Amazon stock forecast: Q1 2026 earnings

Amazon reported Q1 2026 revenue of $181.5bn, up 17% year on year, with AWS revenue rising 28% to $37.6bn and net income at $30.30bn. Explore third-party AMZN price targets and technical analysis. Past performance is not a reliable indicator of future results.

Amazon.com, Inc. (AMZN) is trading at $262.68 as of 10:04am UTC on 18 May 2026, within an intraday range of $261.11–$267.20 per the Capital.com quote feed. Past performance is not a reliable indicator of future results.

Sentiment around AMZN remains supported by a strong Q1 2026 earnings report, in which Amazon posted revenue of $181.5bn, up 17% year-on-year, and net income of $30.3bn (Amazon IR, 29 April 2026). AWS cloud revenue rose 28% year-on-year to $37.6bn, the fastest growth rate in 15 quarters, while results exceeded analyst consensus on both revenue and earnings (CNBC, 29 April 2026). More broadly, the macro backdrop remains uncertain, with elevated energy costs and a firmer US dollar weighing on sentiment following the Trump-Xi summit held in Beijing on 14–15 May 2026 (CNBC, 15 May 2026). The summit produced agreements including a bilateral Board of Trade framework and tariff reductions on select goods, though market participants remain cautious about the depth and pace of any broader US-China trade de-escalation (World Economic Forum, 8 May 2026).

Amazon share forecast: AWS growth shapes third-party outlook

As of 18 May 2026, third-party Amazon stock predictions reflect generally constructive sell-side sentiment following Amazon's Q1 2026 results. Individual broker 12-month targets range from $250 to $370, while consensus aggregates converge in the $305–$312 range. AWS acceleration, AI infrastructure deployment and advertising growth are the most consistently cited positive factors across active coverage.

POEMS (accumulate rating)

Phillip Securities Research, published under the POEMS platform, sets a 12-month AMZN price target of $280, assigned alongside an accumulate rating. The firm notes that Q1 2026 revenue was in line with expectations, while adjusted net income slightly missed expectations due to higher tax expense. It cites AWS growth of 28% year-on-year as the primary structural driver, while Amazon left its $200bn full-year capital expenditure guidance unchanged (POEMS, 4 May 2026).

New Street Research (buy, sharply raised target)

New Street Research lifted its AMZN 12-month price target to $350 from $280, maintaining a buy rating. The firm attributes the substantial upward revision to Amazon's Q1 2026 earnings beat and the $194bn–$199bn Q2 2026 revenue guidance range, with AWS acceleration and advertising growth of 24% year-on-year flagged as the principal drivers (MarketBeat, 4 May 2026).

TD Cowen (strong buy, reiterated)

TD Cowen Managing Director John Blackledge reiterated a strong buy rating on AMZN and a $350 12-month price target. The analyst highlighted AI-driven cloud workload expansion and Amazon's sustained capital expenditure programme as the key underpinnings of the view, while noting that AMZN had advanced approximately 18% year-to-date through mid-May 2026 (Watcher Guru, 13 May 2026).

Public.com (consensus tracker)

Public.com aggregates analyst forecasts for AMZN, recording an average 12-month price target of $305.76 across active coverage. The tracker reflects a broad buy consensus, with the figure derived from multiple independent broker ratings updated after Q1 2026 earnings (Public.com, 14 May 2026).

MarketBeat (consensus overview)

MarketBeat aggregates 60 active analyst ratings on AMZN as of 16 May 2026, producing a consensus 12-month price target of $312.52, within a range of $218–$370. The breakdown shows 57 buy ratings and three hold ratings, with no sell recommendations on record. Across the active coverage universe, AWS momentum and AI monetisation prospects appear to underpin the broadly positive stance (MarketBeat, 16 May 2026).

Predictions and third-party forecasts are inherently uncertain, as they cannot fully account for unexpected market developments. Past performance is not a reliable indicator of future results.

AMZN earnings: Q1 2026 results and Q2 2026 outlook

Amazon reported Q1 2026 results on 29 April 2026, posting revenue of $181.5bn, up 17% year-on-year, alongside net income of $30.3bn (Amazon IR, 29 April 2026). AWS remained the headline driver, with cloud revenue growing 28% year-on-year to $37.6bn, ahead of analyst consensus of $36.64bn per StreetAccount, marking the fastest growth rate in 15 quarters (CNBC, 29 April 2026). The advertising segment expanded 24% year-on-year to $17.2bn, reinforcing its position as a fast-growing profit contributor. For Q2 2026, Amazon guided net sales in the range of $194bn–$199bn, ahead of the prior consensus estimate of $188.7bn, implying continued double-digit year-on-year growth (MarketBeat, 16 May 2026). The company maintained its full-year capital expenditure guidance of approximately $200bn, directed mainly towards AI infrastructure and data centre capacity, a figure that analysts monitoring free cash flow generation relative to investment commitments have focused on (Variety, 29 April 2026).

Operating income for Q1 2026 came in at $23.9bn, with AWS contributing the largest share of group profitability at $14.16bn in segment operating income (Digital Commerce 360, 30 April 2026). Amazon did not provide formal earnings per share guidance for Q2 2026, though Q1 2026 EPS of $2.78 beat analyst consensus of $1.63 by $1.15. The next scheduled earnings release, covering Q2 2026, is estimated for 30 July 2026, in line with Amazon's standard

AMZN stock price: Technical overview

The AMZN stock price trades at $262.68 as of 10:04am UTC on 18 May 2026, above its longer-term moving-average shelf but below the near-term 10- and 20-day simple moving averages. The daily 20/50/100/200-day SMAs stand at approximately $265 / $237 / $231 / $229, with the 20-over-50 alignment intact across the SMA family. This keeps the medium-term trend structure constructive, while the Hull moving average (9) at $265.63 and the volume weighted moving average (20) at $264.56 sit just above the current price, consistent with the mild near-term softness suggested by the momentum (10) reading of -4.12.

The 14-day relative strength index registers 58.56, an upper-neutral reading that neither signals overbought conditions nor suggests a clear loss of upside momentum. The average directional index (14) at 38.38 indicates that an established trend is in place.

On the classic pivot framework, R1 at $291 represents the first notable reference overhead. A daily close above that level would put R2 at $316.93 in view. To the downside, the classic pivot (P) at $247.95 provides initial support, with the 100-day SMA near $231 marking the next meaningful moving-average shelf. A sustained move below those levels could bring S1 near $222.01 into focus (TradingView, 18 May 2026).

This technical analysis is for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any instrument.

Amazon share price history (2024–2026)

AMZN’s stock price opened May 2024 around $183–$185, then drifted lower through late summer, briefly touching $151.70 intraday on 5 August 2024 as a global equity sell-off, triggered by an unwinding of yen-carry trades and recession concerns, swept through US markets. The stock recovered through autumn, reclaiming the $190–$200 range by late October ahead of Q3 2024 earnings, and closed 2024 at $219.85.

The momentum carried into early 2025, with AMZN touching highs above $241 in late January before slipping back towards the $210–$220 range through February and March. A tariff-driven sell-off dominated April 2025, dragging the stock to an intraday low of $160.50 on 7 April amid escalating US-China trade tensions. A partial recovery followed, with the stock closing April 2025 near $191.

AMZN spent most of summer and autumn 2025 consolidating in the $210–$245 range before pulling back in February 2026, dropping to around $198 as broader tech sentiment softened. A second tariff shock hit in early April 2026, pushing AMZN to a 2026 low of $204.83 on 2 April, before a strong Q1 2026 earnings beat — $181.50bn in revenue, up 17% year on year — drove a sharp rebound.

AMZN closed at $262.70 on 18 May 2026, approximately 19.5% above its 2026 opening price of $219.85.

Past performance is not a reliable indicator of future results. Share prices are indicative and may differ from live market prices.

Amazon (AMZN): Capital.com analyst view

Amazon's price performance over the past 12 months reflects the stock's sensitivity to both company-specific catalysts and broader macro conditions. The drawdown to the low $160s in April 2025, and again towards $204 in early April 2026, shows how trade policy developments and tariff escalation can weigh on a company with deep global supply chain exposure. Those periods also showed how quickly the stock can recover when sentiment shifts, with the post-earnings rebound in late April 2026 among the most pronounced moves in the two-year window.

AWS's 28% year-on-year revenue growth in Q1 2026 reinforces the structural cloud and AI narrative. However, the $200bn full-year capital expenditure commitment means the investment cycle remains front-loaded, and free cash flow may face near-term pressure if AI monetisation ramps more slowly than expected.

Advertising revenue growth of 24% year on year adds a diversified earnings stream that is less capital-intensive than cloud infrastructure, which some analysts view as a margin-supportive factor over the medium term. However, Amazon still operates across highly competitive verticals, from e-commerce and logistics to cloud and media, where execution risk and regulatory scrutiny remain persistent considerations. Macro factors, including Federal Reserve rate policy and US-China trade dynamics, have historically amplified AMZN's volatility in both directions and remain relevant to the near-term price environment.

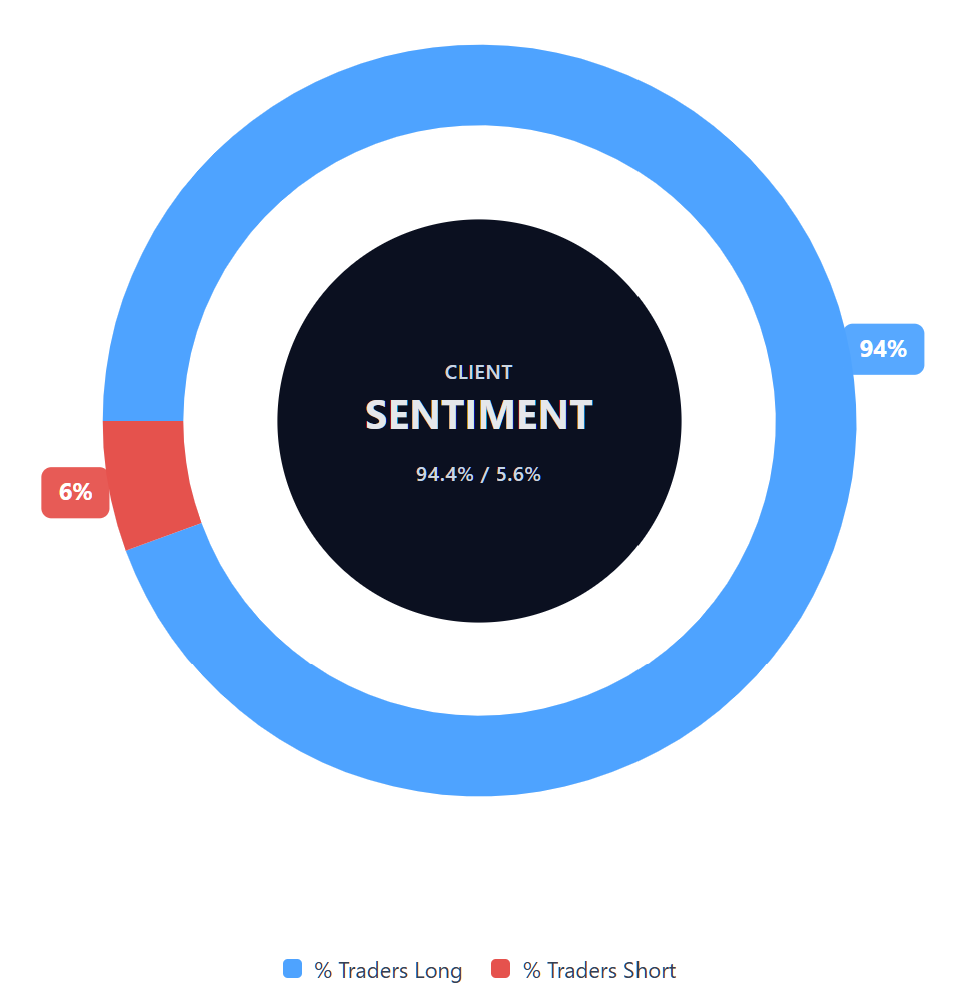

Capital.com’s client sentiment for Amazon CFDs

As of 18 May 2026, Capital.com client positioning in Amazon CFDs stands at 94.4% long vs 5.6% short, putting buyers ahead by 88.8 percentage points. This indicates a heavily long-leaning client sentiment snapshot. The data reflects open positions on Capital.com at the time of capture and can change rapidly as market conditions evolve.

Summary – Amazon 2026

- Amazon (AMZN) trades at $262.68 as of 10:04am UTC on 18 May 2026, up approximately 19.5% from its 2026 opening price of $219.85 and well above the April 2025 tariff-driven intraday low of $160.50.

- Q1 2026 earnings were a primary catalyst, with revenue up 17% year on year to $181.50bn and AWS revenue growing 28% to $37.60bn. The results helped drive a sharp post-results rebound from early April lows near $204.

- Key upside drivers cited by analysts include AWS cloud acceleration, AI infrastructure investment and advertising growth of 24% year on year. Key risks include elevated capital expenditure of approximately $200bn, free cash flow timing and ongoing US-China trade policy uncertainty.

Past performance is not a reliable indicator of future results.

FAQ

Who owns the most Amazon stock?

What is the five-year Amazon share price forecast?

Is Amazon a good stock to buy?

Could Amazon stock go up or down?

Should I invest in Amazon stock?

Can I trade Amazon CFDs on Capital.com?

Yes, you can trade Amazon CFDs on Capital.com. Trading share CFDs lets you speculate on price movements without owning the underlying asset and to take long or short positions. However, contracts for difference (CFDs) are traded on margin, and leverage amplifies both profits and losses. You should ensure you understand how CFD trading works, assess your risk tolerance, and recognise that losses can occur quickly.