FOMC rate cut priced-in as employment softens, despite sticky inflation

The FOMC is expected to cut rates by 25 basis points, with attention on the central bank's guidance amid expectations for further cuts in the future.

The Federal Open Markets Committee meets on October 28–29 and is expected to cut interest rates by 25 basis points.

Labour market weakness meets stubborn inflation

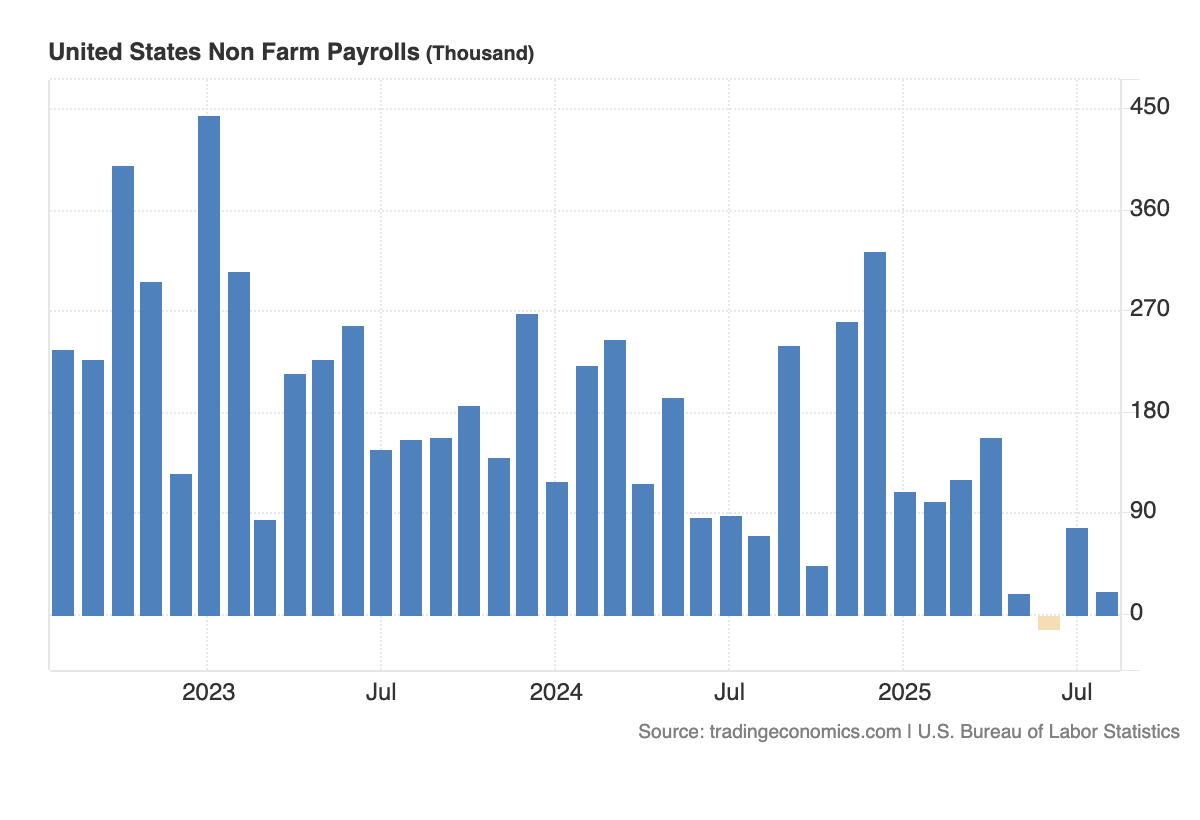

The expected Fed cut comes amid further signs of softening in the US labour market. The unemployment rate has nudged higher to 4.3%, and jobs growth has slowed markedly—trends partly attributed to supply-side disruptions caused by the Trump administration’s changes to immigration policy. While the recent government shutdown has limited the availability of economic data, the signal from what’s available, including private payroll data, points to cooling economic momentum.

(Source: Trading economics)

(Source: Trading economics)

At the same time, inflation remains elevated and uneven. Core PCE—the Fed’s preferred inflation gauge—is running at 2.9%, while September’s core CPI rose to 3.0%, rising from 2.9% the month prior, although less than 3.1% expected. Some of this is due to one-off price effects tied to tariffs and goods inflation, but services inflation has stayed stubborn, and inflation expectations may be drifting higher. This leaves the Fed balancing weaker growth against still-sticky inflation as it weighs the next steps.

Markets look for confirmation but risk disappointment

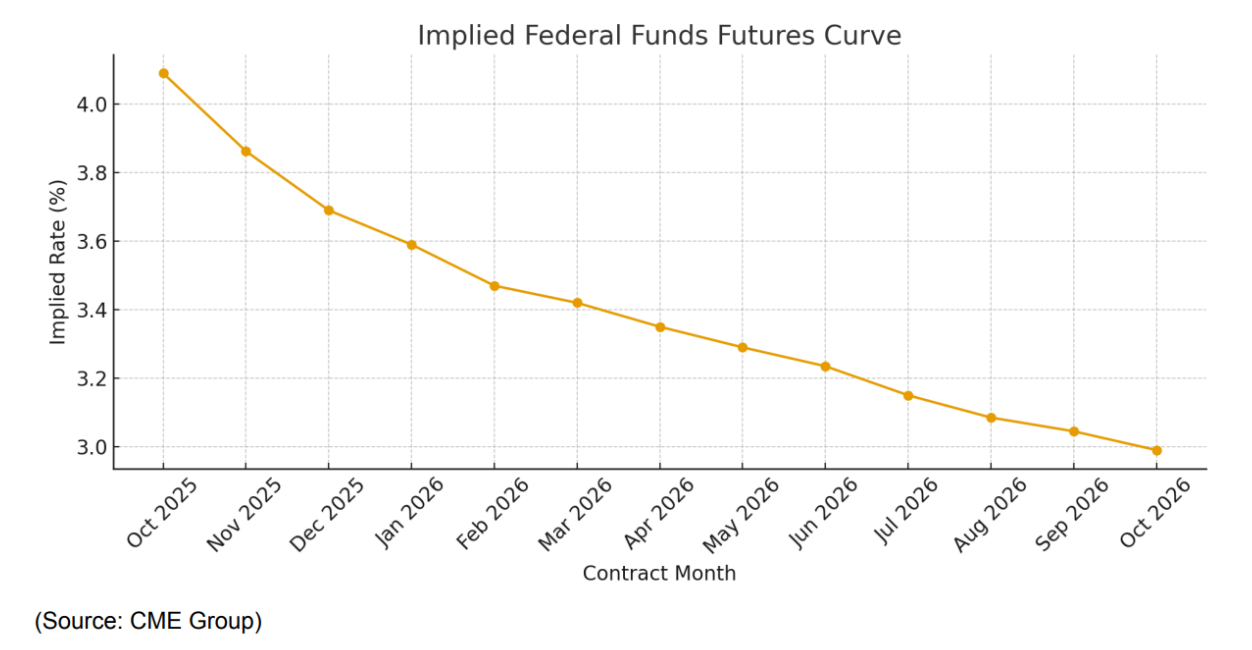

Markets are fully pricing in this week’s expected cut, and futures point to another in December. Traders are also pricing a steady glide path lower for the Federal Funds Rate, with expectations that it will fall below 3% by the end of 2026—well into accommodative territory. However, with no updated Summary of Economic Projections at this meeting, there’s limited opportunity for the Fed to formally validate or challenge that outlook.

Attention will shift to Chair Jerome Powell’s press conference for any hints on the future path of policy. While he’s unlikely to push back aggressively against market pricing, he may also avoid signalling deeper easing given persistent inflation and the lack of fresh data. That creates asymmetric risk: with markets already leaning dovish, even a neutral tone could be perceived as hawkish. Traders should be prepared for volatility if Powell’s remarks fall short of dovish expectations.

The US Dollar Index shows signs of bottoming with cuts baked in

Because of the cuts already baked-in to the curve going into the FOMC meeting, the risks to the market could be asymmetric. A hawkish surprise would probably see a larger reaction than a dovish one.

After a 10% high-to-low correction this year, the US Dollar Index appears to be bottoming, supported recently by political risk in Europe and Japan weighing on the Euro and Yen, respectively. Economic growth has also rebounded following the trade related slowdown earlier in the year.

The rounding shape of price action on the bullish divergence on the weekly RSI is a constructive technical signal for the US Dollar. A break through 100 on the DXY could spark further Dollar strength. A push below 96.50 would confirm a continued downtrend.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)