Australian quarterly CPI could open the door to another RBA cut

The markets expect a soft official inflation read and another RBA rate cut

Australia’s second-quarter inflation data will be a critical moment for markets and the Reserve Bank of Australia.

CPI data expected to show decline in trimmed mean inflation

The official CPI release, due on 30 July, is forecast to show further disinflation, with the trimmed mean CPI expected to rise 0.7% quarter-on-quarter and 2.7% year-on-year, according to market estimates. That would mark a deceleration from the 2.9% rate recorded in Q1 and continue the steady decline in underlying inflation.

Headline inflation is also expected to ease, with CPI forecast at 0.8% QoQ and 2.1% YoY—both down from the previous quarter’s 0.9% and 2.4% readings respectively. The RBA’s preferred core measure—the trimmed mean—will be in focus, especially given the central bank’s recent emphasis on this figure as a guidepost for policy.

RBA’s forecasts in line with market estimates

The Q2 data will be judged relative to the RBA’s projections. In its May Statement on Monetary Policy, the central bank expected trimmed mean inflation to slow to around 2.6% by mid-2025—revised down slightly from 2.7% in its February forecasts. The current market consensus of 2.7% YoY slightly overshoots the May estimate but still falls within the central bank’s broader expectations.

What’s more, those forecasts were predicated on the assumption that interest rates would be lowered gradually throughout 2025. As such, a print within the 2.6–2.7% range would validate the current outlook, and likely trigger no meaningful shift in the RBA’s policy stance—especially considering the central bank left rates on hold at its most recent meeting to gain “greater clarity” from the Q2 inflation data.

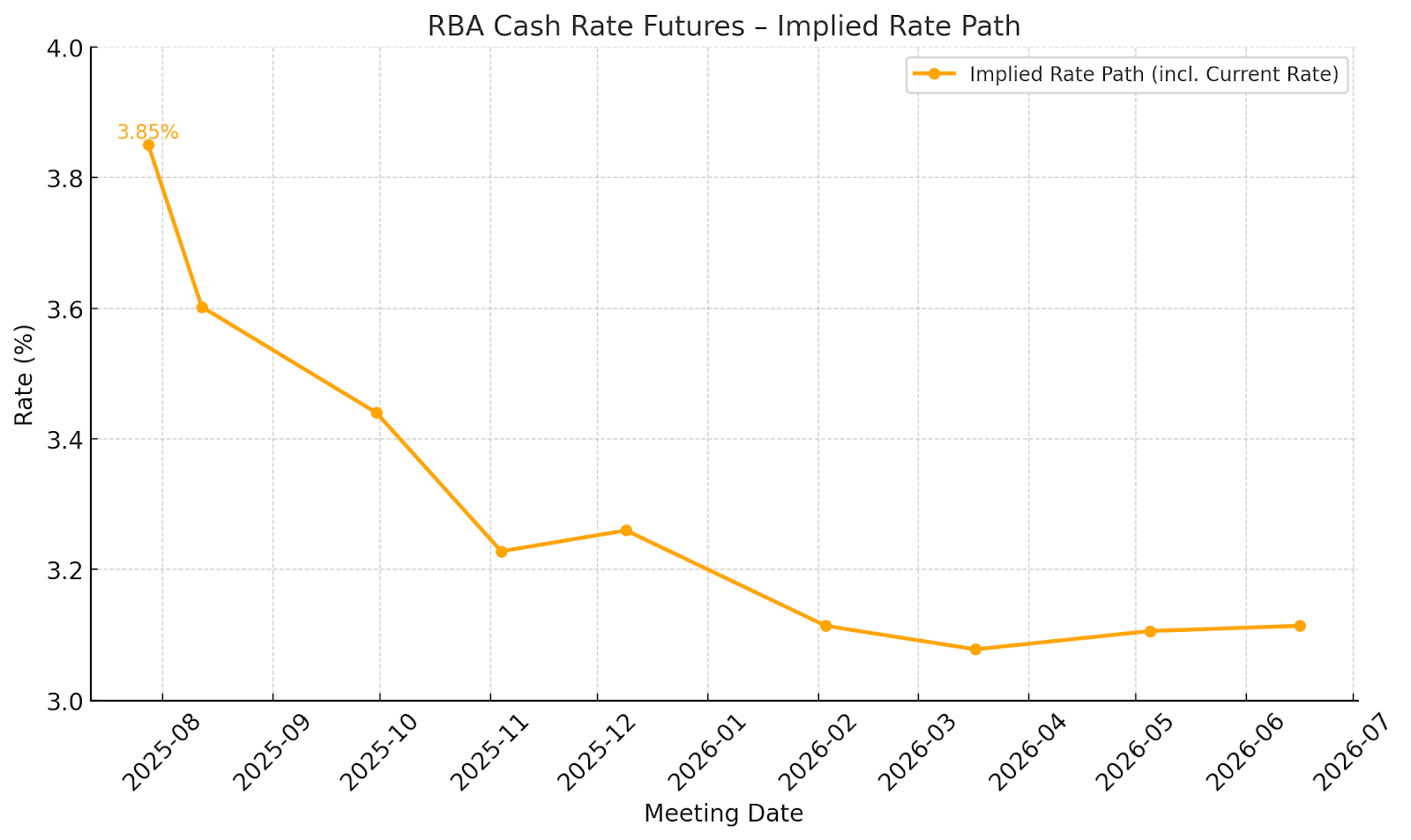

The markets are already priced for August rate cut

Markets are almost fully convinced that the RBA will cut the cash rate when it meets on 12 August. Rates markets currently imply a 98% probability of a 25 basis point reduction, taking the cash rate from 3.85% to 3.60%, with several more cuts priced in by mid-2026. Implied rates fall steadily over the coming year, with futures pointing to a policy rate near 3.11% by June 2026.

This aggressive path reflects not only expectations for disinflation, but also recent weakness in the Australian labour market, which has shown signs of slackening. Soft CPI data would offer the RBA the confirmation it needs to proceed with a cut, justifying a more accommodative stance in light of deteriorating economic momentum.

(Source: Bloomberg)

AUD/USD could rise and ASX200 on upside surprise

Despite the high conviction in markets that the RBA will ease, the risks around this week’s inflation release are not evenly balanced. With a cut all but fully priced in, a soft print in line with expectations may not materially shift rates pricing, nor spark major moves in the AUD or equity markets.

But a hotter-than-expected number—particularly a trimmed mean CPI significantly above 2.7%—could trigger a sharp reaction. Such a surprise would challenge the current policy narrative and force traders to reprice the near-term path for interest rates. That, in turn, could push the Australian dollar higher and weigh on the interest rate-sensitive ASX 200, as expectations for August easing are pared back.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)

The RBA remains focussed on inflation despite weak jobs market

This inflation print may also carry additional weight in understanding the RBA’s reaction function. After surprising markets by holding rates steady at its last meeting, Governor Michele Bullock and the Board made clear that they were waiting on the full Q2 inflation data before making their next move. That decision reintroduced an earlier pattern in the RBA’s reaction function: waiting for the quarterly CPI rather than relying on monthly indicators and shifting focus to the weakening labour market.

Given that, markets will interpret this week’s figures as a final hurdle for the RBA before resuming its easing cycle. With inflation trending lower, the labour market weakening, and real activity indicators flashing red, the bar for delaying a rate cut is high. If the CPI comes in soft, the RBA will have the justification to cut further in order to support the labour market as growth remains anemic.