PayPal stock forecast: Q4 miss, CEO change

PayPal Holdings is a US digital payments group; its shares came under pressure after Q4 2025 revenue missed estimates, 2026 profit guidance softened, and Enrique Lores became CEO on 1 March 2026. Past performance is not a reliable indicator of future results. Explore third-party PYPL price targets.

PayPal Holdings, Inc. (PYPL) is trading at $45.76 in early European trading at 10:27am UTC on 12 March 2026, having ranged between $44.75 and $45.88 intraday. Past performance is not a reliable indicator of future results.

PayPal reported Q4 2025 revenue of $8.68bn, missing analyst estimates of $8.80bn, while full-year 2026 adjusted profit guidance pointed to a low-single-digit percentage decline versus Wall Street expectations of approximately 8% growth, according to LSEG data (Reuters, 3 February 2026). A CEO transition is also in focus, with Enrique Lores, CEO of HP Inc., having taken the helm on 1 March following the exit of Alex Chriss (TechCrunch, 3 February 2026). Additionally, broader US equity markets are mixed on 12 March 2026, with the S&P 500 at 5,775.8 and the Nasdaq edging slightly higher, as investors weigh a tame February inflation print against rising oil prices tied to tensions around the Strait of Hormuz, keeping risk appetite cautious (Yahoo Finance, 11 March 2026).

PayPal stock forecast 2026–2030: Third-party price targets

As of 12 March 2026, third-party PayPal stock predictions reflect a broadly cautious consensus, shaped by the company's Q4 2025 earnings miss, a weaker-than-expected 2026 profit outlook, and a CEO transition announced in February 2026.

Canaccord Genuity, Mizuho (broker revisions)

Canaccord Genuity reiterates a hold rating on PYPL while sharply cutting its 12-month price target to $42 from $100. The reduction reflects the firm’s reassessment of PayPal’s competitive positioning and near-term earnings trajectory after Q4 2025 revenue of $8.68bn came in below the $8.82bn consensus estimate. Meanwhile, Mizuho set a $60 price target on PYPL as of 4 February 2026, maintaining a neutral stance amid post-earnings uncertainty. The firm flagged execution concerns and a challenging fiscal 2026 outlook as key factors weighing on the near-term valuation case (MarketBeat, 9 March 2026).

Fintel (price target projections)

Fintel’s forecast snapshot shows a wide projected range based on analyst estimates, with a projection date of 25 February 2027. The high estimate stands at $105.00, the low at $32.32, with a median projection of $48.45 and an average of $51.89. As with other third-party forecasts, these figures reflect published estimates at a point in time and can change as expectations and guidance evolve (Fintel, 12 March 2026).

MarketBeat (broker consensus overview)

MarketBeat aggregates ratings from 45 analysts and reports a consensus hold with an average 12-month PYPL stock forecast of $59.03, derived from 8 buy, 31 hold, and 6 sell ratings. The dispersion between the high estimate of $100 and the low of $32 highlights uncertainty around PayPal’s near-term outlook amid competitive pressures and leadership change (MarketBeat, 12 March 2026).

Predictions and third-party forecasts are inherently uncertain, as they cannot fully account for unexpected market developments. Past performance is not a reliable indicator of future results.

PYPL stock price: Technical overview

The PYPL stock price trades at $45.76 as of 10:27am UTC on 12 March 2026, within a $44.75-$45.88 intraday range. Price sits below its key simple moving-average cluster, with the 20/50/100/200-day SMAs running at approximately $44 / $50 / $57 / $64 respectively. The 50-day SMA near $49.89 represents the nearest overhead shelf, and the 200-day SMA at $63.94 remains a significant distance above current levels. The 20-over-50 alignment does not apply here, as price trades beneath all four tenors, keeping the intermediate trend under pressure.

Momentum is subdued: the 14-day relative strength index reads 46.42, sitting in neutral territory and offering no clear directional conviction. The average directional index at 23.34 sits just below the threshold that would signal an established trend, suggesting the current move lacks strong directional force.

To the upside, the classic R1 pivot at $53.61 is the first meaningful level to reclaim; a daily close above there would put the R2 area near $61.02 in view. The volume-weighted moving average at $44.43 and the simple moving average (20) at $44.29 offer a nearby confluence of support levels just below current price.

On the downside, the classic pivot point at $46.04 sits marginally above last price and acts as an immediate reference; a move beneath it would bring initial support at S1 near $38.63 into focus. Losing the $44.75 intraday low would reinforce downside momentum towards that S1 zone, with the S2 classic level at $31.06 as a deeper reference if selling pressure extends (TradingView, 12 March 2026).

This is technical analysis for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any instrument.

PayPal share price history (2024–2026)

PYPL’s stock price opened March 2024 trading near $63-64 and remained broadly rangebound through the spring and early summer, with prices oscillating between roughly $58 and $68 from April through to late June 2024.

The stock found firmer footing from late July 2024, climbing from a $57-58 base towards the $80-86 range by early November 2024, aided by improving broader market sentiment. A sharp earnings-driven surge on 29 October 2024 saw PYPL spike intraday to $86.05, its highest level of that period, before settling back into the mid-$80s through the remainder of the year. PYPL closed 2024 at $85.65.

The stock extended those gains into early 2025, touching a two-year high of $94.05 intraday on 21 January 2025, before Q4 2025 earnings on 3 February 2026 triggered a sharp sell-off. PYPL gapped down from $53.05 to close at $42.30 the following session, a single-day decline of roughly 20%. The stock has not recovered those levels since, drifting into the low-to-mid $40s through late February and into March 2026.

PYPL closed at $45.76 on 12 March 2026, down approximately 46.6% from its January 2025 peak of $94.05, and down approximately 32.6% year to date from the 31 December 2025 close of $58.61.

Past performance is not a reliable indicator of future results. Share prices are indicative and may differ from live market prices.

PayPal (PYPL): Capital.com analyst view

PayPal's price performance over the past year reflects a company navigating a meaningful transition. PYPL traded in the high $80s through much of early 2025, supported by solid total payment volume growth and an active share buyback programme. That picture shifted sharply in February 2026, when Q4 2025 earnings disappointed and full-year 2026 guidance pointed to flat-to-declining non-GAAP EPS, prompting a single-session decline of approximately 20%. The sell-off has left PYPL trading near multi-year lows, with the stock broadly range-bound in the $40-$48 area through March 2026.

On one hand, a $15bn share buyback programme and the arrival of a new CEO in Enrique Lores could act as stabilising factors if execution and strategy improve. On the other hand, branded checkout growth, PayPal's most closely watched profitability metric, slowed to just 1% in Q4 2025, while competition from Apple Pay, Klarna, Stripe, and AI-powered commerce tools continues to intensify, leaving the path to a re-rating dependent on execution rather than sentiment alone.

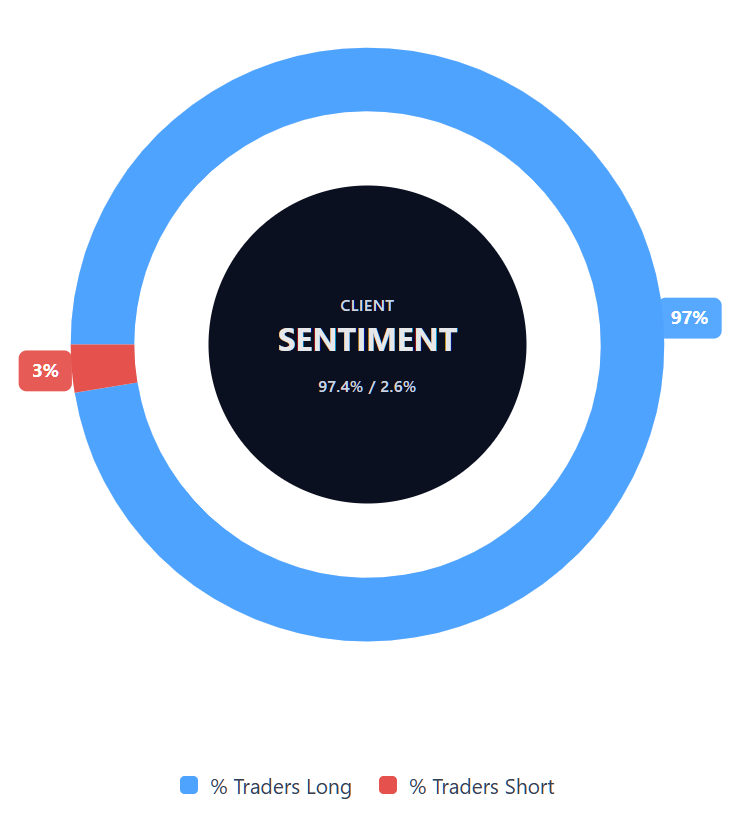

Capital.com’s client sentiment for PayPal CFDs

As of 12 March 2026, Capital.com client positioning in PayPal CFDs sits at 97.4% buyers vs 2.6% sellers, putting buyers ahead by 94.8 percentage points. This snapshot reflects open positions on Capital.com at the time of capture and can change rapidly as market conditions evolve.

Summary – PayPal 2026

- PYPL trades at $45.76 as of 10:27am UTC on 12 March 2026, down approximately 46.6% from its January 2025 peak of $94.05 and roughly 32.6% year to date.

- Price sits below all key simple moving averages (20/50/100/200-day), with the 14-day RSI at 46.42 in neutral territory and the ADX at 23.34 suggesting no firmly established trend.

- The classic pivot point at $46.04 acts as immediate resistance; the R1 level at $53.61 is the first meaningful upside reference, while S1 at $38.63 anchors the downside.

- Key drivers include a Q4 2025 earnings miss, full-year 2026 EPS guidance pointing to flat-to-declining profits, and a CEO transition as Enrique Lores took the helm in March 2026.

- Competitive pressure from Apple Pay, Klarna, Stripe, and AI-driven commerce tools continues to weigh on PayPal's branded checkout growth, which slowed to 1% in Q4 2025.

Past performance is not a reliable indicator of future results.

FAQ

Who owns the most PayPal stock?

What is the 5 year PayPal share price forecast?

Is PayPal a good stock to buy?

Could PayPal stock go up or down?

Should I invest in PayPal stock?

Can I trade PayPal (PYPL) CFDs on Capital.com?

Yes, you can trade PayPal CFDs on Capital.com. Trading share CFDs lets you speculate on price movements without owning the underlying asset and to take long or short positions. However, contracts for difference (CFDs) are traded on margin, and leverage amplifies both profits and losses. You should ensure you understand how CFD trading works, assess your risk tolerance, and recognise that losses can occur quickly.