BoC preview: too early for rate cuts?

BoC preview: too early for rate cuts?

The rise in CPI in December is making it hard for central banks to be mechanically dovish during their first meetings of the year. In Canada, consumer prices dropped 0.3% in the last month of 2023, but the year-round figure came in above the previous month at 3.4%, highlighting the non-linearity of the disinflation process.

It is widely expected that the Bank of Canada will leave rates unchanged at 5% at their meeting on Wednesday. Data provided by Reuters suggests markets are pricing in an 85% chance of no change to the current rate, with the remaining 5% assigned to a 25-bps cut. It still feels like it’s too soon for central banks in developed economies to start cutting rates given how the economic data has shown remarkable resilience after dealing with over 18 months of restrictive monetary policy.

That said, recent data in Canada has evidenced slowing consumer spending, and whilst the unemployment rate remains low, job growth does appear to be cooling. GDP contracted by 0.3% in the third quarter after failing to grow in Q2, and it’s expected that the economy continued to slow in the last quarter of 2023. The price of raw materials going into the manufacturing industry has dropped for three consecutive months, which could be seen as a prelude to slowing consumer prices in the coming months. If so, the path to lower interest rates could become clearer as the Bank of Canada juggles to keep growth and consumer activity from contracting too much, whilst making sure that inflation returns to its 2% target – but more importantly, it stays there for the foreseeable future.

Past performance is not a reliable indicator of future results.

Runaway inflation is one of the key concerns for central banks. Loosening financing conditions too soon can have a detrimental effect on the economy further down the line, so some level of certainty that price pressures are no longer a threat is expected to take the first step in cutting rates.

It is important to note that the cutting cycle doesn’t have to be continuous – central banks can take it one at a time and pause whenever they want, but market mentality is also a key factor to consider. Delivering the first-rate cut could open the floodgates and lead to further loosening of financing conditions via the bond market as traders reposition their expectations, making the balancing act harder for central banks.

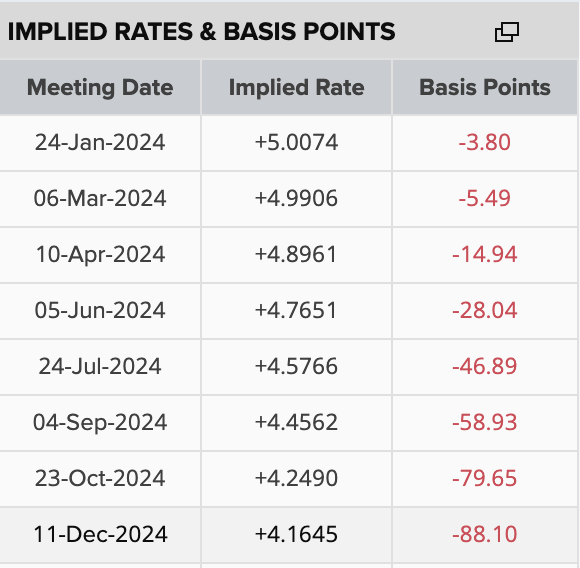

For now, markets are expecting 88bps of cuts in 2024. Interestingly, this is 50bps less than what is expected from the Federal Reserve or the European Central Bank.

Source: Refintiv

Source: Refintiv

The press conference after the meeting on Wednesday will likely be watched for any signs of when the cutting cycle may begin. Markets currently believe that the first real chance of a cut could come in April, but it may be pushed back to June. In a recent interview, BoC Governor Tiff Macklem mentioned that the end of tight policy was in sight but that consumers should get used to the fact that rates would not return to the pre-pandemic levels when ultra-low rates were the norm. Whether markets perceive a shift in positioning from the governor – whether it be more inclined to cut sooner or pushing back on immediate action following higher CPI in December – will be a key driver of momentum in markets.

USD/CAD has been acting less and less like a commodity currency as it derives its momentum as a USD proxy. The recent rally in the US dollar has allowed USD/CAD to recover over 2% since the start of the new year, reaching a five-week high at 1.3540 earlier last week. The pair has corrected lower since then and is now stuck below its 200-day SMA (1.3481) with the 50-day SMA converging just above. With the USD trading sideways over the past few days, Wednesday’s BoC meeting could be a good chance for CAD traders to gain the upper hand. If the central bank continues to push back on rate cuts alluding to stronger data, then CAD bulls could attempt to pull the pair back below 1.34. But a softer BoC may enable USD/CAD to resume its recent bullish rally.

USD/CAD daily chart

Past performance is not a reliable indicator of future results.

Past performance is not a reliable indicator of future results.