Market Mondays: US shutdown, Japan’s leadership change and France’s political instability

US data delay leaves markets focused on FOMC speakers and news headline with Japan in focus after their leadership change

Government shutdown delays key data releases

Markets have largely looked through the U.S. government shutdown so far, treating it as a peripheral risk rather than a core macro shock. History helps: past episodes have rarely derailed equities for long. The practical complication this time is the likely blackout of official data just as investors were leaning on labour readings to validate a dovish Fed path. If Friday’s absent nonfarm payrolls and subsequent releases are delayed further, the policy reaction function becomes harder to read, and a modest risk premium is warranted. There is also a low-probability tail risk that political rhetoric around permanent layoffs turns a temporary disruption into a small growth shock, but for now the tape has taken the view that the underlying U.S. economy remains intact.

In the absence of hard data, markets are forced to infer. Private indicators and survey evidence step into the spotlight, with last week’s ADP reading pointing to contraction and jolting rate expectations. Traders typically discount ADP in favour of the official BLS figures that follow, but with that anchor potentially missing, the private print has had to do more work than usual. Fed officials have been clear that one data point doesn’t set policy; they judge trends over time. Still, pricing now implies a very high likelihood of a quarter-point cut at the end of the month and meaningful odds of additional easing by year-end, alongside a view that the cycle’s trough rate could fall below three percent. That combination—softer labour signals and a data vacuum—is enough to keep volatility elevated even as indices probe record territory.

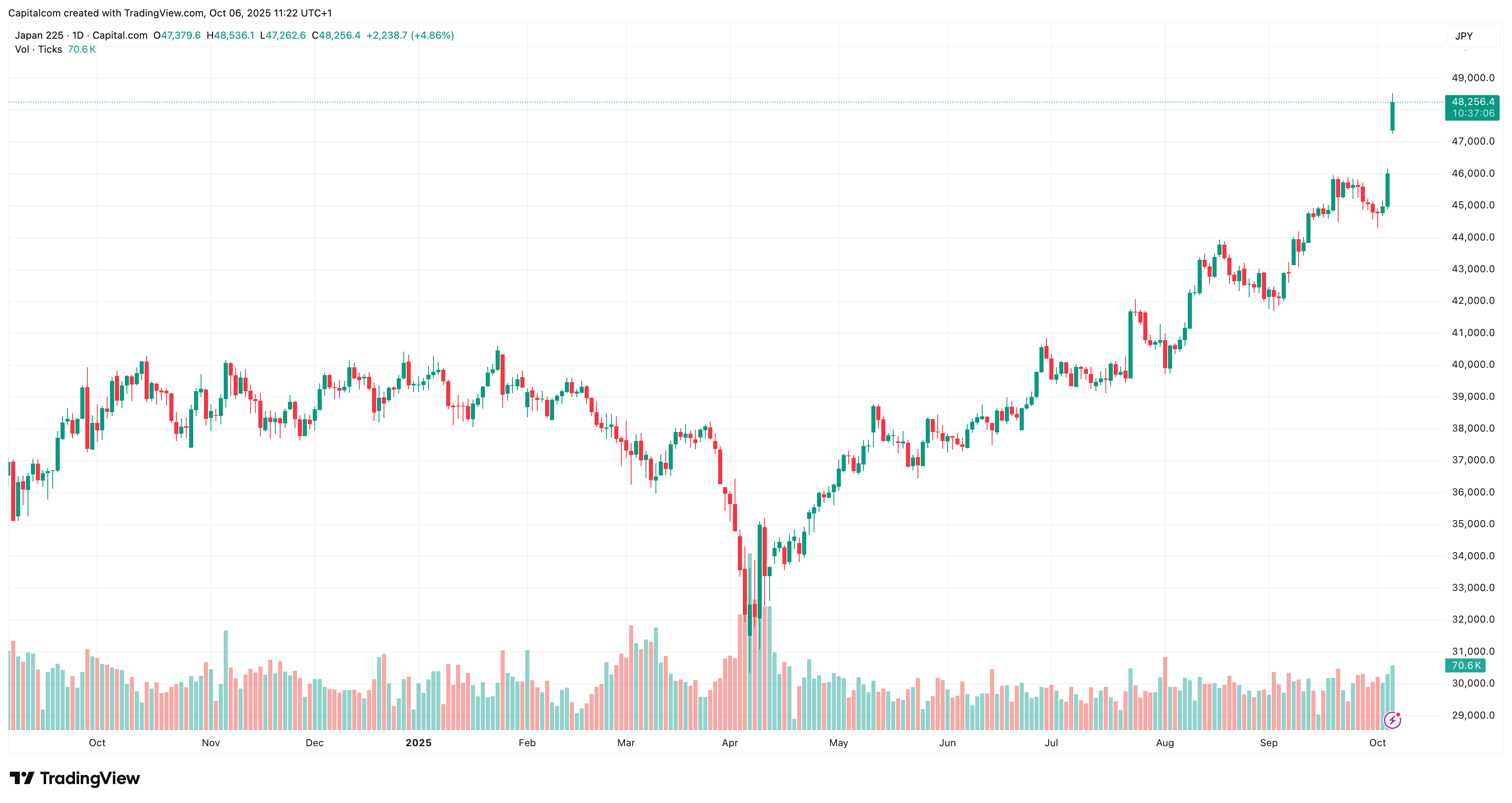

Japan leadership change sparks volatility

The bigger story of the last twenty-four hours has been Japan. A pro-stimulus turn in political leadership and talk of sizeable fiscal support for strategic sectors—from semiconductors and nuclear to AI—have supercharged risk appetite in Tokyo. Equities gapped to record highs, the yen weakened as real-yield concerns and fiscal-sustainability questions resurfaced, and the long end of the JGB curve jumped even as the front end stayed anchored by a cautious central bank. The message for global markets is straightforward: Japan’s policy mix still tilts toward growth support, and that spills over to cyclicals, exporters and the broader capex complex worldwide.

Nikkei 225 daily chart

Past performance is not a reliable indicator of future results.

Gold continues to shine

Gold sits at the intersection of these narratives. A murkier U.S. data path lowers conviction around higher real rates, geopolitical and political noise sustains demand for portfolio insurance, and a softer yen alongside bouts of dollar strength has not been enough to derail inflows. The metal’s bid has been reinforced by persistent central-bank purchases and, in silver’s case, by tightening industrial fundamentals. Silver has benefited from the same safe-haven impulse as gold while drawing incremental demand from electrification and electronics, against a supply base that has struggled to expand after years of under-investment. The result is a powerful, two-engine rally that has punished attempts to fade momentum.

France’s political instability continues

Europe provided a contrasting note. French politics returned to the foreground with reports of another prime-ministerial resignation only weeks after the latest appointment, underlining the difficulties of stabilising fiscal and policy agendas. The CAC 40 slipped on the headlines and French yields moved higher as investors priced a thicker political risk premium, while the euro traded softly against a firmer dollar. The episode is a reminder that politics remains a live variable across the region even as the macro backdrop has improved this year.

Energy rounded out the morning with a technical bounce. Crude recovered after last week’s break lower as the latest OPEC+ decision on output increases proved smaller than rumoured. The broader balance between abundant supply and a patchy demand pulse still argues for two-way trade, but the reversal from oversold levels was enough to steady the complex into the new week.

The immediate question for traders is one of timing rather than direction. If Washington resolves the shutdown quickly and the data calendar normalises, the market can re-anchor expectations in a cleaner way and let earnings season carry the load. If the blackout persists, price action will remain headline-driven, with private surveys, Fed communication and auction metrics doing more of the signalling than usual. Valuations are rich, momentum is intact, and participation is uneven; without fresh confirmation from hard data, the path higher likely becomes choppier, not impossible. For now, the shutdown sits at the periphery while the core of the U.S. economy—and an increasingly consequential Japan—drives the narrative.