Bank of England preview: will updated projections show more cuts are expected in 2024?

Markets have no doubt that the BoE will keep its rate unchanged

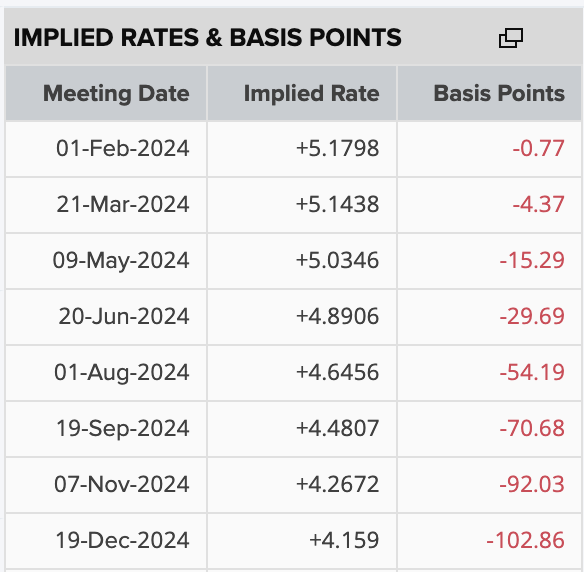

The Bank of England is expected to keep rates unchanged at its meeting on Thursday, 01 Februaryt. Data provided by Reuters shows a 97% chance of keeping rates at the current level of 5.25%. Until now, the central bank has had a firm stance against discussing any rate cuts, but anticipation is high heading into the first meeting of the year as pressure mounts to disclose further details about the future of monetary policy.

Despite the bank having consistently pushed back on rate cuts, markets are currently pricing 100bps of rate cuts in 2024, suggesting there will be four 25bps cuts between June and December. The recent rise in consumer prices in December pushed back on expectations for a rate cut sometime in the first half of the year, with the probability of a cut in March now down to 16%.

Source: Refinitiv

But despite the uptick in inflation, the annual rate has come down significantly from the peak of 11.1% seen at the end of 2022, suggesting that restrictive monetary policy has done its job in reducing spending and financing. But recent data has sparked concerns about growth and how much longer the UK economy can withstand a high level of rates. Whilst CPI is still a way from its 2% target – currently at 4% – business investment and consumer spending have both contracted significantly over the past few months. Mortgage approvals have also settled at a lower monthly average for the past year.

It is still unclear whether the Federal Reserve will deepen its dovish commentary at their meeting the day prior, but Lagarde’s comments last week seemed to suggest a turning point in the ECB’s policy book. She failed to explicitly mention rate cuts or give any forward guidance, but she also avoided any strong hawkish commentary, which has been a constant from her in the past few months. This has led markets to believe that, whilst she is not confident enough to communicate it, she no longer sees an immediate upside threat to inflation, and therefore rate cuts could follow soon. Her failure to leverage the higher CPI reading in December also reinforced this view.

The same could happen with Governor Bailey. He also failed to give much forward guidance in the BoE’s December meeting as he reiterated that the central bank remains data dependent. This is a key technique used to avoid having to give clear instructions on what’s to come. But, with pressure mounting on the economy, and markets expecting up to 100bps of cuts soon, he may feel enticed to give further insight, or at least seem open to the idea of cuts. Markets will be closely monitoring this, and UK assets will likely be sensitive to any developments in forward guidance.

The vote split will also be important. In December there were still three MPC members voting for a 25bps hike. At this meeting, it may be the first time since September 2021 that all nine members vote to keep rates unchanged. That said, we could have new dissidents that vote to cut rates by 25bps. The thing is, despite the expectations that this meeting will be more dovish than the previous one, it may not be as dovish as markets are hoping for. With no quarterly projections in December, markets were left with the meeting summary and minutes to guide their expectations. The vote split also helped price out dovish expectations.

That is why traders will be paying close attention to the updated projections at this meeting. In November, the Policy Report had headline inflation dropping to 3.1% and 1.9% by the end of 2024 and 2025 respectively. Any hint of an upgrade in any of these figures may derail rate-cut expectations. Similarly, the year-end Bank Rate projections for 2024 and 2025 in November 2023 stood at 5.1% and 4.5% respectively, suggesting that they only expected one 25bps cut this year. More cuts could be added in the new projections, but it seems unlikely that the bank will adapt to the four cuts expected by markets just yet.

Traders will also be eager to see if any MPC members still back a rate hike, as that could impact the timing of the first rate cut when it eventually comes. Moreover, to justify 100bps of cuts this year, the takeaways from this meeting have to be significantly more dovish than the one in December. If not, markets may be forced to re-price their expectations, leading to a shift in valuation for GBP and UK stocks.

GBP/USD daily chart

Past performance is not a reliable indicator of future results.

The pound rose over 1% against the US dollar following the December meeting after the BoE maintained its hawkish stance and failed to mention rate cuts. The pair was already pushing higher heading into the meeting as the Fed was surprisingly dovish the day prior, weighing on the dollar. Since then, GBP/USD has been trading mostly sideways and has failed to break above the resistance encountered between 1.2790 and 1.2830. The pair has been pulling back from its highs in recent days, and the RSI has been flattening along the midline with a downside tilt. This suggests the pair is struggling to attract new buyers, and therefore the path of least resistance remains lower in the short term. The Fed meeting on Wednesday will likely trigger the start of the move – depending on how markets perceive their monetary policies compare to each other.