EUR/USD forecast: Third-party price targets

Movements in the euro–US dollar exchange rate often reflect a shifting balance between economic data, central bank expectations and broader market conditions.

With EUR/USD trading near familiar levels at the start of 2026, attention has turned to how recent price behaviour fits within the wider context of monetary policy, liquidity and longer-term trends.

Euro–US dollar (EUR/USD) is trading around 1.1698 in early US session trading on 7 January 2026, within an intraday range of 1.1677–1.1738 on Capital.com’s feed as of 3:08pm UTC. The pair is holding close to levels cited by external platforms around 1.1690–1.1685, reflecting relatively contained price action after Monday’s dip towards the mid-1.16 area. Past performance is not a reliable indicator of future results.

The move comes amid a modestly firmer US dollar, with the US Dollar Index hovering near 98.6 ahead of key US labour market and services data (Trading Economics, 7 January 2026). At the same time, softer eurozone inflation readings around 2% have reinforced expectations that the European Central Bank will keep policy steady in the near term (Euronews, 7 January 2026). Market commentary also notes that EUR/USD is trading near recent lows with a bearish bias still evident, as liquidity remains moderate after the turn of the year (Investing.com, 1 January 2026).

Past performance is not a reliable indicator of future results.

Euro forecast 2026–2030: Analyst price target view

As of 7 January 2026, third-party EUR/USD forecasts cover a broad range of medium-term scenarios, as major institutions assess relative monetary policy, growth dynamics and capital flows between the US and the euro area. The following views summarise selected third-party targets and frameworks published between late-2025 and early-2026.

BNP Paribas (G10 FX strategy)

BNP Paribas states in its Currencies Focus that, as of 13 November 2025, it holds a three-month EUR/USD target of 1.16 and a 12-month target of 1.24, expressed as the value of one euro against the US dollar. The bank points to expected Federal Reserve rate cuts, stable European Central Bank policy and an anticipated erosion of the US dollar’s safe-haven appeal as factors shaping its medium-term outlook (BNP Paribas Wealth Management, 13 November 2025).

ING (FX outlook)

ING’s G10 FX Outlook discusses EUR/USD 'fair value' rising from the 1.15 area towards around 1.20 over 2026, rather than setting a single spot target. This view is linked to expectations for gradual improvement in eurozone growth, lower energy prices and modest US dollar depreciation, alongside concerns around US debt dynamics and equity valuations (ING Think, 10 November 2025).

MUFG

G10 FX 2026 outlook (December 2025)

MUFG’s G10 FX 2026 Outlook presents a constructive and balanced EUR prediction, describing the pair – EUR/USD –as biased higher in a 'post-peak USD world' without assigning a single year-end target. The analysis highlights an ECB expected to remain on hold through 2026, alongside projected Federal Reserve cuts and a generally softer US dollar (MUFG Research, 19 December 2025).

Annual FX outlook update

An January 2026 FX outlook update from MUFG reiterates expectations that EUR/USD could trade above the 1.2000 level over the cycle. The bank notes that this threshold has historically marked the divide between negative and non-negative euro rate environments, while pointing to returning foreign inflows into European bonds and equities, ECB policy stability and inflation near target as potential supporting factors (MUFG Research, 7 January 2026).

Reuters (FX outlook and update)

A currency strategists survey released on 3 December 2025 by Reuters reported median expectations for EUR/USD near 1.17 in three months, rising to about 1.19 in six months and 1.20 on a 12‑month view. The poll notes a broadly weaker dollar narrative tied to Fed rate‑cut bets, while flagging that a sizeable minority of respondents see scope for renewed dollar strength if market expectations prove too dovish (Investing.com, 3 December 2025).

In an early‑January 2026 follow‑up, Reuters reported that its latest poll still pointed to a modest euro appreciation over the year, with median projections indicating incremental gains of roughly 1% and an end‑2026 level around 1.20. Strategists in that survey described the dollar outlook as generally soft amid expectations for gradual Fed easing and ongoing concerns over central‑bank independence, while acknowledging upside risks to the dollar if those assumptions shift (Reuters, 7 January 2026).

Predictions and third-party forecasts are inherently uncertain, as they cannot fully account for unexpected market developments. Past performance is not a reliable indicator of future results.

Euro–US dollar: Technical overview

EUR/USD is trading near 1.1698 as of 3:08pm UTC on 7 January 2026, sitting just below the 20-day simple moving average around 1.1733, while broadly aligned with the 30-day SMA near 1.1694. On the daily chart, a dense moving-average cluster is visible around the 20-, 50-, 100- and 200-day SMAs, roughly at 1.17 / 1.16 / 1.17 / 1.16, with the 50- and 100-day measures remaining beneath spot and broadly supportive.

The 14-day RSI near 48.7 points to neutral, mid-range momentum, while an ADX reading close to 23.7 suggests a trend that is developing but not firmly established.

On the upside, the nearest Classic resistance level is R1 around 1.1834, with a daily close above that area bringing R2 near 1.1930 into focus. On pullbacks, the Classic Pivot at 1.1712 offers initial support, with the 100-day SMA around 1.17 and the 200-day SMA near 1.16 forming a broader support zone. A sustained break below this area on a closing basis would increase the risk of a move towards S1 near 1.1616 (TradingView, 7 January 2026).

This technical analysis is provided for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any instrument.

EUR/USD history

EUR/USD spent much of early 2024 trading close to the 1.08 level, edging higher through the spring and summer before moving into the low-1.10s by late September. By year-end, the pair had slipped back towards the 1.03–1.05 range, closing at around 1.04 on 31 December 2024 and starting 2025 just above 1.03 against the US dollar.

Through 2025, EUR/USD established a gradual upward trend, rising from roughly 1.03 in January to the mid-1.13s by late May, before extending into the 1.17–1.18 zone during the summer and early autumn. After a brief dip towards 1.14 in June and a subsequent consolidation phase around 1.15–1.16 in late summer, the pair moved back into the mid-1.17s in December 2025 and remained near that area into early 2026, closing at about 1.17 on 7 January 2026.

Past performance is not a reliable indicator of future results. Share prices are indicative and may differ from live market prices.

Capital.com analysis: Euro–US dollar outlook

Over the past two years, the euro–US dollar pair has moved from the low-1.03 region to the high-1.17s, reflecting a material recovery in the euro against the US dollar, alongside extended periods of consolidation. Price swings have often aligned with changing expectations for interest rates and growth on both sides of the Atlantic. Periods of euro strength have tended to coincide with phases of US dollar softness, while pullbacks have followed stronger US data or renewed demand for dollar safety.

A key focus for many market participants remains the evolving policy gap between the Federal Reserve, which has already begun cutting rates, and the European Central Bank, which ended 2025 with policy on hold and inflation projections close to target. A narrowing US–euro area rate differential and firmer eurozone confidence may support the euro, but shifts in US rate expectations, weaker European data or renewed risk aversion could see the dollar regain ground, keeping EUR/USD under pressure.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage; a high percentage of retail investor accounts lose money when trading CFDs. Past performance is not a reliable indicator of future results.

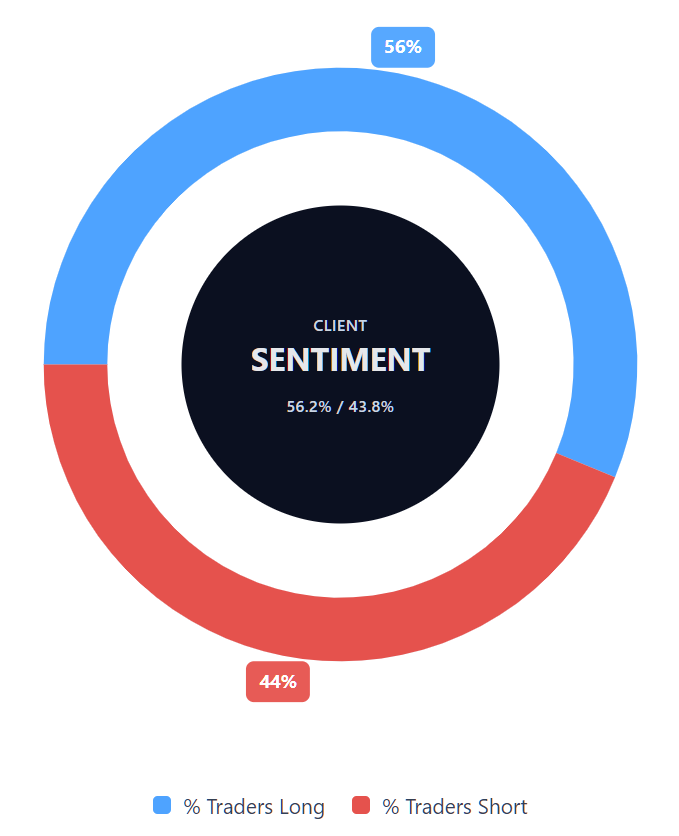

Capital.com’s client sentiment for EUR/USD CFDs

On 7 January 2026, Capital.com client positioning in EUR/USD CFDs showed 56.2% buyers versus 43.8% sellers, indicating a moderate long bias of around 12.3 percentage points. Positioning remains balanced rather than one-sided, with both bullish and bearish views still well represented. This snapshot reflects open positions on Capital.com and can change over time as clients respond to market developments.

Summary: EUR/USD (2025–2026)

- EUR/USD started 2025 just above 1.03 and trended higher through the year, reflecting a notable recovery in the euro against the US dollar.

- The pair moved into the mid-1.13s by late May and spent much of the second half of the year oscillating between roughly 1.14 and 1.18, as markets responded to shifting rate expectations and data releases.

- By December 2025, EUR/USD was trading in the mid-1.17s, with external commentary focusing on diverging ECB–Fed policy paths and a softer US dollar narrative.

- Technical studies in early January 2026 show price holding near a concentrated moving-average zone around the mid-1.16 to mid-1.17 area, with daily momentum indicators remaining broadly neutral.

- Analyst scenarios for 2026 cluster within a 1.16–1.24 range, linking potential euro strength to Federal Reserve easing and steady ECB policy, while noting that renewed US dollar demand could limit or reverse gains.

Past performance is not a reliable indicator of future results.

FAQ

What is the 2026 EUR forecast (euro to US dollar)?

What influences EUR/USD movements?

Could EUR/USD go up or down?

How can traders access EUR/USD CFDs on Capital.com?

On Capital.com, traders can access EUR/USD through contracts for difference (CFDs), which allow them to speculate on price movements without owning the underlying currency. The platform provides real-time pricing, charting tools and risk-management tools, such as take-profit and stop-loss orders. CFDs are traded on margin, and leverage amplifies both profits and losses.*

*Standard stop-loss orders aren’t guaranteed. Guaranteed stop-loss orders (GSLOs) incur a fee if activated.