Michael Kramer: Why Do Revisions Matter So Much in the Payroll Report?

The most important number in the monthly US non-farm payroll report may not be the headline payroll figure, but the revisions that follow months later.

Author: Michael Kramer, Mott Capital Management | For publication on Capital.com

The most important number in the monthly US non-farm payroll report may not be the headline payroll figure, but the revisions that follow months later. Revisions matter because markets, policymakers and investors make real-time decisions based on data that later proved materially inaccurate.

The non-farm payroll report is typically released on the first Friday of each month and is one of the most closely watched economic data releases published by the US government. The report shows how many jobs were created during the month, the unemployment rate and the pace of wage growth.

A significant portion of the report relies on estimates. Each month, the Bureau of Labour Statistics*1 surveys roughly 119,000 businesses and government agencies, representing approximately 622,000 individual worksites. In addition to the survey data, the BLS applies seasonal adjustments and uses the birth-death model, which estimates the number of businesses being created or closed each month. Because of this, the jobs report is revised regularly.

Markets continue to react aggressively to the initial payroll release because it remains one of the timeliest snapshots of economic momentum available to investors and policymakers. That said, while the headline figures attract most of the attention, revisions often provide a much clearer picture of the labour market particularly when the initial reading overstates or understates underlying employment conditions.

Revisions can either reinforce or weaken the market's interpretation of the current report. A strong headline has historically been viewed more favourably when accompanied by upward revisions to prior months. At the same time, a strong initial reading can lose impact when the accompanying revisions disappoint.

Where Revisions Really Matter

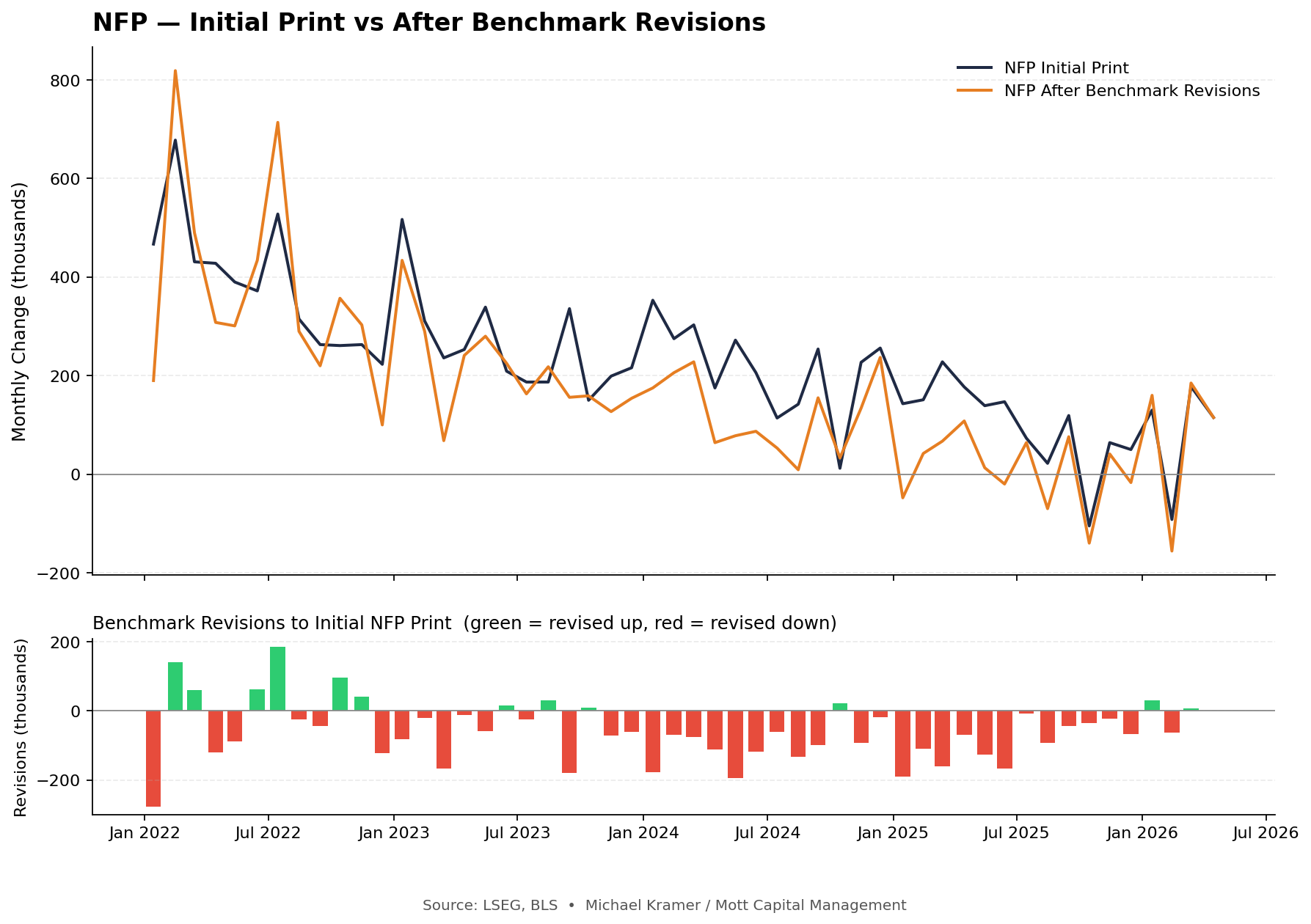

There was a period from the middle of 2023 through the end of 2025 during which revisions consistently came in significantly lower than the initial payroll estimates. Anyone focusing solely on the initial releases may have concluded that the labour market was materially stronger than it was.

(Source: LSEG, BLS. Michael Kramer / Mott Capital Management)

(Past performance is not a reliable indicator of future results)

The revisions suggested that employment growth was slowing and that the labour market was weaker than the initial reports implied. That distinction mattered for policymakers at the Federal Reserve when determining the appropriate path for monetary policy.

Changes in the Policy Path

The revision process does not end with the monthly updates. Data is continually revised throughout the year and ultimately reconciled with the Quarterly Census of Employment and Wages (QCEW). In 2025, this benchmark process showed that employment growth in the US had been materially weaker than the monthly payroll reports initially projected.

The QCEW is a labour market report based on actual unemployment insurance tax records filed by employers, covering more than 95% of US jobs. The preliminary benchmark estimate released in September 2025 showed that the US labour market had created roughly 911,000 fewer*2 jobs than initially indicated by the monthly payroll reports. The data was finalised in the February 2026 payroll report, which showed that approximately 898,000*3 fewer jobs had been created between March 2024 and March 2025 than originally estimated.

These revisions were substantial and likely contributed to the Federal Reserve's growing confidence that labour market conditions were cooling sufficiently to begin cutting policy rates at its September, October and December meetings. By the time the QCEW revisions were fully incorporated, it had become clear that the initial payroll reports had largely overstated the pace of job growth, while the benchmark data confirmed that hiring conditions were considerably weaker than they had first appeared.

Payroll revisions shaped a very different market narrative from the one implied by the initial reports. Those revisions began to influence expectations about Federal Reserve policy, particularly when data trended in a direction that required a policy response.

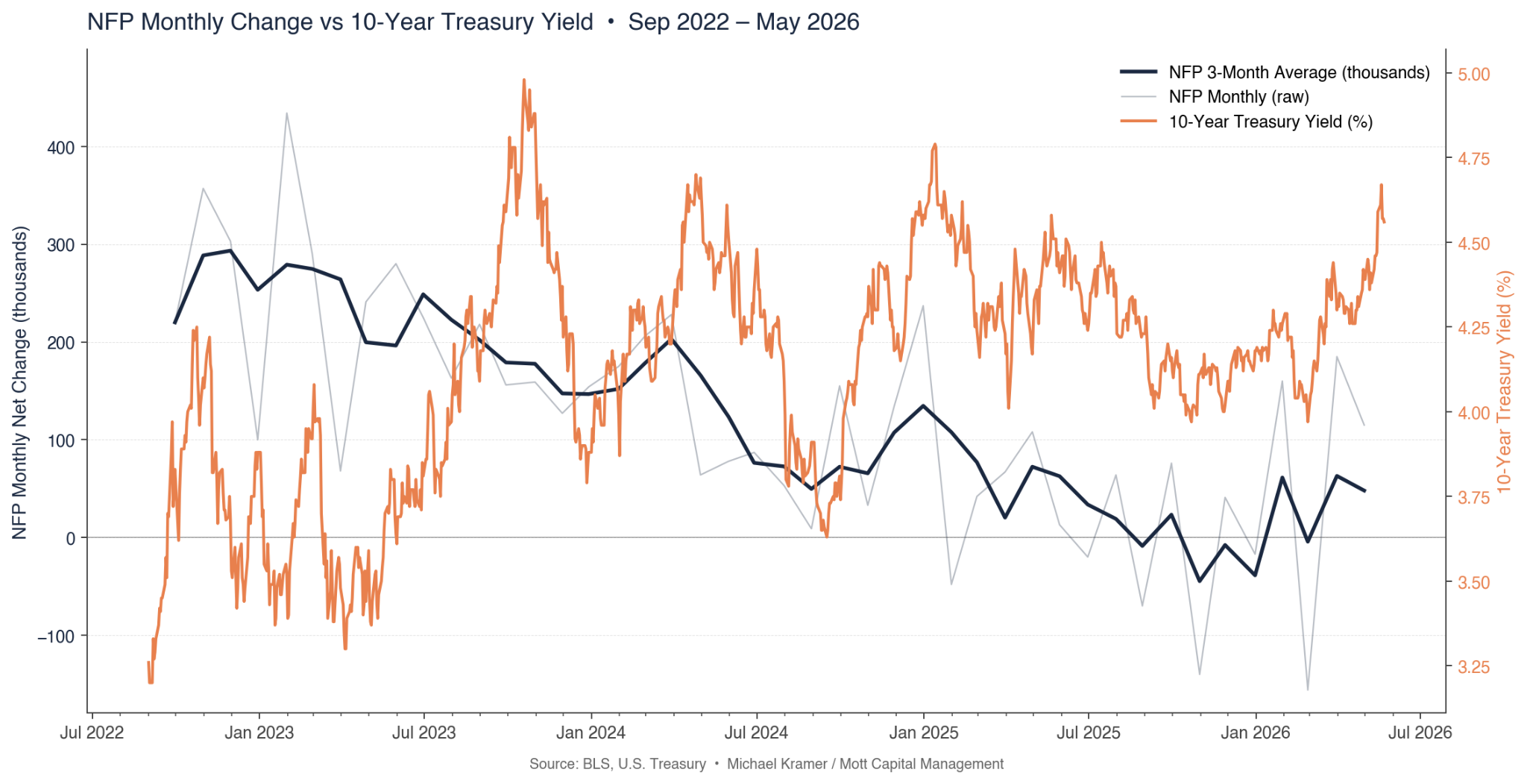

The revisions played a clear role in broader market trends, especially in interest rates and the US dollar. Beginning in 2024, the 10-year Treasury yield broadly trended lower alongside the weakening trend in the revised labour market data.

(Source: BLS, U.S. Treasury • Michael Kramer / Mott Capital Management)

(Past performance is not a reliable indicator of future results)

The payroll report is a constantly evolving estimate of economic conditions. Over time, the revisions, not the headline, have consistently told the more consequential story, shaping both monetary policy expectations and broader market direction.

Sources

*1 Bureau of Labour Statistics — Current Employment Statistics: https://www.bls.gov/ces/

*2 Economy Insights — US added fewer jobs than previously reported (September 2025 benchmark): https://www.economyinsights.com/p/us-added-fewer-jobs-than-previously-reported

*3 BLS — Employment Situation Summary, February 2026 (final benchmark revision): https://www.bls.gov/news.release/archives/empsit_02112026.htm

This article is written by Michael Kramer of Mott Capital Management and is published on Capital.com for educational and informational purposes only. The content does not constitute financial advice or a recommendation to buy or sell any financial instrument. Past performance is not a reliable indicator of future results. CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. The majority of retail investor accounts lose money when trading CFDs. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.