Market Mondays: Fed speculation, AI-ROI, and Nvidia results shape a likely volatile week

The markets stare down a deluge of US data and Nvidia's quarterly results as the markets grapple with the probabilities of a US Federal Reserve rate cut in December.

Markets are entering the week clouded by rising uncertainty across macro and micro fronts, with traders parsing a shifting US rate outlook, fresh doubts about AI valuations, and a potentially market-moving earnings report from Nvidia.

Markets reprice the Fed: December cut now a coin toss

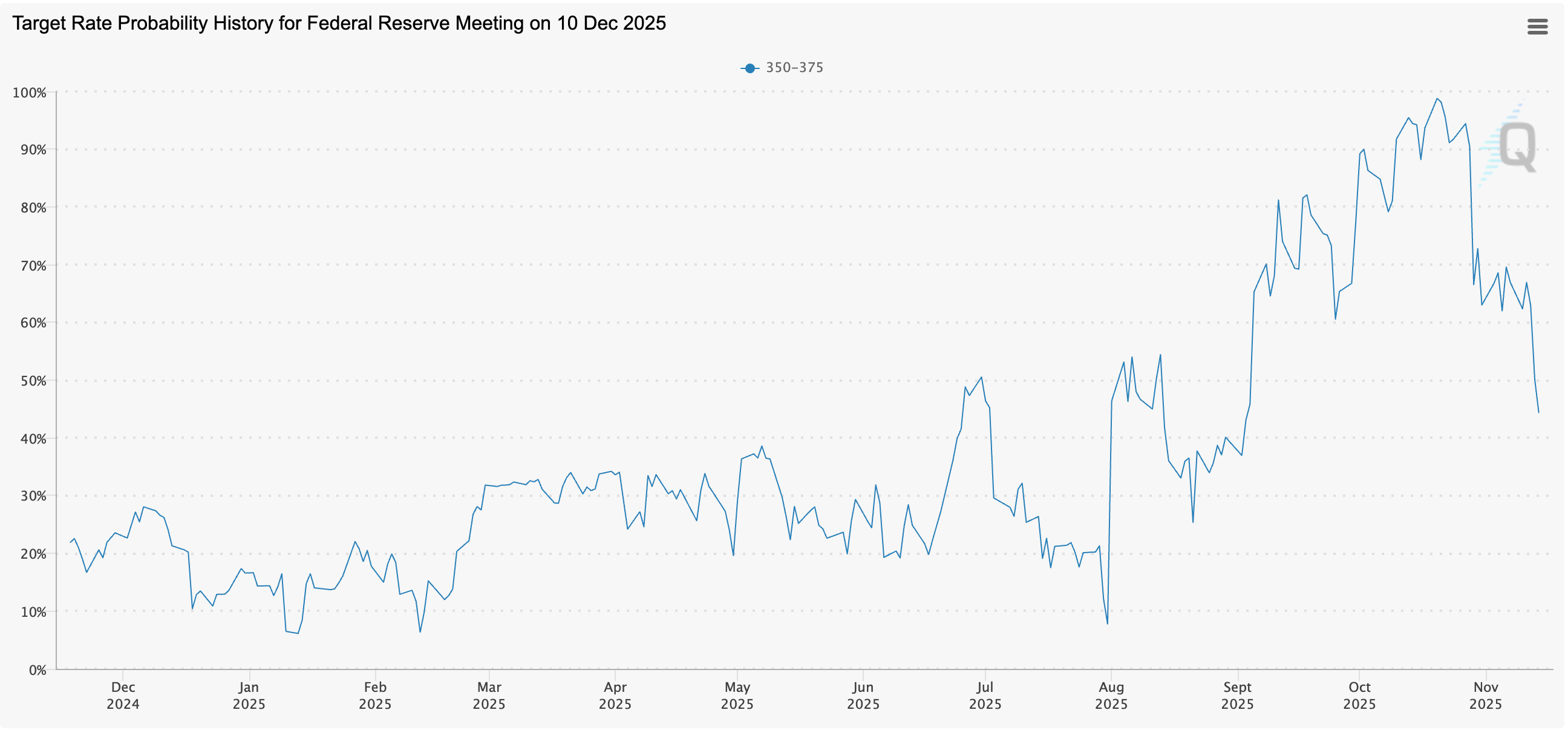

A core driver of volatility is the recalibration of US Federal Reserve rate expectations. Just weeks ago, markets were pricing a near 98% chance of a December cut. That probability has now collapsed to around 43%, with a hold priced at 56%, according to CME FedWatch.

(Source: CME Group)

This dramatic shift was catalysed by Jerome Powell’s now-famous line: “A December rate cut is not a foregone conclusion.” Since then, Fed speakers have delivered broadly hawkish rhetoric, pointing to persistent inflation risks. While doves remain concerned about the softening labour market, the consensus appears to be one of caution, with policymakers seeking to preserve optionality heading into year-end.

Equities have responded accordingly. The Nasdaq has lost momentum, retreating from record highs posted in late October. The narrative of looser monetary policy that fuelled recent gains is being challenged, weighing on risk assets and buoying the US Dollar.

AI valuations under scrutiny ahead of Nvidia earnings

The second key story is the AI-ROI trade. As investor enthusiasm for artificial intelligence cools down, markets are grappling with whether current valuations—especially for the Magnificent Seven—are justified by earnings and productivity growth.

The forward price-to-earnings ratio for the S&P 500 has returned to levels seen during the pandemic and dot-com bubbles. While earnings growth this quarter is tracking a robust 13.1%, the concern is that these results are being used to justify increasingly rich valuations, particularly in the tech sector.

All eyes now turn to Nvidia. The company’s fiscal Q4 results will serve as a litmus test for the AI trade, with analysts expecting EPS of $0.97. Key questions include: Are hyperscalers still investing aggressively in AI infrastructure? How strong is demand for Nvidia’s new Blackwell and Rubin chips? And are China export restrictions beginning to bite?

Nvidia’s stock has pulled back from recent highs, potentially lowering the bar for a positive surprise. A break above $210 would suggest the structural uptrend remains intact. Conversely, a failure to meet elevated expectations could deepen the current correction.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)

Macro data flood resumes post-shutdown

US data releases resume in full this week after delays caused by the government shutdown. Non-farm payrolls for September will be in focus, though they are considered dated. More relevant are forward-looking inflation signals, which will guide the Fed’s path.

A key debate is forming over the nature of recent labour market weakness. Is it cyclical, structural, or driven by factors like immigration and AI automation? The policy implications are significant. A supply-side constraint (via immigration) or positive productivity shock (via AI) may justify a different monetary response than a traditional slowdown in economic activity.

Market pricing suggests scepticism that the Fed has the political will to keep policy tight enough to restore inflation to target. This could reinforce a "run it hot" regime—where fiscal expansion and mild monetary easing co-exist—adding to upside risks for inflation in 2025.

Technical setup: Still a pullback, not yet a reversal

Technically, US indices still appear to be in consolidation rather than full-blown reversal. The Nasdaq is testing a key support level near 24,000. A breach of this zone would mark a lower low and threaten the uptrend. The S&P 500 is showing a bullish wedge formation, with higher lows offering tentative optimism for trend continuation—though conviction is waning.

The US dollar looks poised to regain ground, with DXY potentially breaking higher after a 10% drawdown through much of the year. A firm close above 100 on the index could signal a return to dollar strength, especially as the Fed recalibrates its tone and US exceptionalism narratives regain momentum.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)

Global FX: BOJ credibility under fire, UK policy on watch

USD/JPY has broken key technical resistance, driven by the BoJ’s reluctance to normalise policy even as inflation pressures mount. Japan’s fiscal expansion under new leadership has only added fuel to the move. Unless the BoJ hardens its stance, the yen is at risk of continued depreciation.

In the UK, weak GDP and labour data, combined with dovish BoE commentary, have set the stage for rate cuts in 2024. The pound and FTSE were hit late last week after reports of a fiscally conservative budget reversal—highlighting investor concerns over long-term UK fiscal sustainability.

Despite the sell-off, the FTSE remains in a technical uptrend. Key levels to watch include 9,575 on the downside and 9,930 on the upside. A break of the latter would open the door to 10,000—a psychologically significant milestone for the index.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)