NVIDIA stock forecast: Record Q4 revenue, H200 exports

NVIDIA reported record Q4 fiscal 2026 revenue of $68.1bn, while Blackwell demand, conditional H200 exports to China and wider tech-sector weakness continue to shape the stock’s outlook. Past performance is not a reliable indicator of future results. Explore third-party NVDA price targets.

NVIDIA Corporation (NVDA) is trading near $175.70 in the afternoon session at 12:05pm UTC on 7 April 2026, within an intraday range of $175.50–$178.90. Past performance is not a reliable indicator of future results.

Pressure on the stock reflects a confluence of macro and sector-specific factors. Broad US equity markets have faced volatility amid ongoing trade policy uncertainty, with recession concerns elevated after Goldman Sachs raised its 12-month US recession probability to 30% from 25% in late March 2026, while J.P. Morgan and other major banks issued similar warnings in prior months (TheStreet, 24 March 2026). The Nasdaq has faced selling pressure alongside the wider Magnificent Seven cohort amid that same macro backdrop.

At the company level, NVIDIA reported record Q4 fiscal 2026 revenue of $68.1bn, up 73% year-on-year, with Data Center revenue reaching $62.3bn, driven by Blackwell platform adoption and AI infrastructure demand. The company also guided Q1 fiscal 2027 revenue of approximately $78bn, above Wall Street's consensus expectation of $72.6bn at the time (NVIDIA Investor Relations, 25 February 2026). Additionally, the US approved conditional exports of NVIDIA's H200 chips to China in January 2026, with requirements including third-party chip assessment and supply adequacy conditions, keeping regulatory dynamics in focus for the stock (Reuters, 14 January 2026).

NVIDIA stock forecast 2026–2030: Third-party price targets

As of 7 April 2026, third-party NVIDIA stock predictions reflect broadly bullish sentiment on the company's AI infrastructure positioning, with individual 12-month targets ranging from $250 to $325. The forecasts below are drawn from sell-side research notes and a consensus aggregator, ordered from lower to higher target.

Benchmark (Buy reiteration)

Benchmark reiterates a Buy rating with a $250 12-month NVDA stock forecast, maintaining confidence in the stock's near-term trajectory. The firm cites NVIDIA's Q4 fiscal 2026 earnings beat – EPS of $1.62 against a consensus of $1.54 – and continued hyperscaler demand for Blackwell architecture as the basis for the retained target (MarketBeat, 1 April 2026).

New Street Research (target trim)

New Street Research lowers its 12-month price target on NVDA to $275 from $307, while retaining a Buy rating, implying approximately 56% upside from the prior close at the time of publication. The reduction reflects valuation recalibration amid broad sector derating and ongoing trade policy uncertainty, rather than a change in the firm's underlying view on AI infrastructure demand (MarketBeat, 1 April 2026).

Raymond James (Strong Buy, target raise)

Raymond James raises its 12-month price target on NVDA to $323 from $291, maintaining a Strong Buy rating, as analyst Srini Pajjuri points to management's visibility into $1tn in GPU-related sales through 2027, which the firm notes may represent a conservative estimate. The increase is anchored in NVIDIA's Q4 fiscal 2026 revenue of $68.13bn, up 73.2% year on year, with the firm citing sustained hyperscaler capital expenditure commitments and the Blackwell platform ramp as the primary demand drivers (Investing.com, 18 March 2026).

MarketBeat (sell-side consensus overview)

MarketBeat aggregates ratings across 53 covering analysts, placing the average 12-month consensus price target for NVDA at $275.25, with a consensus rating of Buy. The distribution comprises 4 Strong Buy, 47 Buy, and 2 Hold ratings, with no Sell recommendations recorded. The target range runs from $140 at the low end to $320 at the high, with analysts broadly weighing robust near-term Blackwell demand against longer-run risks, including US export restrictions, custom-chip competition from hyperscalers, and macro-driven valuation pressure (MarketBeat, 1 April 2026).

Public.com (consensus aggregator)

Public.com reports an average 12-month consensus price target of $267.55 for NVDA across 38 covering analysts, with a Buy consensus rating. According to the breakdown, 55% of analysts assign a Strong Buy, 39% a Buy, 3% a Hold, and 3% a Strong Sell. The aggregator notes that the bull case centres on data centre revenue growing at a compound annual rate of approximately 80–90% through calendar 2026 and 2027, while the bear case flags risks including market-share erosion, heightened GPU competition, and macroeconomic pressure on capital expenditure budgets (Public.com, 6 April 2026).

Predictions and third-party forecasts are inherently uncertain, as they cannot fully account for unexpected market developments. Past performance is not a reliable indicator of future results.

NVDA stock price: Technical overview

The NVDA stock price trades at $175.70 as of 12:05pm UTC on 7 April 2026, sitting just above the classic pivot point of $175.85 and broadly in line with the short-term moving average cluster. The 10- and 20-day simple moving averages (SMAs) at around $174 and around $178 respectively register buy signals on TradingView, while the 30-, 50-, and 100-day SMAs at around $180, around $183, and around $183 all read sell, reflecting a stock trading in a contested zone between short- and medium-term trend signals.

The 14-day relative strength index (RSI) sits at 49.37, a neutral reading that points to neither overbought nor oversold conditions. The average directional index (ADX) at 21.99 indicates a developing rather than established trend, suggesting price action lacks strong directional conviction at current levels.

On the topside, R1 at $187.43 (classic pivot) is the nearest reference above the current price; a daily close through this level could put R2 near $200.46 into view. The Hull moving average (9) at $177.47 and the volume-weighted moving average at $177.33 sit marginally above the last price and may act as near-term references.

On the downside, the classic pivot at $175.85 provides initial support, with S1 at $162.82 the next classic reference below. The 200-day SMA at around $180 and 100-day SMA at around $183 both sit above the current price, while the 200-day exponential moving average (EMA) at around $173.77 represents the nearest long-term moving average shelf beneath current levels (TradingView, 7 April 2026).

This is technical analysis for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any instrument.

NVIDIA share price history (2024–2026)

NVDA’s stock price opened April 2024 around $87, already in the early stages of what would become a marked two-year run driven by surging demand for AI chips and data centre infrastructure.

The stock closed 2024 at $134.34 – a gain of roughly 178% for the year – after touching a two-year high around $140 in November 2024, before pulling back into year-end. NVDA started 2025 near $138 and continued to trend higher through January, briefly touching $150 on 7 January 2025 before retreating. The stock stabilised in the $120–$140 range through February and early March 2025, then came under significant pressure from April through early May 2025, falling as low as $86.13 on 7 April 2025 as tariff-related macro concerns weighed on the broader technology sector.

A recovery gathered pace from May 2025 onwards. NVDA climbed back through the $130s and $140s into summer, and by late October 2025 had retraced towards a peak close of $207.28 on 3 November 2025, the highest close in the provided dataset. The stock then gradually drifted lower, closing 2025 at $186.63.

NVDA is trading at $175.70 on 7 April 2026, approximately 5.9% below its 31 December 2025 close of $186.63, and around 77% above its 7 April 2025 close of $99.25.

Past performance is not a reliable indicator of future results. Share prices are indicative and may differ from live market prices.

NVIDIA (NVDA): Capital.com analyst view

NVDA's price trajectory over the past two years reflects the extraordinary growth of AI infrastructure spending, with the stock climbing from the mid-$80s in April 2024 to a peak close of $207.28 in November 2025 on the back of record quarterly revenues and sustained hyperscaler capital expenditure commitments. The Blackwell platform rollout and NVIDIA's dominant position in data centre GPU supply have underpinned that strength, though the same concentration in a single growth theme leaves the stock exposed to any shift in AI spending priorities, tighter export controls, or the emergence of competing custom silicon from major cloud providers.

As of 7 April 2026, NVDA trades approximately 15% below that November 2025 peak, with broader macro headwinds – including trade policy uncertainty and sector-wide valuation pressure – acting as a drag on the price. At the same time, the company's Q4 fiscal 2026 earnings beat and forward revenue guidance of approximately $78bn for Q1 fiscal 2027 suggest that the underlying demand environment remains intact. Some market participants view this as a potential support factor, while others point to the stock's premium valuation as a risk if growth expectations moderate.

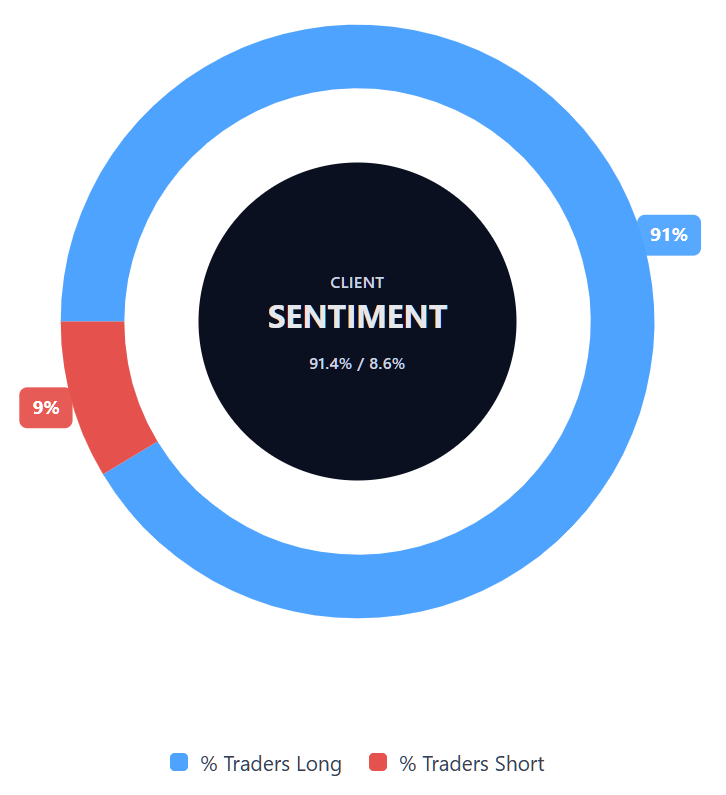

Capital.com’s client sentiment for NVIDIA CFDs

As of 7 April 2026, Capital.com client positioning in NVIDIA CFDs stands at 91.4% buyers and 8.6% sellers, which puts buyers ahead by 82.8 percentage points and places sentiment firmly in a heavy-buy, one-sided-long territory. This snapshot reflects open positions on Capital.com at the time of publication and can change rapidly as market conditions evolve.

Summary – NVIDIA 2026

- NVDA trades at $175.70 as of 12:05pm UTC on 7 April 2026, around 15% below its November 2025 peak close of $207.28 and approximately 77% above its April 2025 low near $86.

- Key price drivers include AI data centre demand via the Blackwell platform, hyperscaler capital expenditure commitments, US export control policy on chip sales to China, and broader macro and trade policy uncertainty.

- NVIDIA reported record Q4 fiscal 2026 revenue of $68.13bn, up 73% year on year, and guided Q1 fiscal 2027 revenue of approximately $78bn, with the US conditionally approving H200 chip exports to China in January 2026.

- TradingView's technical indicators are mixed: short-term moving averages signal buy, while the 30-, 50-, and 100-day SMAs sit above the price and read sell; RSI at 49.37 is neutral, with no strong directional trend confirmed.

Past performance is not a reliable indicator of future results.

FAQ

Who owns the most NVIDIA stock?

What is the 5 year NVIDIA share price forecast?

Is NVIDIA a good stock to buy?

Could NVIDIA stock go up or down?

Should I invest in NVIDIA stock?

Can I trade NVIDIA CFDs on Capital.com?

Yes, you can trade NVIDIA CFDs on Capital.com. Trading share CFDs lets you speculate on price movements without owning the underlying asset and to take long or short positions. However, contracts for difference (CFDs) are traded on margin, and leverage amplifies both profits and losses. You should ensure you understand how CFD trading works, assess your risk tolerance, and recognise that losses can occur quickly.