June US Non-Farm Payrolls data tipped to show lift in jobless rate

The US unemployment rate tipped to rise as labour market softens

With geopolitical risks easing and equities climbing to record highs, investor attention now turns to the US labour market. June 2025’s non-farm payrolls report, due Thursday due to the July 4 holiday, could prove pivotal in shaping expectations for interest rate cuts later this year—particularly as the Federal Reserve balances a still-warm inflation backdrop with signs of softening job growth.

Resilient but softening: Jobs growth expected to slow

The US labour market has shown remarkable resilience over the past year, recent prints suggest momentum may be cooling. Markets are bracing for a moderate increase in payrolls in the low 100,000s and an unemployment rate ticking up to 4.3%. That would represent a continued softening from the strong start to 2025, when the “US exceptionalism” trade was in full swing.

The expected figures are not recessionary by any stretch, but they would signal that some slack is returning to the labour market. For the Fed, this may reinforce the argument for adjusting policy to support employment—even as inflation remains above target.

Fed flexibility: Markets bet on a cut despite sticky inflation

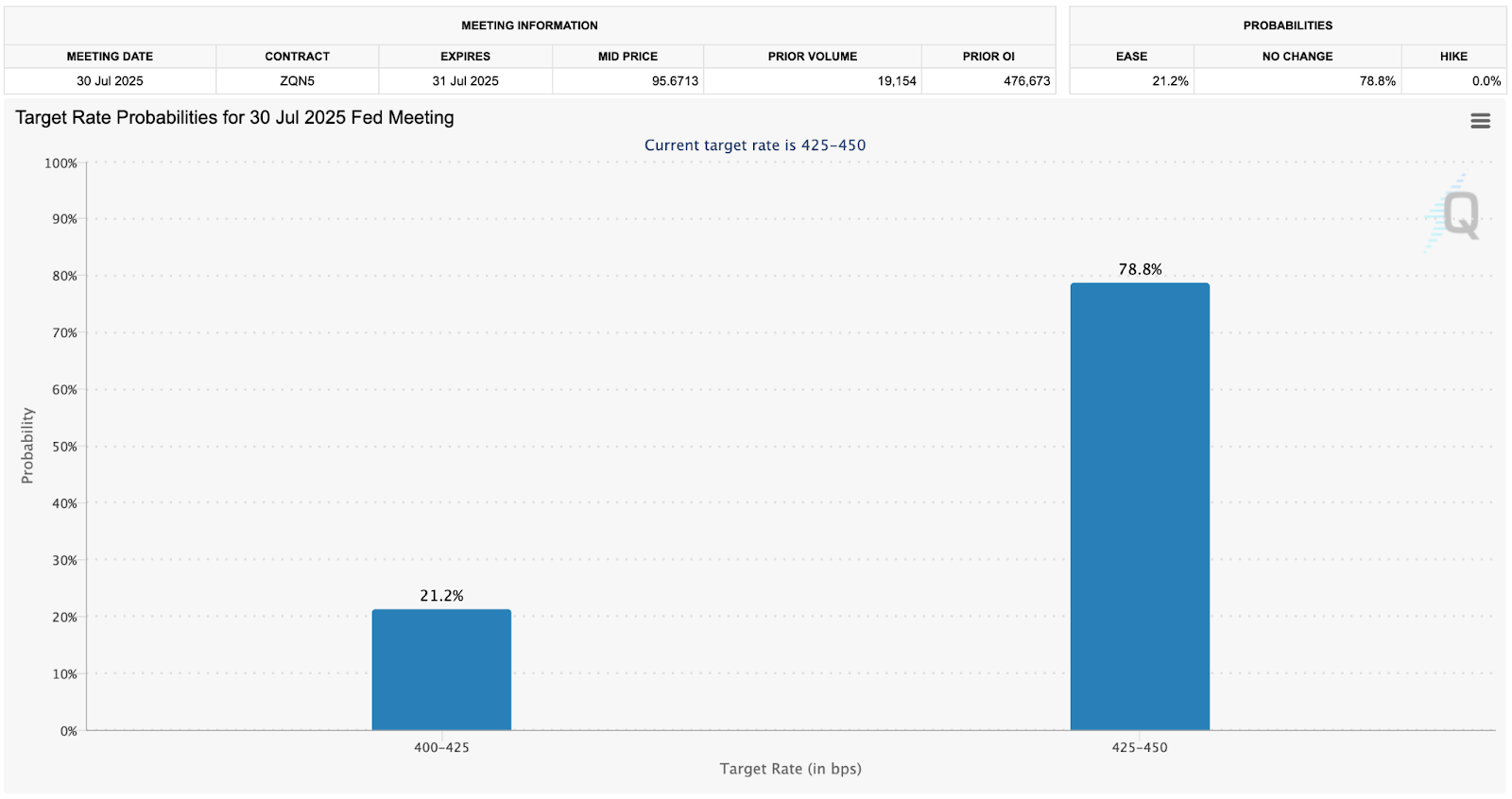

The June 2025 NFP release comes after a week in which the Fed’s preferred inflation gauge, core PCE, surprised to the upside, coming in around 2.7% year-on-year. Yet markets hardly flinched, largely because the Fed has already revised its inflation forecasts higher and is still signalling two rate cuts this year.

That’s given investors confidence that the Fed is willing to look through moderate inflation surprises, especially if job market data begins to show further signs of deterioration. As a result, market pricing continues to reflect rising odds of a July 2025 rate cut, despite inflation coming in hotter than expected.

(Source: CME Group)

Labour market in focus: Good news is good, bad news is bad

This week’s jobs data could reinforce a new market dynamic: bad news on employment is increasingly seen as a catalyst for easier monetary policy, while strong data is simply confirmation that the economy remains in decent shape.

In other words, the Fed appears to be leaning toward its employment mandate over its inflation mandate, at least at the margin. A softer June 2025 NFP print may bolster the case for a cut as early as July, while a stronger reading would likely be welcomed by equity markets, which have remained bullish even amid lingering inflationary risks.

Wall Street hits record highs supported by AI, trade optimism

US stock indices, particularly the S&P 500 and Nasdaq, have surged to record highs in mid-2025, fuelled largely by tech outperformance and optimism around AI. However, the rally remains narrow, with cyclicals lagging and the Dow still below its highs. This divergence suggests markets still see growth risks from tariffs and trade uncertainty—a backdrop that makes incoming macro data like the June NFP even more crucial.

If the labour market does continue to soften, it may finally draw more attention to the risks simmering below the surface. For now, though, the market remains in buy-the-dip mode, especially with Fed officials signalling willingness to cut to support the labour market.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)