US PCE data to test Fed’s ability to keep cutting rates

The PCE data will test the Fed's ability to cut rates further.

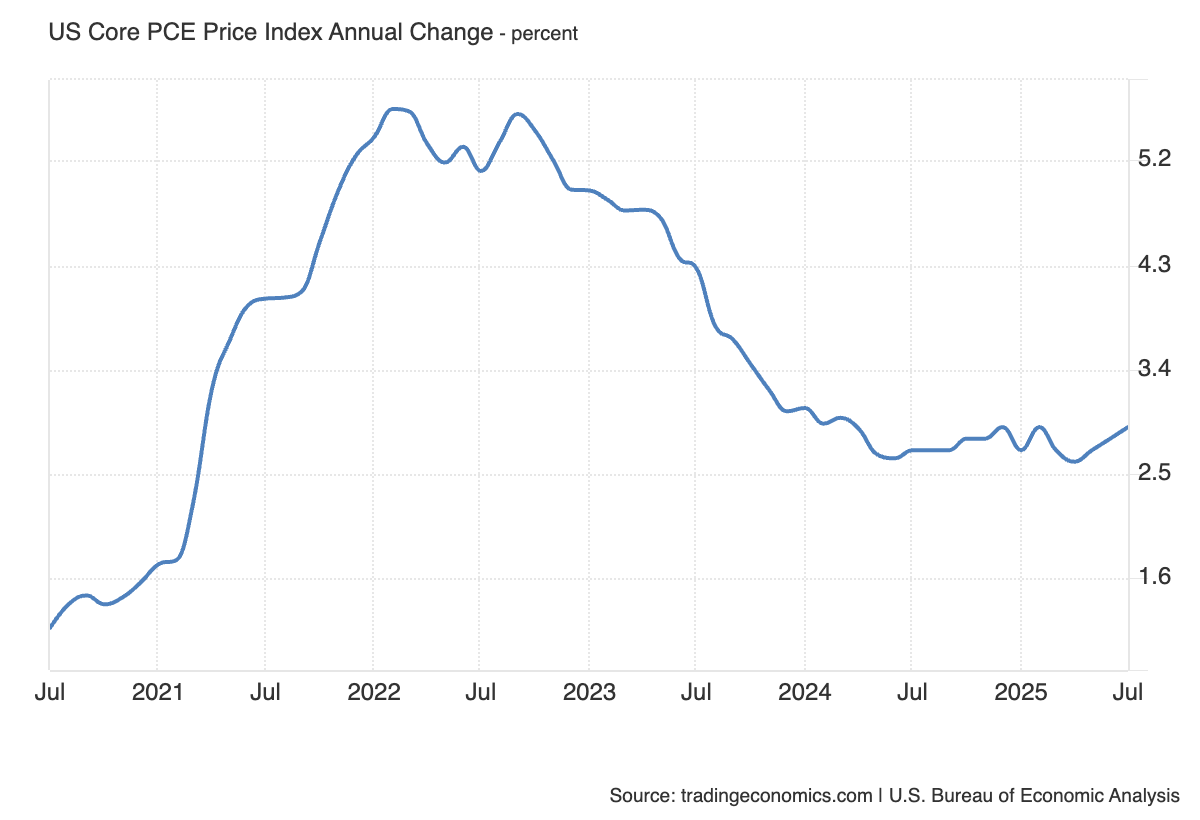

The latest US Personal Consumption Expenditures (PCE) inflation numbers are due on Friday, 26 September, with the release expected to confirm steady price pressures through August.

Forecasters predict steady inflation in August

Forecasts suggest core PCE will rise by 0.2 per cent month-on-month, a softer increase compared to the prior reading, with the annualised rate sitting around 2.5 per cent. On a year-on-year basis, core PCE is projected to increase by 2.9 per cent, in line with a month earlier. These numbers imply that inflation remains on a steady path but still above the Federal Reserve’s 2 per cent target, which has arguably become reanchored in the high 2 per cent range.

(Source: Trading Economics)

(Source: Trading Economics)

Services and goods inflation in focus

Markets will be watching closely how services and goods inflation contribute to the outcome. Services inflation has been the key driver of persistently elevated price growth, fuelled by resilient consumer demand in recent years. Goods inflation, on the other hand, has shown signs of picking up, reflecting the pass-through of tariffs into consumer prices. Together, these components will provide insight into the underlying drivers of inflationary pressures.

PCE data to test the case for October and December rate cuts

The release will be assessed in the context of last week’s Federal Reserve decision, which delivered a rate cut and signalled the likelihood of further reductions in October and December. Despite this dovish tilt, policymakers struck a cautious tone, highlighting upside risks to inflation as tariffs continue to filter through the economy. That caution has been echoed by Fed officials this week, who acknowledged the potential need for additional easing but stressed the importance of remaining vigilant against lingering price pressures.

Wall Street and US Dollar confront asymmetric risks

Interest rate markets currently assign a 90 per cent probability of another cut in November and a 75 per cent chance of a move in December. Given market pricing, the risk to markets is asymmetric. A stronger-than-expected inflation figure, particularly if the core annual figure pushes above 3 per cent, could lead investors to doubt the Fed’s capacity to cut rates as aggressively as currently priced. An outcome broadly in line with expectations would reinforce existing bets on further easing, likely offering a boost to equity markets while exerting downward pressure on the US Dollar.