FOMC tipped to keep rates on hold as political pressure mounts

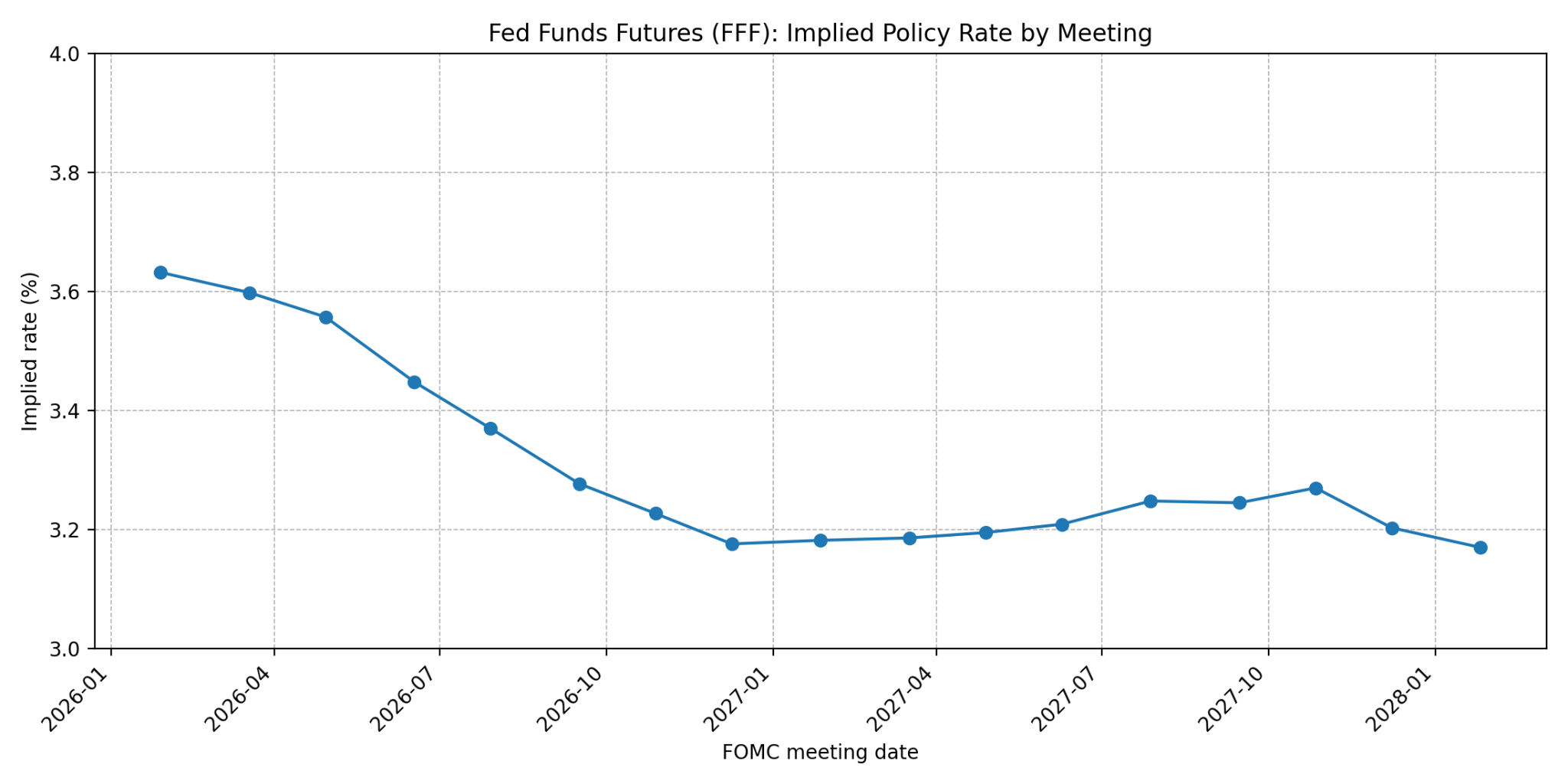

The markets are pricing in that the Fed will begin an extended pause at its first meeting of 2026.

The FOMC meets for the first time in 2026 and is widely expected to keep policy unchanged at 3.50% to 3.75%.

Rates tipped to remain on hold amid strong growth, sticky inflation

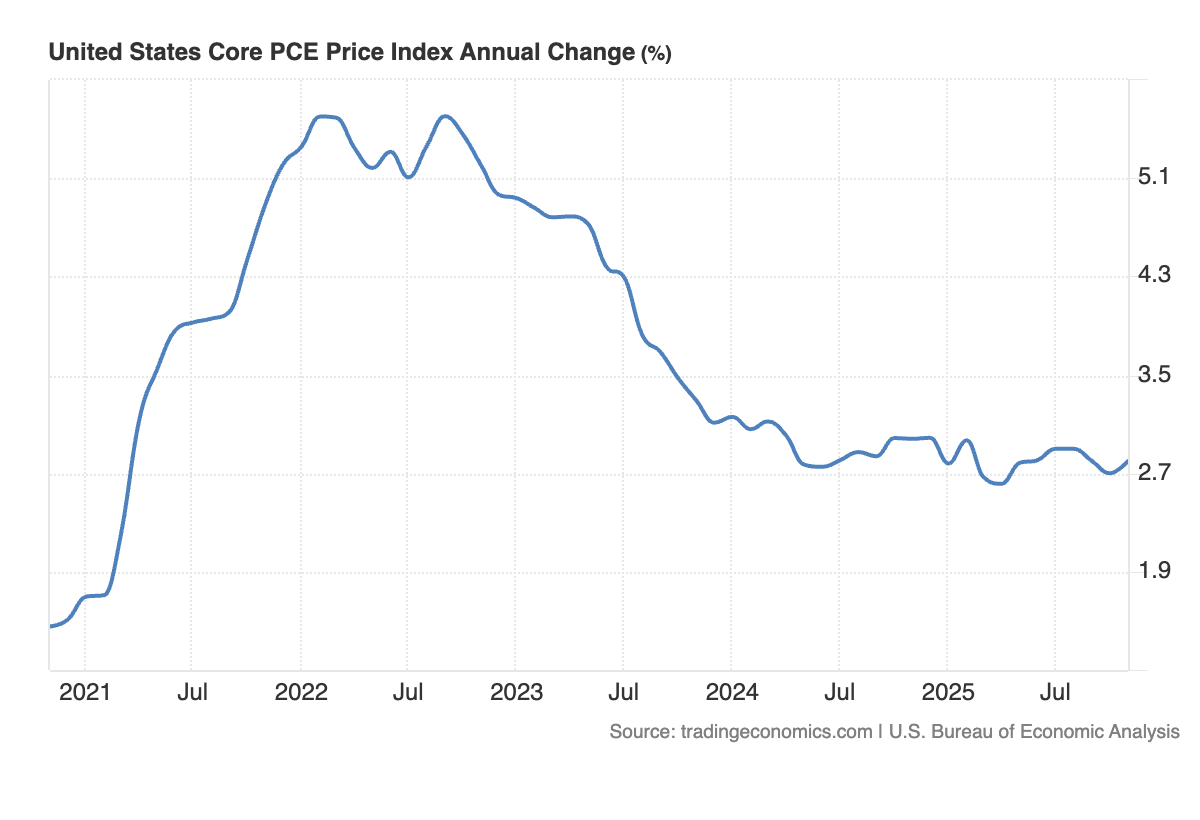

US rates futures imply that the US Federal Reserve is all but certain to keep policy unchanged when its first meeting of 2026 concludes on January 28. A majority of FOMC members are expected to vote for a hold, with the probable exception the Trump-appointed Stephen Miran, who is likely to vote for a cut. The decision comes amidst signs of strong economic activity, a resilient labour market, and sticky inflation in the United States. The final GDP reading for Q3 showed upwardly revised growth of 4.4% q/q, the December Non-Farm Payrolls report revealed sluggish jobs growth but a drop in the unemployment rate to 4.4%, and, most pertinently, November’s PCE Index data revealed a lift in core inflation to 2.8%.

(Source: Trading Economics)

(Source: Trading Economics)

The markets price-in an extended pause in US rates

Following gradual rate cuts in the second half of 2026, the markets are pricing in the US Federal Reserve will begin an extended pause at this meeting. The Fed is expected to maintain similar guidance to what it adopted at its final meeting last year, where it emphasised downside risks to the labour market amid elevated but stable inflation. However, it’s likely to frame its decision to hold rates around a wait-and-see approach to policy to assess how inflation evolves and the jobs market responds to previous cuts.

Currently, the markets are pricing in that the Fed could keep policy unchanged until the middle of 2026, with the next cut not fully baked-in until the second half of the year. The odds further cuts from there have diminished in recent weeks in response to solid data and elevated inflation. Heading into the January meeting, the rates curve is implying an 80% chance of two more cuts before the end of the cutting cycle.

Given no move is expected from the Fed and there are no updated economic projections at this meeting, most of the informational value out of this FOMC meeting will be in Chairperson Jerome Powell’s press conference. While such questions will probably be batted away, Chairperson Powell is likely to be asked about the criminal probe launched by the Trump administration into the central bank and its campaign to pressure the Fed into lowering interest rates.

(Source: Bloomberg, Capital.com)

US Dollar slides as “sell America” trade reignites

The US Dollar is on the backfoot heading into the Fed decision due to the erratic trade and foreign policy of the Trump administration. Threats to invade Greenland – which have since been walked back – along with fresh tariffs threatened against the likes of Canada, South Korea and some European nations have reignited the so-called “sell America” trade.

At the margins, US rate expectations have been a modest tailwind to the US dollar recently, with exceptional growth and elevated inflation pushing back the timeline of future cuts and raising the futures curve. If the Fed mirrors that strength with slightly more hawkish language, that could add some support to the US Dollar, offsetting some of the weakness driven by a loss of confidence in the US government.

The US Dollar is reaching technically oversold levels in the short-term. The EUR/USD is approaching overbought levels on the daily RSI, with the pair falling short of the test of technical resistance at 1.1920. A dovish surprise from the Fed at this meeting could nudge the EUR/USD to test that level. Meanwhile, a reversion in the pair would bring previous resistance and now support at 1.180 into view.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)