Risk-off prevails as Trump-tariffs raise risks to global growth

Global markets turn risk-off as Trump imposes new tariffs on Mexico, Canada, and China.

The markets have tariffs on their mind as a burgeoning global trade war develops. Wall Street pared its advance on Friday after US President Donald Trump announced 25% tariffs on Mexico and Canada, for what Trump alleges is their role in the fentanyl trade, while he also slapped 10% tariffs on China. Canada has already responded in kind with its own tariffs, while Mexico is reportedly considering doing the same, and it's almost certain China will also retaliate. The developments are a major risk to global economic activity and short-term inflationary pressures in the United States, with the biggest fear that this will set off a vicious cycle of tit-for-tat trade measures that will dramatically impact global growth potential and investment returns.

How have the markets responded to the tariff announcement?

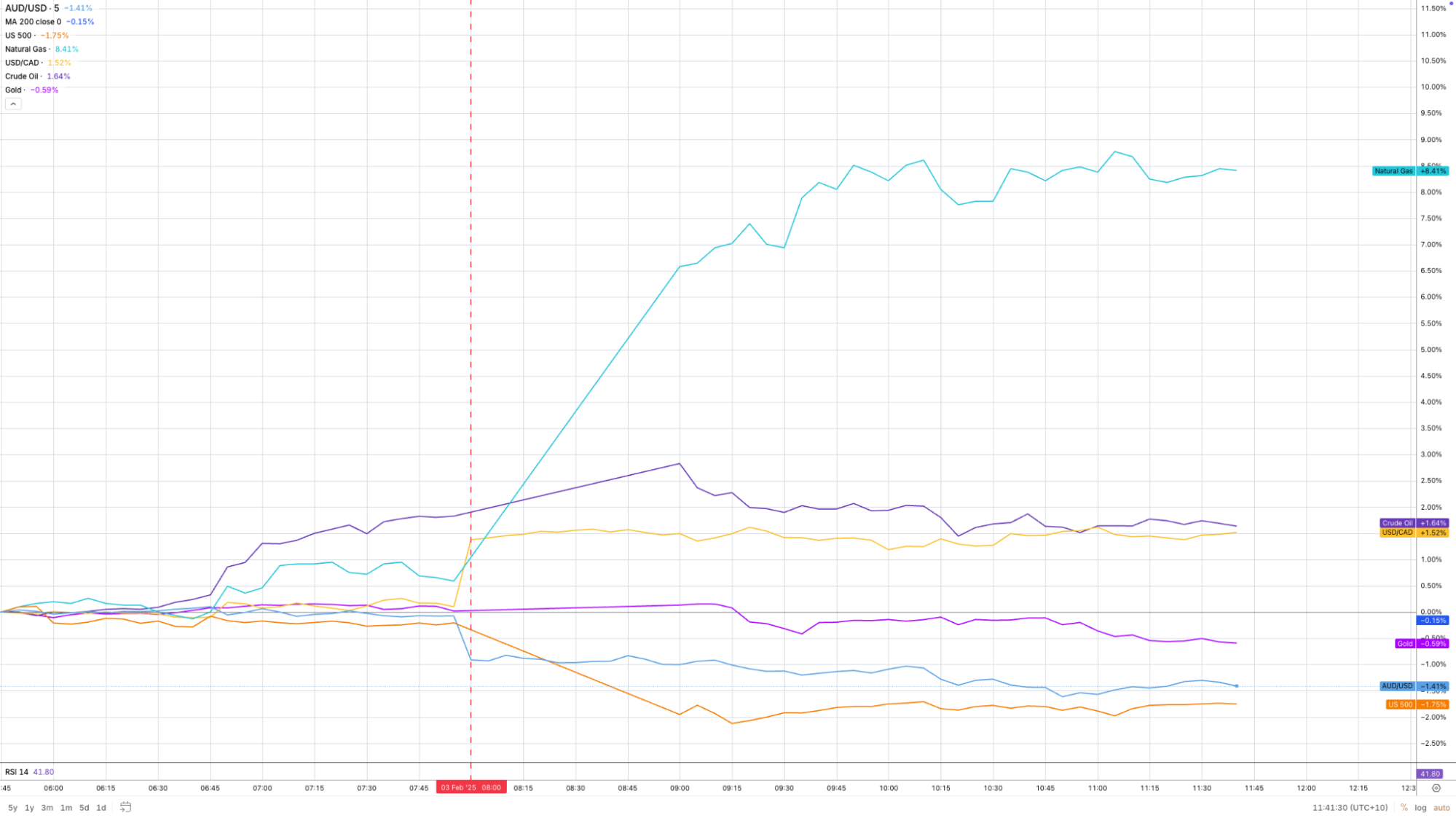

The early reaction is to sell risk. The Canadian Dollar has hit a more than 20-year low; the Aussie Dollar is near a 5 year low, so is the Kiwi Dollar, and the Mexican Peso has plunged. The Yen and US Dollar are higher as the markets turn “risk off”. Stocks are following suit in early Asian trade. Futures are tumbling as well, pointing to another big loss for US markets to kick-off the new week after the DeepSeek sell-off. Energy prices are largely higher, however, because this risks Canadian energy exports to the US, and will potentially lead to lower output. That’s why natural gas and oil prices are higher today despite the impact of tariffs on global growth.

(Past performance is not a reliable indicator of future results)

Tariffs raises short-term inflation risks, long-term growth risks

A sudden spike in import costs will likely feed into inflation directly and indirectly as the impacts of higher prices filter through the economy. However, it should be noted a tariff is a one of change in the price level. Inflation is defined as a constant increase in the rate of change in prices. So this will imply a short-term spike in inflation, before price growth reverts to its underlying drivers. The bigger, structural issue for the economy is related to growth. More expensive input prices raises costs across the economy, eroding profit margins for businesses and reducing consumption amongst households. This lowers demand via weaker consumption and less business investment, all else equal, lowering employment growth.

Higher tariffs risk delaying US Federal Reserve rate cuts

Because of the short-term impacts on prices but the longer term impacts on US growth potential, what these and future tariffs mean for US rates depends on the referenced timeline and second order consequences of them. Initially, tariffs will likely lower the prospects of further rate cuts from the Fed because the central bank will have to deal with short-term price shocks. However, because of the drag on growth from their imposition, like in 2018/19, the consequences on economic activity may see a renewed cutting cycle as growth weakens and the economy works through the base effects of higher prices.

US equities at risk of further downside as tariffs rise

Tariffs will hurt the outlook for US equity prices. It’s bad for earnings, because it’s a squeeze on corporate margins and growth. It’s also bad for valuations because it increases volatility and lowers the odds of a rate cut from the Fed going forward. Cyclicals ought to perform worse, so should export sensitive economies, especially those exposed to Asia. One counter argument not to worry too much about the impact of tariffs on equities is that, due to the fact Trump uses the stock market as a barometer of his success, significant weakness in equity prices will force him to back-off on tariffs. This was arguably true in his first term; if he acts the same way again this time around, it would help restore confidence that the worst of the trade-war will not come to fruition.