ECB Preview: How many more cuts should we expect?

The ECB meeting in June will be key to determine the trajectory of monetary policy for the second half of 2025

The European Central Bank (ECB) will hold its next monetary policy meeting on Thursday, June 5, with markets widely anticipating another interest rate cut.

Interest Rate Outlook

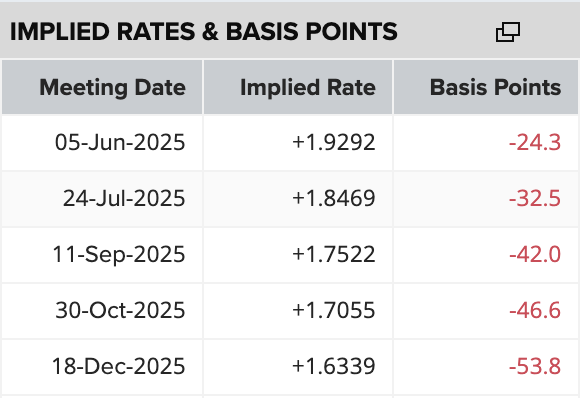

At its most recent meeting in April, the ECB reduced its key interest rates by 25 basis points, bringing the deposit facility rate to 2.25%. Markets are now pricing in another cut in June, though expectations for further easing beyond that remain uncertain. A potential pause in July is gaining traction, as the ECB evaluates incoming economic data and inflation dynamics. (Source: refinitiv)

(Source: refinitiv)

Economic Considerations

The ECB’s policy decisions hinge on maintaining a stable balance between inflation control and supporting economic growth.

Inflation in the Eurozone is projected to ease further throughout 2025. The preliminary May CPI reading, due two days before the meeting, is forecast by Reuters to show headline inflation falling to the ECB’s 2% target. A confirmation of this decline would likely reinforce the case for another rate cut.

However, given the central bank has already eased rates by 175 basis points over the past year, divergence within the Governing Council has emerged. Some members advocate for caution, signalling that the timing and pace of further rate cuts are still subject to debate.

On the growth front, the Eurozone faces headwinds from global trade tensions and subdued consumer demand. Rising mortgage payments are already prompting households to cut spending or dip into savings, posing a risk to overall consumption. However, recent GDP data indicates modest resilience, with quarterly growth picking up modestly over the past year.

The ECB has also stressed the importance of structural financial reforms and joint EU-level investments, particularly in defence and technology, to enhance long-term economic stability.

Market Implications

Investors will be closely parsing the ECB’s language for signals on the future path of interest rates.

- A dovish stance, including a June rate cut with a signal of continued easing, would likely boost European equities, especially ratesensitive sectors, as lower yields make stocks more attractive than bonds.

- In currency markets, a dovish ECB would likely weaken the euro, especially against the US dollar, given expectations that the Federal Reserve will hold rates steady for longer. This could extend recent downside pressure on EUR/USD.

Conversely:

- If the ECB cuts rates but expresses concern about lingering inflation risks, this could unsettle equity markets while offering some support to the euro.

- A hawkish stance, involving either no rate cut or messaging that downplays further easing, may pressure equities but could strengthen EUR/USD, particularly if the ECB expresses greater confidence in the Eurozone’s economic resilience.

Conclusion

The ECB’s June meeting will be a pivotal moment in determining the trajectory of monetary policy for the second half of 2025. With inflation nearing target and economic signals still mixed, the central bank must carefully navigate the trade-off between supporting growth and anchoring price stability.