Mortgage rate forecast for 2025 and beyond

Explore the latest mortgage rate forecasts, with third-party predictions and how to trade CFDs linked to rate movements.

Mortgage interest rates represent the percentages charged by lenders on home loans. In the US, these rates are influenced by movements in long-term treasury yields, which in turn reflect expectations for the federal funds rate set by the Federal Reserve – a key benchmark that drives short-term borrowing costs and shapes overall economic activity.

For contract for difference (CFD) traders, mortgage rate movements can provide some insights into broader macroeconomic trends. Expectations of changes in Federal Reserve policy may influence USD forex pairs, as well as shares or indices with exposure to housing, banking, and consumer credit.

In this guide, we examine the latest US mortgage interest rate forecasts from third-party analysts, alongside key factors shaping the outlook.

US mortgage rates: 2025 forecast

As of May 2025, third-party forecasts suggest US mortgage rates may ease gradually through the rest of the year – though the pace of decline remains uneven across outlooks.

Fannie Mae, in its May 2025 Economic and Housing Outlook, projected average 30-year fixed mortgage rates at 6.5% in Q2 2025, falling to 6.1% by Q4. That would bring the full-year average to 6.4%, before edging lower to 5.9% in 2026.

The Mortgage Bankers Association (MBA) took a more cautious view in its May 2025 forecast. The group expected rates to remain at 6.7% through Q3 2025, slipping to 6.6% by year-end. Its full-year projection came in at 6.6% – among the highest in the current set of forecasts.

Wells Fargo forecasted a more moderate decline. Its economists expected rates to fall from 6.6% in Q2 to 6.3% by the end of 2025. Despite earlier cuts to the federal funds rate, the bank noted in its March update that: 'Mortgage rates are not far from levels which prevailed over a year ago,' suggesting limited transmission from policy to borrowing costs so far.

Freddie Mac echoed that view, pointing to a shift in market sentiment: 'Unlike last year when many were anticipating that mortgage rates would decline, in early 2025 the prevailing sentiment is that rates will stay higher for longer.' The firm noted that this may lead to earlier homebuyer activity, as fewer buyers now expect further near-term drops.

Mortgage rate forecast for 2026

Looking further ahead, most forecasters expect a continued – though still modest – decline in mortgage rates. Fannie Mae projected the average 30-year fixed rate to fall to 5.8% by Q4 2026. Wells Fargo and the MBA placed their 2026 averages at 6.35% and 6.3%, respectively.

Morningstar provided the most optimistic view, forecasting a drop to 5.60% in 2026 and 5.00% by 2027, assuming inflation pressures continue to ease. Fitch Ratings, in its Global Housing and Mortgage Outlook, saw rates ranging from 5.7% to 6.3% in 2026 and noted: 'We expect arrears to continue to fall as further cuts to mortgage rates reduce mortgage payments.'

Past performance is not a reliable indicator of future results.

What’s the US mortgage interest rate history?

Between 2005 and 2008, average mortgage rates in the US ranged between 5.87% and 6.41%, reflecting a period of relatively tight monetary policy prior to the global financial crisis. As the downturn unfolded, rates were pushed lower in response to aggressive Fed easing. By 2012, the average rate had dropped to 3.66%, and remained below 4% for much of the following decade.

The COVID-19 pandemic saw mortgage rates hit fresh record lows, with the 30-year fixed average falling to a 2.65% all-time-low in 2021. However, that trend reversed from 2022 onwards, as the Federal Reserve implemented a series of rate hikes to combat inflation. Average mortgage rates rose in 2022 and again in 2023, marking the fastest tightening cycle since the 1980s.

By May 2025, the 30-year fixed mortgage rate had reached 6.81%, remaining below 7% for 17 consecutive weeks. 'Stable mortgage rates coupled with moderately rising inventory are attracting homebuyers into the market,' said Sam Khater, Chief Economist at Freddie Mac, noting that purchase application activity was up 18% year-on-year.

What’s the average mortgage rate?

US mortgage interest rates averaged 6.81% in May 2025, according to Trading Economics data, reflecting a slight increase from 6.76% the previous week. The move tracked a rise in long-term treasury yields, as investor sentiment improved following a temporary tariff rollback between the US and China.

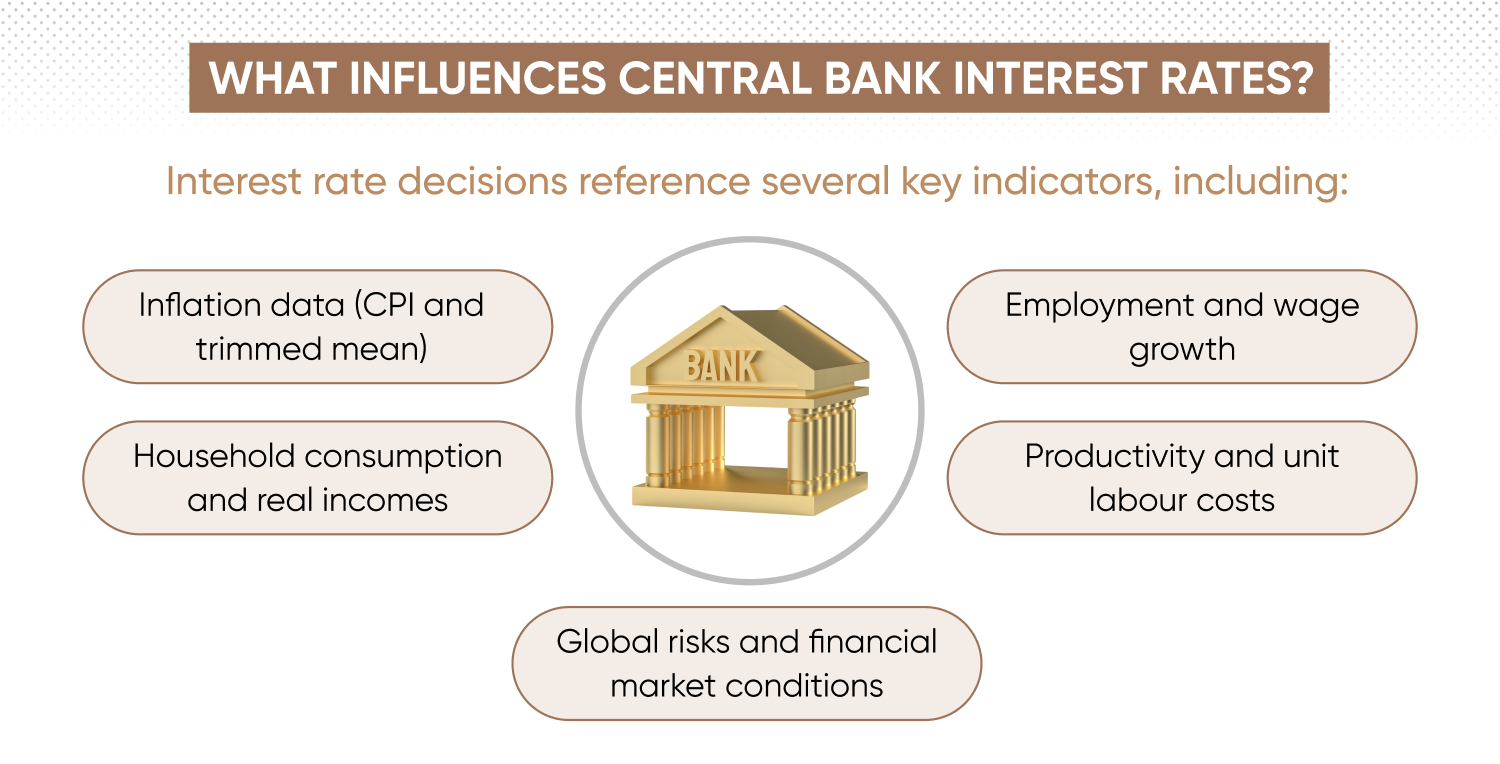

Understanding US Federal Reserve rate decisions

The US Federal Reserve sets the federal funds rate to meet its dual mandate: stable inflation and maximum employment. This benchmark rate directly influences borrowing costs across the economy – including mortgage interest rates – and indirectly shapes expectations across forex and equity markets.

In its 7 May 2025 statement, the Federal Open Market Committee (FOMC) voted to hold the federal funds rate at 4.25%-4.50%, maintaining a cautious stance amid mixed economic signals. While activity continued to expand and labour market conditions remained solid, inflation stayed above the Fed’s 2% target.

Notably, the Fed flagged a rise in uncertainty compared with its March meeting. The statement pointed to ‘increased risks of both rising unemployment and inflation’, suggesting that policymakers may need to respond flexibly to incoming data. ‘The Committee will carefully assess incoming data, the evolving outlook, and the balance of risks,’ it said.

According to J.P. Morgan’s Vinny Amaru, ‘the Fed’s recent statement emphasized that the economy continues to expand at a moderate rate despite some recent trade data anomalies, mostly due to the likely frontloading of imports ahead of potential tariffs.’

The Fed has continued with its balance sheet reduction, reducing holdings of treasuries and mortgage backed securities. This process may add a further tightening layer to financial conditions, potentially affecting longer-dated yields and, in turn, mortgage rates.

What’s next for mortgage rates?

The FOMC’s next policy meeting is scheduled for 17-18 June 2025, which is when new economic projections will be released.

For traders, shifts in rate expectations can affect USD forex pairs and shares – particularly those linked to banking, housing and consumer credit. The outlook for mortgage rates will hinge closely on how the Fed balances risks across growth, inflation, and financial stability over the coming months.

Interest rates: How do they affect mortgages?

The Federal Reserve funds rate influences US mortgage prices. When the central bank changes its official rate, lenders adjust their variable mortgage rates accordingly – though the relationship isn’t always one-to-one, and the flow-through can vary in both timing and magnitude.

Global interest-rate settings also play a role. If major central banks like the European Central Bank shift policy, it can influence bond yields and funding markets.

Here’s how two cash rate scenarios might impact variable mortgage rates:

| Scenario | Reaction | Result |

|---|---|---|

| Fed hikes the cash rate | Lenders may increase variable mortgage rates. | Higher repayments may reduce borrowing capacity, potentially weighing on housing prices. |

| Fed cuts the cash rate | Lenders may reduce variable mortgage rates.* | Lower repayments may stimulate demand, potentially supporting housing prices. |

*However, lenders may delay or partially pass on cuts, especially if their funding costs remain elevated.

For fixed mortgage rates, the link to Fed moves is less direct. Fixed rates reflect expectations about future interest rate changes and domestic bond market conditions, making them sensitive to shifts in central bank guidance and investor sentiment.

Discover third-party US Federal Reserve interest rate predictions.

What other factors influence US mortgage rates?

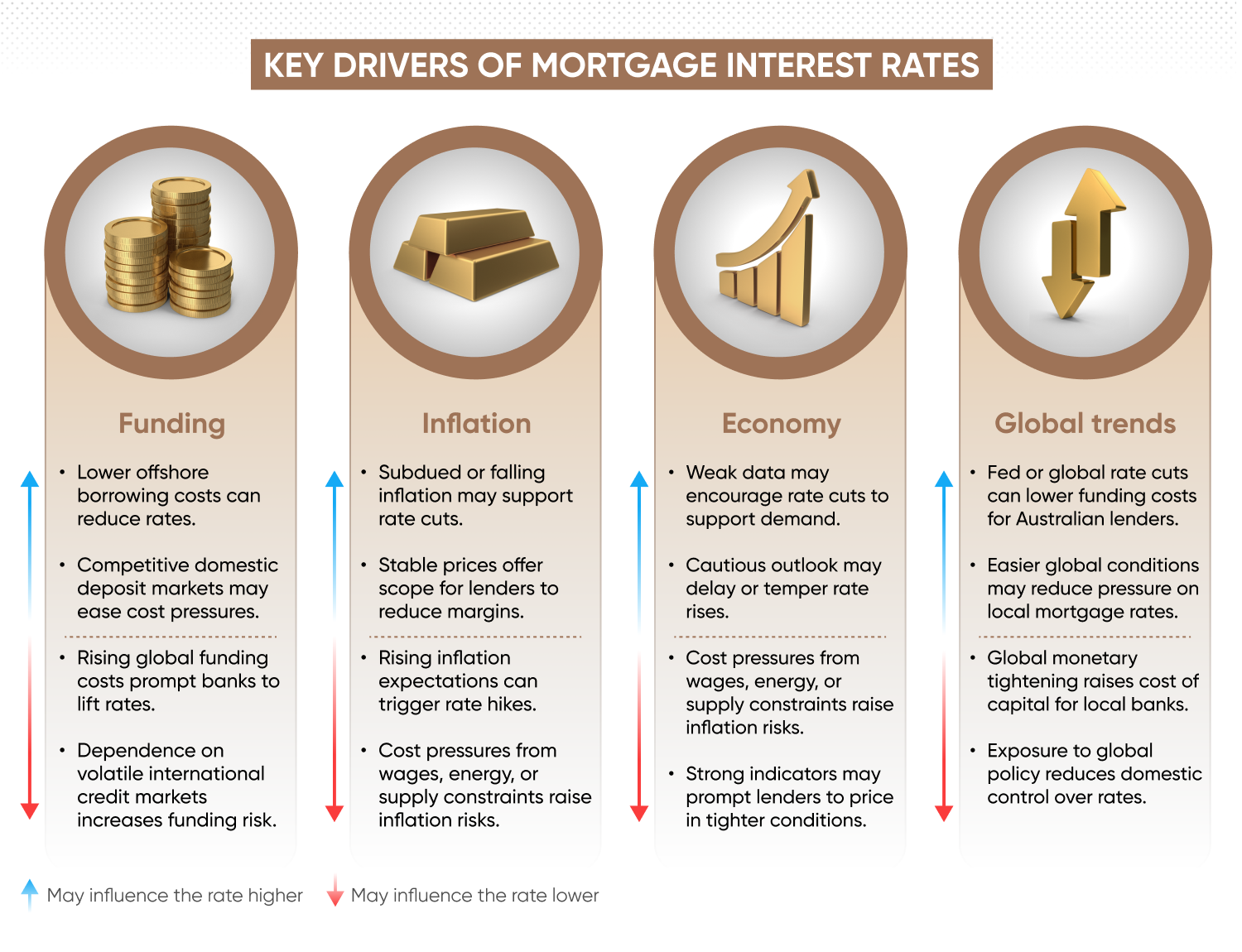

Although the federal funds rate remains an important influence for US mortgage pricing, other factors also affect how lenders set interest rates on home loans – including bond market trends, borrower risk profiles and broader macroeconomic developments. For fixed-rate mortgages, the primary benchmark is the yield on the 10-year treasury bond.

Bond yields

Most US mortgage rates are loosely pegged to the yield on 10-year treasury bonds. If yields rise – often in response to inflation expectations or changes in Fed guidance – mortgage rates typically follow. Conversely, falling yields can create scope for lenders to reduce mortgage rates, especially if demand for safe-haven assets increases.

Credit risk and borrower profile

Lenders assess individual borrower risk when setting rates. A higher credit score, lower debt-to-income (DTI) ratio, or larger down payment can lead to better terms. Many lenders apply rate tiers, with the best pricing reserved for FICO scores above 740. Loan type and repayment term also play a role – for example, shorter-term or adjustable-rate loans may come with lower initial rates.

Inflation trends

Persistent inflation or rising inflation expectations can drive up long-term borrowing costs. Mortgage lenders may adjust rates pre-emptively if data suggests upward price pressure – whether due to energy costs, wage growth or supply disruptions. If inflation subsides and real yields fall, lenders may reduce mortgage rates where feasible.

Funding costs and market liquidity

Banks and non-bank lenders raise capital through deposits, securitisation, or wholesale and repo markets. If funding costs rise – due to credit spreads widening, higher risk premiums, or tighter global liquidity – lenders may lift mortgage rates to maintain margins. Lower funding costs, in contrast, can offer room to cut.

Global central bank policy

US mortgage markets are indirectly influenced by overseas monetary policy. Fed decisions tend to have the strongest impact, but tightening by the European Central Bank or Bank of Japan can raise global bond yields and affect capital flows. These global shifts can influence treasury yields and indirectly affect mortgage pricing, even without changes to US domestic policy.

How to trade mortgage interest rates

While mortgage interest rates aren’t directly tradeable, their movements can influence various CFD markets – especially shares and forex. Here’s how to gain exposure to mortgage rate trends through related assets.

Shares

Mortgage rate fluctuations can affect a range of interest rate-sensitive sectors – most notably banks, mortgage REITs, and homebuilders. These businesses can see margins, earnings, and valuations shift in response to changes in borrowing costs and housing demand.

Rising mortgage rates can mean higher borrowing costs, slower housing demand, and weaker affordability. This may put pressure on homebuilders and mortgage REITs, while supporting bank margins if lending volumes hold up.

Falling mortgage rates can mean cheaper credit, increased home loan activity, and a pickup in refinancing. This may benefit homebuilders and rate-sensitive equities, but can narrow margins for banks and mortgage lenders.

Here are some shares CFDs that react to mortgage rate trends:

- JPMorgan Chase & Co – major US bank with large retail lending operations and some exposure to housing credit – trade JPMorgan

- Bank of America Corp – one of the largest US mortgage lenders; net interest income fluctuates with rate cycles – trade Bank of America

- Annaly Capital Management – mREIT focused on mortgage assets; performance hinges on yield spreads – trade Annaly

- AGNC Investment Corp – specialises in agency-backed mortgage investments; sensitive to long-term rate shifts – trade AGNC

- DR Horton – leading US homebuilder; sales volumes correlate with housing affordability – trade DR Horton

- Taylor Wimpey PLC – UK-listed builder; demand and affordability are influenced by interest rate levels – trade Taylor Wimpey

- Barclays PLC – UK-based bank with residential mortgage exposure; impacted primarily by Bank of England policy – trade Barclays

- Old Republic International – US mortgage insurer; performance linked to housing defaults and credit conditions – trade Old Republic

Forex

Mortgage interest rates are shaped by long-term bond yields, which in turn reflect monetary policy and macroeconomic outlook. These same dynamics affect forex markets – particularly where rate differentials between countries drive capital flows.

Rising mortgage rates may reflect expectations that the US Federal Reserve will tighten policy, leading to higher long-term treasury yields and a stronger US dollar (USD).

Falling mortgage rates could signal a shift toward Fed easing, pushing yields lower and weakening the USD.

Here are some forex CFDs you can trade now, aligned with mortgage rate moves:

- USD/JPY – historically follows US treasury yields; rising US mortgage rates may strengthen USD – trade USD/JPY

- EUR/USD – sensitive to Fed-ECB rate outlook; dovish ECB stance or hawkish Fed guidance can weigh on the euro – trade EUR/USD

- GBP/USD – moves on rate differentials between the Bank of England and Federal Reserve – trade GBP/USD

- AUD/USD – reacts to diverging RBA and Fed policy signals; yield expectations can drive direction – trade AUD/USD

- USD/CAD – Canada’s housing market plays a key role; mortgage-sensitive data may influence CAD – trade USD/CAD

- NZD/USD – commodity-linked pair influenced by global interest rate trends and risk sentiment – trade NZD/USD

Learn more about forex trading

FAQs

What are mortgage rates today?

As of 22 May 2025, the average 30-year fixed mortgage rate in the US stood at 6.81%, according to Freddie Mac. This marked the 17th consecutive week the rate remained below 7%, with recent movements reflecting shifts in treasury yields and market sentiment. Weekly changes tend to follow developments in long-term bond markets, rather than short-term policy shifts.

When will mortgage rates go down?

Most third-party forecasts expect a gradual easing in mortgage rates through the second half of 2025 – though timing remains uncertain. Fannie Mae projected a decline to 6.1% by Q4, while the Mortgage Bankers Association and Wells Fargo expect more modest reductions. Future cuts will depend on Federal Reserve decisions, inflation trends, and broader funding conditions. If the Fed resumes easing or treasury yields decline, mortgage rates could move lower – though lenders may delay passing on cuts, depending on margins and risk sentiment.

What is the current mortgage interest rate?

The current national average for a 30-year fixed mortgage rate is 6.81% as of mid-May 2025. Shorter-term and adjustable-rate loans may offer lower rates, but pricing varies based on borrower profile, loan structure, and lender funding costs. Mortgage rates remain elevated by historical standards, though they have stabilised in recent months as inflation pressures eased and Federal Reserve policy turned more data-dependent.