What’s this document for?

This document will show a complete costs and charges breakdown across our products, covering spreads, overnight adjustments, guaranteed stop-loss orders (when activated), and currency conversion fees (where applicable).

You’ll find examples demonstrating how we calculate our fees, which you can apply to your own trades to estimate the cumulative effect of our costs and charges on your returns.

It’s important to remember that your total costs will increase proportionate to your trading volumes.

The example trades and the values shown in this document are for illustrative purposes only. They should not be treated as forecasts, recommendations or endorsements of a particular trading strategy.

- For more information on our costs and charges, click here.

- You can also find out how we price our markets per asset class by clicking here.

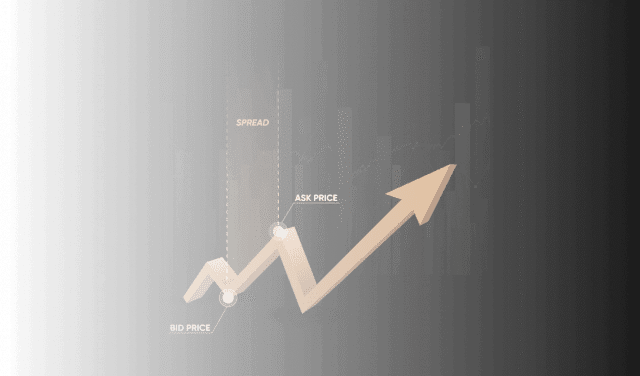

Spread cost examples for CFD trades

In this section, we’ll focus on spread cost examples across our five main asset classes, using CFDs. The spread is the difference between the bid and ask price of the market at the time you place your trade. It’s charged to cover the cost of facilitating the trade, and it’s the main way we and other derivatives brokers make money.

Trading outside regular exchange hours may be available on selected stocks. Please note that spreads can widen, and liquidity may be lower during these times, which can impact execution quality and cost.

You can find typical spread prices by clicking on your chosen asset on our markets page, in the ‘All markets’ section.

Forex

- You hold a position of 100,000 units of EUR/USD, with a bid/offer quote at 1.05000/1.05006.

- The spread on this market is therefore 0.6 pips (0.00006).

- Opening the position: you pay half the spread when you enter (0.3 pips, or 0.00003).

- Closing the position: you pay the other half when you exit (0.3 pips, or 0.00003).

- The spread is calculated in the quote currency.

- Total cost of the spread: 100,000 units × 0.00006 = $6 (or equivalent in your account currency).

Commodities

- You hold a position of 10 contracts on Gold (10 troy ounces), with a bid/offer quote at 2500.00/2500.30.

- The spread on this market is therefore 0.30 points (2500.30-2500.00).

- Opening the position: you pay half the spread when you enter (0.15 points).

- Closing the position: you pay the other half when you exit (0.15 points).

- Total cost of the spread: 10 contracts × 0.30 points = $3 (or currency equivalent).

Indices

- You hold a position of 1 contract on the UK 100, with a bid/offer quote at 9000/9001.

- The spread on this market is therefore 1 point (9001-9000).

- Opening the position: you pay half the spread when you enter (0.5 points).

- Closing the position: you pay the other half when you exit (0.5 points).

- Total cost of the spread: 1 contract × 1 point = £1 (or currency equivalent).

Shares

- You hold a position of 10 shares on Apple, with a bid/offer quote at 240.00/240.13.

- The spread on this market is therefore 0.13 points (240.13-240.00).

- Opening the position: you pay half the spread when you enter (0.065 points).

- Closing the position: you pay the other half when you exit (0.065 points).

- Total cost of the spread: 10 shares × 0.13 points = $1.30 (or currency equivalent).

Cryptocurrencies

- You hold a position of 0.1 contracts on Bitcoin, with a bid/offer quote at 90,000/90,050.

- The spread on this market is therefore 50 points (90,050-90,000).

- Opening the position: you pay half the spread when you enter (25 points).

- Closing the position: you pay the other half when you exit (25 points).

- Total cost of the spread: 0.1 contracts × 50 points = $5 (or currency equivalent).

Overnight funding (swaps) cost examples

When you hold a CFD position open overnight, a small adjustment, known as a swap, may be applied to reflect the cost or benefit of maintaining that exposure. Whether you pay or receive this amount depends on several factors, such as the direction of your trade, the underlying interest rate for the asset, and any adjustments for holding it beyond the trading day.

It’s important to note that swap charges are based on the total value of your open position, not the margin you’ve committed. In other words, even if you’ve used leverage to open a trade, the full position size – also known as the notional value – is used in the calculation. This ensures consistency in how funding costs are applied, regardless of how much capital was initially required.

The examples below illustrate how these overnight adjustments are worked out across different asset classes, using simplified and rounded figures for clarity.

Forex

- You hold an overnight position of 10,000 units of USD/JPY. Your nominal exposure is therefore $10,000.

- For the purposes of this calculation, let’s say the overnight swap (or TomNext) rate for USD/JPY is currently -0.0182. At the prevailing spot price of 132.80 that equates to -0.0137% daily.

- Our daily fee is 0.00411%.

- So to hold a long position overnight you would receive 0.00959% – the negative USD/JPY swap rate less our fee – of your exposure, which, converted from JPY, is $0.96 or currency equivalent.

- To hold a short position, you would pay 0.01781% – the positive swap rate plus our fee – of your exposure, which is $1.78 converted, or equivalent.

Commodities

- You have a position of 4,000 therms of Natural Gas, currently priced at $2.54. Your position’s full exposure is therefore $10,160.

- Let’s say the overnight basis adjustment for Spot Natural Gas is currently 0.0031. At the prevailing spot price of 2.54 that equates to 0.12205% daily.

- Our daily fee is 0.01096%.

- For a long position, you’d pay 0.13301% (our fee + the basis adjustment) = $13.51.

- For a short position, you’d receive 0.11109% (our fee – the basis adjustment) = $11.29.

Indices (USD denominated)

- You have a position of 0.6 contracts on the US Tech 100, priced at 20140. Your full exposure would be $12,084.

- Since the US Tech 100 is denominated in USD, the relevant benchmark rate is SOFR. Let’s say this is 5.01448% annually, or 0.01393% daily.

- Our daily fee is 0.01111%.

- For a long position, you’d pay 0.02504% (Our fee + SOFR) = $3.03.

- For a short position, you’d receive 0.00282% (Our fee – SOFR) = $0.34.

Indices (GBP denominated)

- You have a position of 1 contract on the UK 100, priced at 8175. Your full exposure would be £8,175.

- Since the UK 100 trades in GBP, the relevant benchmark rate is SONIA – let’s say this is 4.98260% annually, or 0.01365% daily.

- Our daily fee is 0.01096%.

- For a long position, you’d pay 0.02461% (our fee + SONIA) = £2.01.

- For a short position, you’d receive 0.00269% (our fee – SONIA) = £0.22.

Shares (USD denominated)

- You have a position equivalent to 50 shares in Tesla, currently priced at $252. Your total exposure is $12,600.

- Since Tesla trades in USD, the relevant benchmark rate is SOFR. Let’s say this is 5.01448% annually, or 0.01393% daily.

- Our daily fee is 0.01111%.

- For a long position, you’d pay 0.02504% (our fee + SOFR) = $3.16.

- For a short position, you’d receive 0.00282% (our fee – SOFR) = $0.36.

Shares (GBP denominated)

- You have a position equivalent to 4000 shares in Barclays, currently priced at £2.41. Your total exposure is £9,640.

- Since Barclays trades in GBP, the relevant benchmark rate is SONIA. Let’s say this is 4.98260% annually, or 0.01365% daily.

- Our daily fee is 0.01096%.

- For a long position, you’d pay 0.02461% (our fee + SONIA + our fee) = £2.37.

- For a short position, you’d receive 0.00269% (our fee – SONIA) = £0.26.

Cryptocurrency CFDs

- Long positions: you’ll pay 0.06164% of the nominal position value daily (or 22.5% annually).

- Short positions: you’ll receive 0.0137% of the nominal position value daily (or 5% annually).

Example

- You have a position on BTC with a nominal value of $100,000 which you hold overnight.

- For a long position, you’d pay $61.64 (or currency equivalent) (0.06164% of 100,000).

- For a short position, you’d receive $13.70 (0.0137% of 100,000).

Bonds/interest rates

- You have a position on the US 10-Year T-Note CFD, currently priced at $112.50 per 100 face value. Your position’s full exposure is $200,000.

- Let’s say the overnight basis adjustment is -0.0008. At a price of 112.50, that equates to: (-0.0008 / 112.50) × 100 = -0.0711% daily

- Our daily fee is 0.01096%.

- If you're long:

Total overnight rate = 0.01096% - 0.0711% = -0.06014%

Funding = $200,000 × -0.06014% = -$120.28

You’d receive a credit of $120.28 overnight. - If you're short:

Total overnight rate = 0.01096% + 0.0711% = 0.08206%

Funding = $200,000 × 0.08206% = $164.12

You’d pay a funding cost of $164.12 overnight.

Guaranteed stop-loss order cost example

A guaranteed stop-loss order (GSLO) fee is only charged if the GSLO is triggered. The GSLO closes the trade at exactly the price level you specify, with no risk of gapping or slippage. Since we take on this risk for you, we (and other providers) charge a fee for using the GSLO.

You can see the GSLO fee on the deal ticket before placing your trade, once you’ve selected a GSLO. The GSLO premium itself varies depending on the specific market, the position's open price, and the quantity traded.

Formula

You can check the GSLO fee value on the deal ticket when opening a position and adding GSLO.

Guaranteed stop-loss order example

- You open a long position of 1 Gold contract, with a bid/offer quote at $2,000/$2,000.30.

- You place a GSLO at $1,980 to limit potential losses.

- Assume the GSLO premium for this market is 0.03%.

- If the market drops to $1,980, the GSL ensures your position is closed exactly at that price, with no slippage.

GSLO fee calculation:

- GSLO fee = GSLO premium × position open price × quantity

- 0.03% × $2,000.30 × 1 contract = $0.60

- Total GSLO fee charged (if triggered): $0.60

Conversion fees

When trading an asset priced in a different currency than your account’s base currency, a small conversion fee applies.

The fee is calculated as 0.7% of the spot forex rate for retail clients.

Conversion fee calculation

- You’re trading in an account denominated in USD.

- You have an open CFD trade on France 40 – denominated in EUR – that’s in profit by €10.

- This is shown on your position as $10.85 (€10 at the spot EUR/USD rate of 1.08461) and you decide to close the trade.

- If no currency conversion fee had been applied, the profit of that position would be simply be calculated as follows:

However, at the point of closure you’ll be charged the 0.7% currency conversion fee. The calculation is done as an ‘all-in’ conversion rate which encompasses the spot rate and the 0.7% fee.

The all-in rate is 0.7% less favourable than the spot rate, and therefore the profit realised on the position would be slightly less:

Your profit after the currency conversion fee is:

Therefore, in this example, you’ve been charged a currency conversion fee of $0.08.

| Conversion fee rate | Currency conversion cost | |

|---|---|---|

| Without the currency conversion fee | 0% | $0 |

| With the currency conversion fee | 0.7% | $0.08 |

You can see the ‘all-in’ rate used for the conversion of each transaction in the ‘Reports’ section of the platform, as well as on your statements.

Dynamic currency conversion fees

If you deposit or withdraw in a currency different from your bank’s currency, your bank may apply dynamic currency conversion (DCC) fees. These fees vary by provider and are independent of Capital.com.

To avoid unnecessary conversion costs, consider funding your account in the same currency as your bank account. Contact us for more details on DCC.

Knock-out option fees

Knock-out options are a structured risk product where you can set a predefined knock-out level that automatically closes the trade if reached.

When trading knock-outs, there are three key fees to consider:

1. Spread

- Like CFDs, you’ll be charged a spread on each knock-out trade you place.

- If you think a market will rise in value and open an ‘Up’ knock-out, your entry level is based on the ask (buy) price of the underlying market.

- If you think a market will fall in value and open a ‘Down’ knock-out, your entry level is based on the bid (sell) price of the underlying market.

- When you exit each trade, the opposite side of the market is used. EG, for ‘Up’ your close price will be based on the bid price, and for ‘Down’ it will be based on the ask price of the underlying market.

- You can view the exact spread applied to your knock-out trade by clicking on ‘Order summary’ in the deal ticket.

2. Knock-out fee (charged only if the knock-out level is hit)

- If the price goes against you and reaches your chosen knock-out level, the trade automatically closes, and you’ll be charged a knock-out fee.

- This is calculated as a small percentage of the knock-out price, for example, 0.02%. The calculation will vary per asset class.

- If the knock-out level is not reached, this fee is refunded to you.

3. Overnight adjustment (applied only if the trade is held overnight)

- If you hold a knock-out trade past market close, an overnight adjustment will be applied.

- This adjustment is based on the underlying price, which represents your market exposure.

- It’s calculated as: Number of options × underlying price × overnight rate

- The overnight rate is determined by:

- For Up positions (if you think the price will rise): minus benchmark rate (ie, SONIA or SOFR), minus our daily fixed admin fee

- For Down positions (if you think the price will fall): +benchmark rate minus our daily fixed admin fee

- If the rate is negative, you pay interest to hold the position overnight.

- If the rate is positive, you receive interest for holding the position overnight.

4. FX conversion fee

If your account’s base currency differs from the currency of the underlying market, an FX conversion may occur when you open and/or close a knock-out trade. This FX conversion is separate from the knock-out fee.

The conversion uses the prevailing platform exchange rate at the time of the transaction, in line with how currency conversions work for other instruments.

Important: When no FX conversion occurs (for example, a EUR account trading a EUR-denominated index), the KO behaves economically like a CFD, with no FX impact.

When an FX conversion does occur, movements in the exchange rate can affect the value of your knock-out trade at opening/ closing, which in turn affect your trade’s final result when converted into your account’s base currency.

At Capital.com, no FX conversion markup is charged on knock-out options. This means that while a currency conversion rate may be applied, no additional FX conversion cost is added on top of that rate.

Example 1: Up option (held overnight, then knock-out level hit)

- You think the Germany 40 will rise in value, and open an ‘Up’ knock-out on the index, with the knock-out price at 10,000.

- You set your knock-out level at 9,900.

- You hold the position overnight, after which the price falls, hits the knock-out level, and your position is closed.

Fee calculations

1. Spread (included in the quoted price)

In this example, let’s say the underlying Capital.com Germany 40 CFD bid/ask is 19,898/19,900.

Since you’re trading an ‘Up’ knock-out, your knock-out is priced from the ask side – 19,900 – meaning you enter at a level slightly above the mid-market price. The 2-point difference between bid and ask reflects the embedded spread.

So, your knock-out trade incurs a spread cost of €2 (2 index points × €1 per point).

2. Knock-out fee (since the knock-out level was hit): €2 (based on an example rate of 0.02% of the knock-out price)

3.. Overnight adjustment (as the position was held overnight)

- The underlying ask price is 19,900.

- The overnight rate for ‘Up’ positions:

- Benchmark rate = 0.01393% (daily)

- Current admin fee = 0.01111% (daily)

- Total overnight rate = -0.02504%

Overnight adjustment calculation:

1 × 19,900 × (-0.02504%) = -€4.98 debited

Final costs:

- Spread: €2 (embedded in quoted price)

- Knock-out fee: €2

- Overnight adjustment: €4.98

- Total cost = €8.98

Example 2: Down option (held overnight, then knock-out level hit)

- You think the Germany 40 will fall in value, and open a ‘Down’ knock-out on the index, with the knock-out price at 10,000.

- You set your knock-out level at 10,100.

- You hold the position overnight, after which the price rises, hits the knock-out level, and the position is closed.

Fee calculations

1. Spread (included in the quoted price)

Again, the underlying bid/ask spread is 19,898/19,900. Since you’re trading a ‘Down’ knock-out, your knock-out is priced from the bid side – 19,898 – meaning you enter at a level slightly below the mid-market price.

As with the ‘Up’ example, your knock-out trade incurs a spread cost of €2 (2 index points × €1 per point).

2. Knock-out fee (since the knock-out level was hit): €2 (0.02% of the knock-out price)

3. Overnight adjustment (as the position was held overnight)

- The underlying price is 19,898.

- The overnight rate for Down positions:

- Benchmark rate = 0.01393% (daily)

- Current admin fee = 0.01111% (daily)

- Total overnight rate = +0.00282%

Overnight adjustment calculation:

Final costs:

- Spread: €2

- Knock-out fee: €2

- Overnight adjustment (credit received): -€0.56

- Total cost = €3.44

Please note that conversion fees as described above apply to both traditional CFDs and knock-out options.