NVIDIA stock forecast: TSMC demand signal, China risk

NVIDIA is a US chipmaker whose recent share-price moves have reflected strong AI-related demand, record quarterly revenue, and continued uncertainty around US export controls affecting China sales. Explore third-party NVDA targets. Past performance is not a reliable indicator of future results.NVIDIA Corporation (NVDA) last traded at $188.34 as of 4:57pm UTC on 13 April 2026, pulling back from an intraday high of $189.42 and holding well above the session low of $182.50. Past performance is not a reliable indicator of future results.

Sentiment around the stock has been underpinned by robust AI-driven demand, with TSMC reporting first-quarter revenue up 35.1% year on year – a result that lifted chipmakers broadly and saw the Philadelphia Semiconductor Index reach a record high of 8,926.08 on 10 April 2026 (Reuters, 10 April 2026). NVIDIA rose 1.8% in that session as investors interpreted strong foundry revenue as a proxy for sustained GPU demand (FinancialContent, 10 April 2026). The broader backdrop also includes ongoing trade policy uncertainty, with the Trump administration's export control framework continuing to restrict NVIDIA's ability to ship certain advanced chips to China without a licence – a regulatory overhang NVIDIA flagged in its fiscal Q4 2026 results, noting that it was not assuming any Data Center compute revenue from China in its forward outlook (NVIDIA Investor Relations, 25 February 2026). NVIDIA's fiscal Q4 2026 earnings, reported in February 2026, showed record revenue of $68.1 billion, up 73% year on year, with Q1 fiscal 2027 revenue guidance set at approximately $78.0 billion, providing a fundamental reference point for the stock's current trading level (Fortune, 25 February 2026).

NVIDIA stock forecast 2026–2030: Third-party price targets

As of 13 April 2026, third-party NVIDIA stock predictions reflect a broadly constructive stance, shaped by NVIDIA's record fiscal Q4 2026 results, GTC 2026 disclosures around the Blackwell and Rubin platform roadmap, and the company's updated $1 trillion GPU revenue outlook through 2027 (NVIDIA Investor Relations, 25 February 2026). The following targets summarise leading third-party views on the NVDA market.

New Street Research (Buy, trimmed target)

New Street Research lowered its 12-month price target on NVDA to $275 from $307, while retaining a Buy rating. Analyst Pierre Ferragu maintained his constructive stance despite the revised estimate, noting that NVIDIA added approximately $500 billion in orders since October 2025 and that management's $1 trillion revenue projection through 2027 likely understates the eventual outcome (MarketBeat, 1 April 2026).

Raymond James (Strong Buy, raised target)

Raymond James raised its 12-month NVDA stock forecast to $323 from $291, keeping a Strong Buy rating, as analyst Simon Leopold increased estimates to reflect management's updated $1 trillion cumulative GPU sales outlook through 2027. The firm noted that its inference-as-a-catalyst thesis may be running slightly ahead of schedule, with next-generation Vera Rubin and Rubin Ultra platforms expected to sustain revenue momentum into the second half of 2026 (Yahoo Finance, 28 March 2026).

Wedbush (Outperform, reaffirmed with upside call)

Wedbush analyst Dan Ives reaffirmed an Outperform rating on NVDA, citing 30–40% upside from then-prevailing levels near $177 and describing the pullback as a buying opportunity amid near-term macro noise. The firm pointed to accelerating enterprise AI deal activity, Jensen Huang's statement that the agentic AI inflection has arrived, and NVIDIA's Q4 fiscal 2026 networking revenue growth of 263% year on year as indicators that underlying demand remains structurally intact (247 Wall St., 6 April 2026).

Intellectia AI (consensus overview, multi-analyst compilation)

A compilation of sell-side ratings reports that 38 analysts covering NVDA assign a consensus Buy rating with an average 12-month price target of $253, implying approximately 38% upside from the then-current price of $183. Evercore ISI analyst Mark Lipacis holds the street-high target of $352, underpinned by a view that NVIDIA could capture 70–80% of the AI accelerator market, with rising inventory levels cited as a signal of sustained demand growth (Intellectia AI, 12 April 2026).

MarketBeat (consensus survey, broad panel)

MarketBeat's aggregated consensus across 53 analysts assigned NVDA a Buy rating, with an average 12-month price target of $275.25, a high of $400, and a low of $140. The wide range reflects divergent assumptions on AI spending durability, export control headwinds affecting China revenue, and competitive dynamics in the GPU market (MarketBeat, 10 April 2026).

Predictions and third-party forecasts are inherently uncertain, as they cannot fully account for unexpected market developments. Past performance is not a reliable indicator of future results.

NVDA stock price: Technical overview

On the daily chart, the NVDA stock price trades at $188.34 as of 4:57pm UTC on 13 April 2026, holding above a broadly aligned moving-average cluster, with the 20-, 50-, 100- and 200-day SMAs sitting at roughly $178, $182, $183 and $181 respectively, according to TradingView. All 12 SMA and EMA readings across the 10-through-200 tenor range carry a buy signal, reflecting consistently constructive positioning of price relative to its key averages. The 200-day EMA at $174.29 runs notably below the 200-day SMA, providing a secondary longer-term reference level. The Hull moving average (9) at $189.04 sits fractionally above the last close and registers a sell signal, suggesting near-term momentum may be moderating at these levels.

Momentum readings from TradingView are mixed. The 14-day RSI at 61.38 sits in the upper-neutral band, consistent with a constructive but not overextended condition. The commodity channel index (20) at 146.65 registers a sell signal, while the ultimate oscillator at 71.90 and the MACD level at 0.84 both show buy signals; the average directional index (14) at 18.38 remains below 25, suggesting the current trend lacks strong directional conviction.

On the topside, the classic R1 pivot at $187.43 sits just below the last close of $188.34; the R2 level at $200.46 comes into view should price sustain a daily close above R1. On the downside, the classic pivot point at $175.85 represents the first reference, with the 100- and 200-day SMA shelf in the $181–$183 area a secondary consideration; a move beneath that cluster could open the path towards the S1 pivot at $162.82 (TradingView, 13 April 2026).

This is technical analysis for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any instrument.

NVIDIA share price history (2024–2026)

NVDA’s stock price opened April 2024 trading near $85, still early in what would become a sustained AI-driven rally. The stock climbed steadily through the rest of 2024, closing the year at $134.34 on 31 December 2024, a gain of roughly 56.7% from mid-April levels, as demand for NVIDIA's Blackwell GPU architecture gathered momentum across hyperscale data centre customers.

2025 brought sharper swings. NVDA started the year at $137.97 on 2 January and pushed to a dataset high close of $207.28 on 3 November 2025, buoyed by record fiscal-quarter results and accelerating AI infrastructure spending. That peak proved difficult to hold. A combination of broader tech sector pressure and US–China chip export uncertainty pulled the stock lower through late 2025 and into the new year, with the sharpest leg coming in early April 2025, when NVDA touched a session low of $86.13 on 7 April 2025 amid tariff-driven market stress – a peak-to-trough decline of roughly 52.1% from the November 2025 close. The stock recovered sharply from there, nearly doubling from that low.

NVDA closed at $188.10 on 13 April 2026, approximately 0.3% down year to date from the 2 January 2026 open of $188.74, but up around 71.9% year on year versus the 14 April 2025 close of $109.42.

Past performance is not a reliable indicator of future results. Share prices are indicative and may differ from live market prices.

NVIDIA (NVDA): Capital.com analyst view

NVDA's price trajectory over the past two years reflects the scale of market appetite for AI infrastructure exposure, with the stock roughly doubling from mid-2024 levels before enduring a sharp correction of over 50% between November 2025 and early April 2025. The subsequent recovery, which brought NVDA back above $188, suggests that demand-side fundamentals – centred on data centre GPU spend and NVIDIA's Blackwell and Rubin platform roadmap – continue to attract buyers after pullbacks. That said, the speed and depth of the April 2025 drawdown illustrate how quickly sentiment can shift; any softening in AI capital expenditure commitments from hyperscale customers, or further tightening of US chip export controls towards China, could weigh on the stock in a similarly abrupt fashion.

On the macro side, a weaker US dollar environment has historically supported dollar-denominated growth equities, and the current trade policy uncertainty cuts both ways: escalating tariffs add cost pressure to NVIDIA's supply chain, while any de-escalation could act as a near-term catalyst. Consensus analyst targets published in March and April 2026 sit between $253 and $323, reflecting broad conviction on AI demand durability, though the wide range of estimates – from $140 to $400 across the full analyst panel – underscores how materially views diverge on longer-term competitive dynamics and regulatory risk.

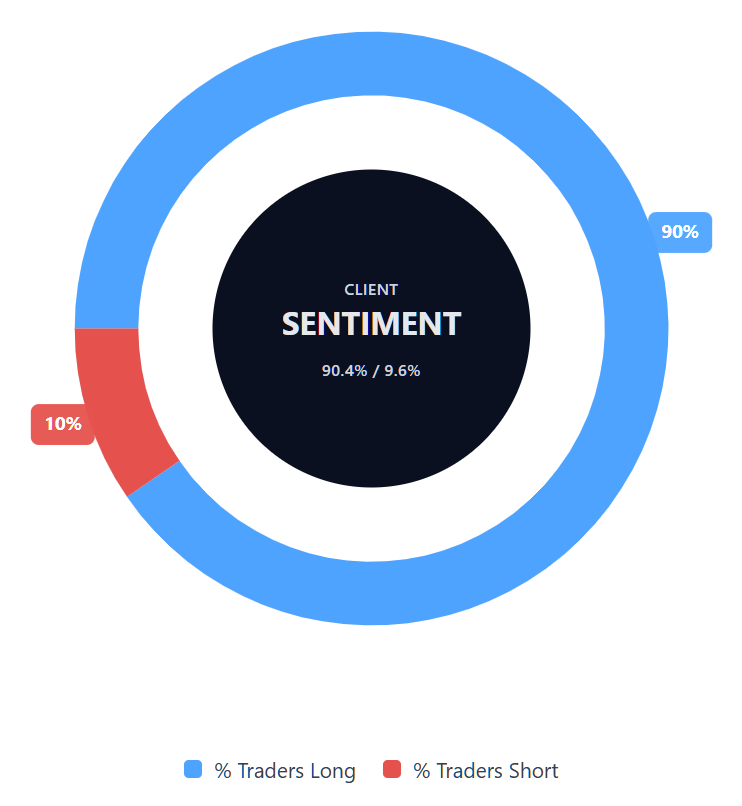

Capital.com’s client sentiment for NVIDIA CFDs

As of 13 April 2026, Capital.com client positioning in NVIDIA CFDs stands at 90.4% long and 9.6% short, putting buyers ahead by 80.8 percentage points and placing sentiment firmly in heavy-buy, one-sided-towards-longs territory. This snapshot reflects open positions on Capital.com and can change rapidly as market conditions evolve.

Summary – NVIDIA 2026

- As of 4:57pm UTC on 13 April 2026, NVDA was trading at $188.34, roughly 0.3% down year to date but up around 71.9% year on year.

- Key price drivers include AI data centre GPU demand, NVIDIA's Blackwell and Rubin platform roadmap, and the company's fiscal Q4 2026 revenue of $68.1bn, up 73% year on year.

- US chip export controls affecting China sales remain an ongoing regulatory overhang, while broader tariff uncertainty adds macro risk to near-term earnings visibility.

- TSMC's 35.1% year-on-year Q1 revenue growth, reported in April 2026, lifted semiconductor sentiment and provided a positive read-across for NVDA.

Past performance is not a reliable indicator of future results.

FAQ

Who owns the most NVIDIA stock?

What is the 5-year NVIDIA share price forecast?

Is NVIDIA a good stock to buy?

Could NVIDIA stock go up or down?

Should I invest in NVIDIA stock?

Can I trade NVIDIA CFDs on Capital.com?

Yes, you can trade NVIDIA CFDs on Capital.com. Trading share CFDs lets you speculate on price movements without owning the underlying asset and to take long or short positions. However, contracts for difference (CFDs) are traded on margin, and leverage amplifies both profits and losses. You should ensure you understand how CFD trading works, assess your risk tolerance, and recognise that losses can occur quickly.