The RBA expected to keep rates on hold as inflation fires up again

The RBA is likely to keep rates on hold at 3.60% as inflation shows signs of accelerating.

The RBA is expected to keep the cash rate on hold at 3.60% when it meets on Tuesday, 4th of November as Australian inflation re-accelerates.

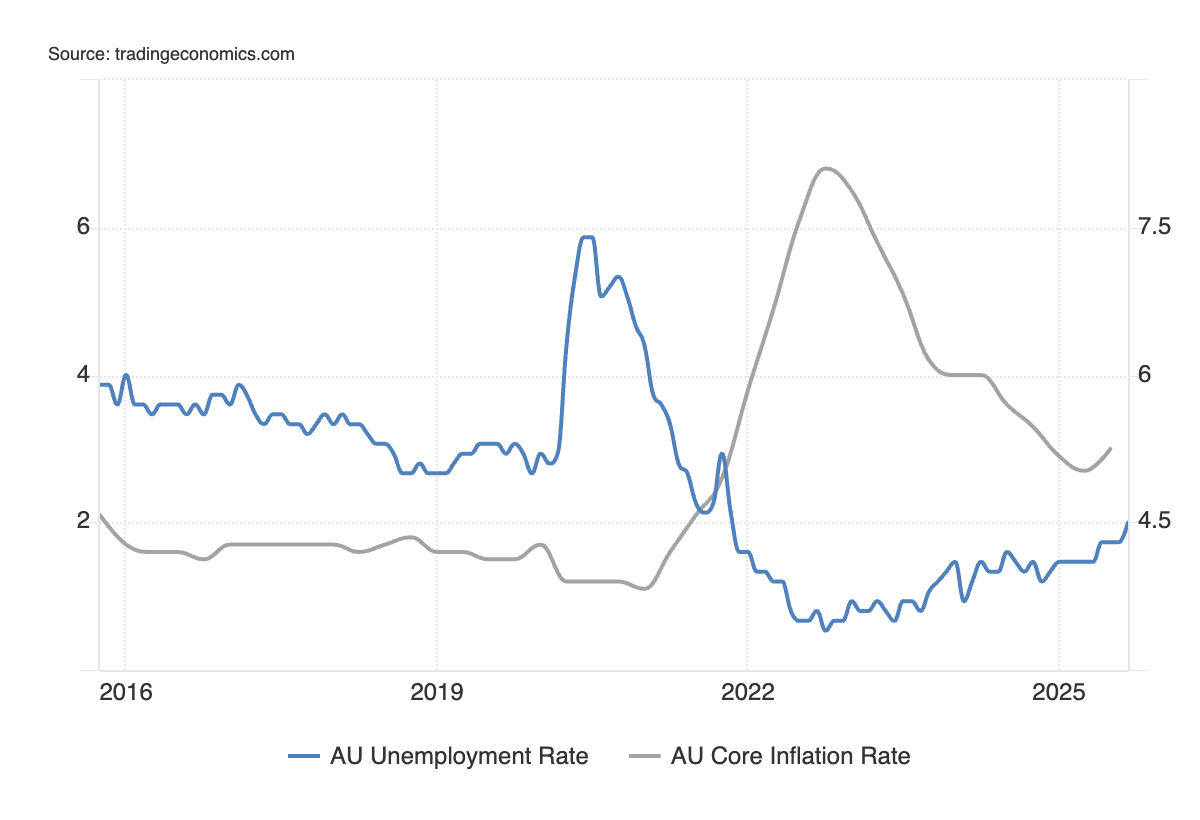

The RBA balances risks of rising inflation and jobless rate

Official CPI data all but extinguished any expectation of an RBA cut this month. The inflation figures for the September quarter saw a surprise jump in both headline and underlying prices, pushing both above the central bank’s target. Headline inflation lifted to 3.2%, largely due to the rolling off of electricity subsidies in several major Australian states. However, the RBA’s preferred measure of price growth, annual trimmed mean CPI, leapt to 3.0% – far exceeding the 2.7% estimate.

The dynamic suggests policy may not be as restrictive as previously thought, with demand too strong for an economy hampered by weak productivity growth. Although economic activity remains relatively tepid, despite a lift in consumer activity recently as higher real wages and rate cuts support households, aggregate demand remains in excess of aggregate supply. That’s putting upward pressure on inflation and likely making the RBA wary of compounding the problem by cutting rates further.

The rise in inflation is happening even as evidence mounts of a weaker labour market. Market participants had come to expect a high chance of another cut before the end of 2026 after September’s labour force data revealed a surprise rise to 4.5%. The simultaneous rise in inflation and the unemployment rate is creating an invidious situation for the RBA, with the central bank being pulled in opposite directions by both sides of its mandate.

(Source: Trading Economics)

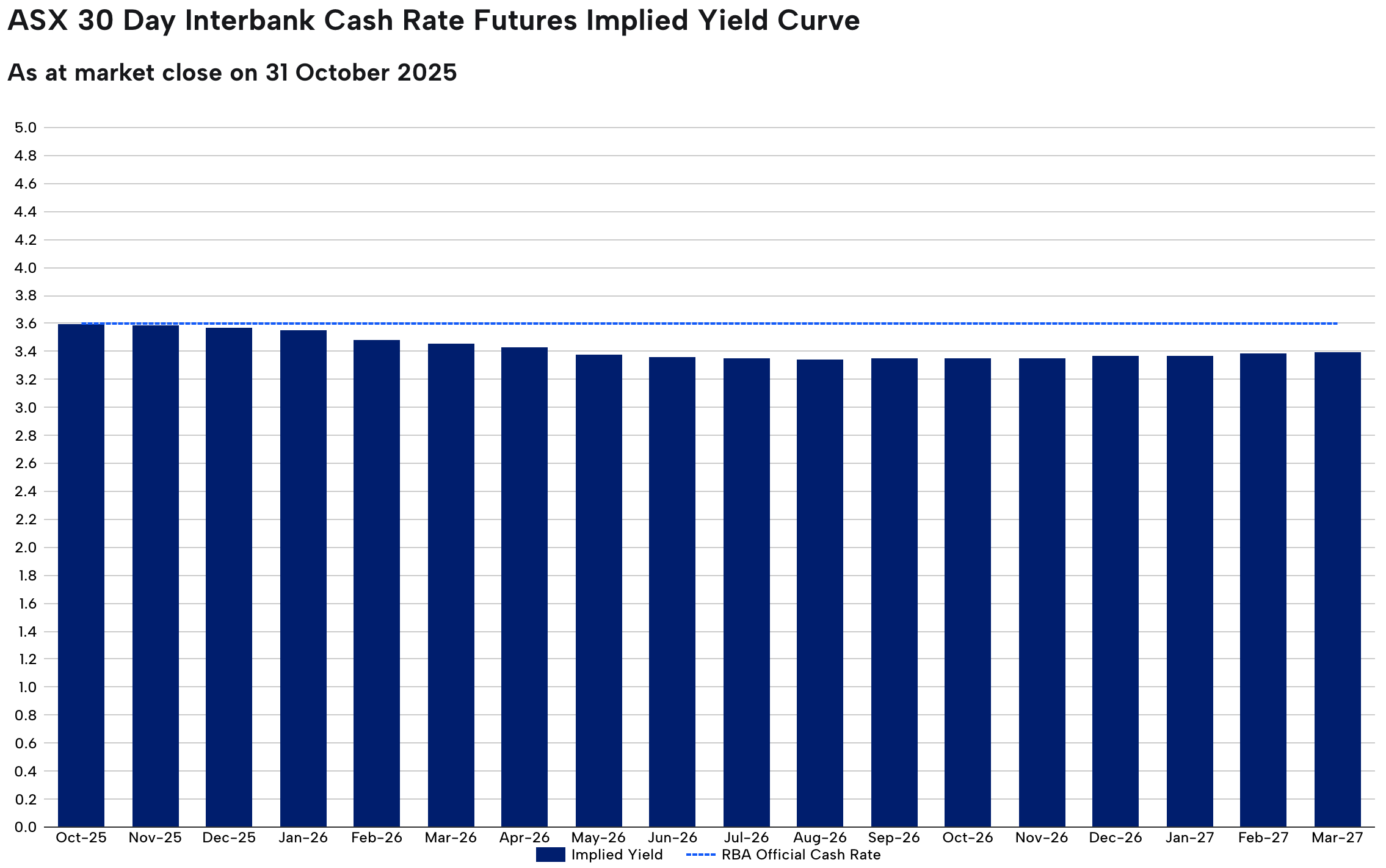

The markets price-out rate cuts before the end of 2025

The hot inflation data has led the markets to price-out further rate cuts from the RBA before the end of 2025. Doubts have now emerged about the central bank’s capacity to lower rates further, with another cut still baked-in to the curve, but not until May 2026.

(Source: ASX)

The RBA updates its Statement on Monetary Policy at this meeting, with a focus on the central bank’s projections for trimmed mean CPI and the unemployment rate. The August SOMP revealed the RBA expected inflation and the jobless rate to steady at 2.6% and 4.3%, respectively, from the end of 2025 onwards, with the forecasts the basis for future rate cuts. The data shows both have already been exceeded and could be trending in the wrong direction, leading the markets to price-out imminent cuts. Market participants will be homing in on the refreshed projections to assess how the RBA views the current balance of risks and frame the RBA’s future reaction function.

A recovering US Dollar holds back the AUD/USD

The falling rate cut probabilities and easing trade tensions between the US and China are meaningful tailwinds for the Australian Dollar. However, a resurgent US Dollar is limiting the upside of the AUD/USD. Following a break-out of a short-term trend channel, the pair failed to hold above the 66-handle. A confluence of support appears around 0.6530, a break of which could open up further downside for the AUD/USD. Meanwhile, resistance sits just below 0.6630, with a break signalling a potential continuation of the 2025 uptrend.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)