Renewed US-China trade tensions re-inflame volatility as risk assets tumble

A spike in US and China trade tensions over rare earths has ignited fresh volatility.

Wall Street and oil tumbles while gold pops on fresh US-China trade tensions

The markets have looked primed for a shock for a while. The hallmarks of a market vulnerable to a sharp drawdown were there. Low volatility, high valuations, stretched positioning, complacency. The move wasn’t inevitable. But when markets get so bullish, they don’t respond to negative surprises kindly. As a result, Wall Street plunged as risk appetite turned, with tech stocks exposed to rare earth curbs underperforming. The US Dollar retraced against G4 counterparts but growth currencies, especially those exposed to China, tumbled. Oil prices also sank more than 5%, hitting levels not seen since the last trade war flare up. Meanwhile, gold bounced back towards record highs.

(Source: Trading View)

(Source: Trading View)

(Past performance is not a reliable indicator of future results)

Trade war risks may go silent but they never disappear

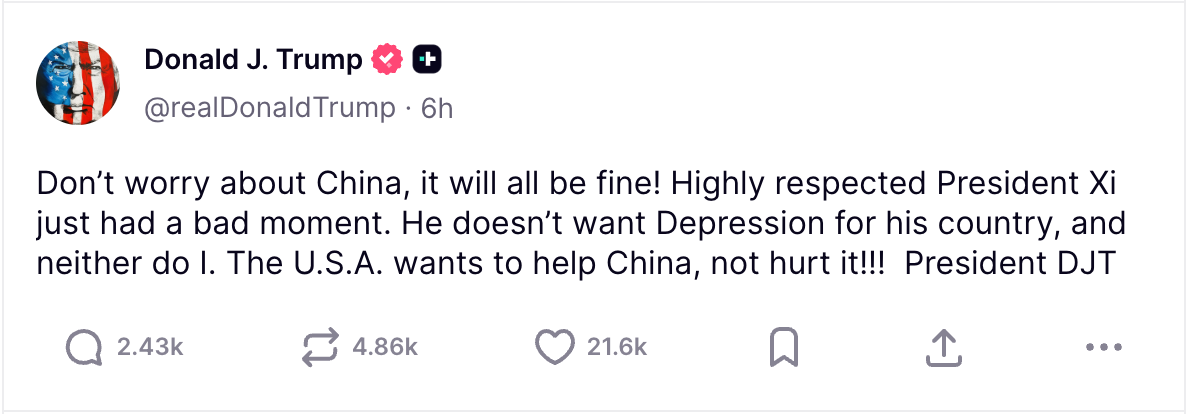

The latest flare up shows the ever present risk of US and China trade tensions. The curious element of this episode is that it was provoked by China’s actions. The catalyst was further curbs on rare earth exports: critical elements in critical technology, ranging from iPhones to data centres. Although it was not responded to immediately by the markets when the ban was announced last week, it represents a big shot across the bow. In fact, it was the ban on rare earth exports that all but forced the Trump administration to back off its mega tariff threats after Liberation Day. The move by China has led to very bellicose rhetoric from the Trump administration, including threats of new tariffs and the cancellation of a meeting with US President Donald Trump and Chinese President Xi. Although, in a sign of a potential olive branch, President Trump has shared a conciliatory message on Truth Social that has eased fears of spiralling tensions.

(Source: @realDonaldTrump)

(Source: @realDonaldTrump)

The biggest issue for the market now is whether tit-for-tat tariff threats start again and whether a higher rate – 100% across the board – of tariffs will be implemented on November 1 by the US. It could be this is all brinkmanship and the markets are back to the “TACO trade”, meaning the theatre will be short-lived. Initial price action at the Asia open suggests this could be the case. Even if it is, it could come with a pain that goes beyond the pullback of an overbought and expensive stock market. As was seen after the Liberation Day tariffs, while many imposts were eventually unwound or put on pause, it did result in a material (albeit fairly short) hit to the US economy. The fresh tit-for-tat reintroduces a level of uncertainty that could impact consumption, investment and employment decisions, slowing growth for a period – something that has to be discounted in asset prices.

Traders also confront backlog of US data, looming US earnings season

As investors work through this new chapter in the US-China rivalry, there are other events in the week ahead that will need to be tackled and digested. The US Government shutdown is dragging on and the markets are getting itchy for the data required to inform US Fed policy expectations. US earnings season also picks up in earnest, with the banks, as always, the first cabs off the rank. Before this new trade induced volatility, the main focuses for the markets were when and how deeply the Fed would cut rates and whether US tech stocks would continue to deliver gangbuster earnings. Although both issues may be drowned out this week by trade uncertainty, it’s likely these two variables will remain the most important for markets over time.