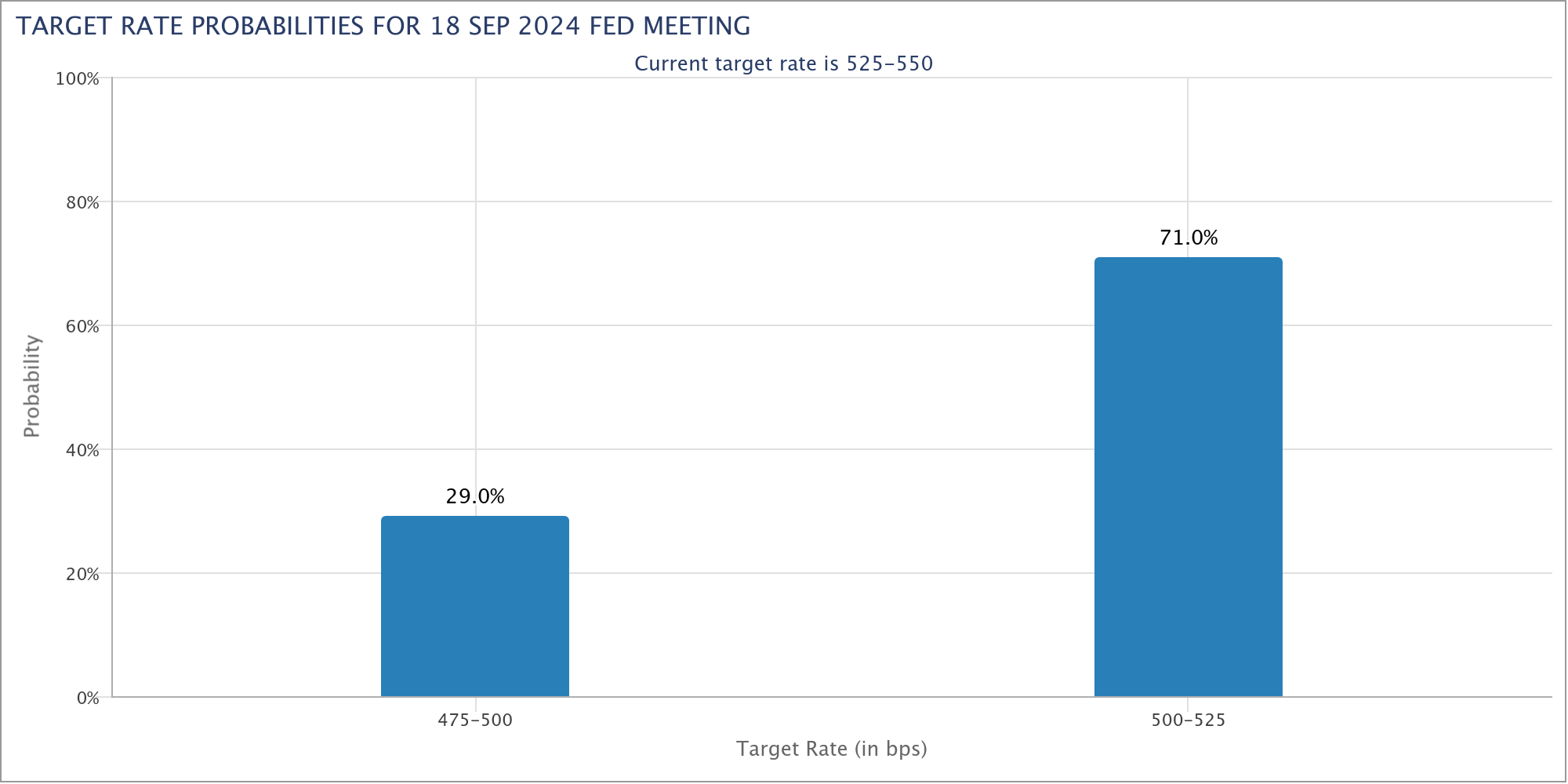

For the markets, the price data is expected to be a formality, providing the US Federal Reserve the last confirmation that it can lower interest rates when it meets on the 18th of September. However, there are two-way risks to interest expectations depending on an upside or downside surprise in price pressures. Amid fears of a softening labour market, a significant (and therefore unlikely) jump in CPI could cast doubt over the Fed’s ability to cut interest rates aggressively to stave-off a downturn. Alternatively, a major downside surprise could stoke concern of an unfolding demand shock in the US economy.

After last week’s Non-Farm Payrolls data, the implied probabilities of what the Fed is likely to do with policy in a few weeks time shifted aggressively towards a 50 basis point cut. Fed Fund Futures imply a 70% chance of a “jumbo” move and there’s more than 100 basis points of cuts priced into the curve before the end of the year. Given the focus on labour market conditions, the inflation data may be less of a driver of market volatility than it has been in the past.

(Source: CME Group)

Amidst fears of a potential US recession and a subsequent tightening of global financial conditions, the US Dollar has rallied across the G10 currency complex. As a proxy for global growth, the AUD/USD has turned lower after rejecting critical resistance at 0.6800 to renew its primary downtrend. The 200-day moving average looms as a critical level of technical support.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)