Five things traders learned this US earnings season

S&P 500 earnings beat expectations, valuations improved, and the Magnificent Seven led the way.

The US earnings season for the third quarter is all but over. Here are five things traders learned this reporting period.

The S&P 500 is delivering double digit earnings growth

The S&P 500 exceeded expectations again in the Q3. The market is on course to deliver 13.4% earnings growth for the the period*, vastly exceeding the 7.9% estimate heading into it. The result was underpinned by a better than expected 8.4% expansion in revenues and an increase in profit margins to a 16 year high of 13.1%.

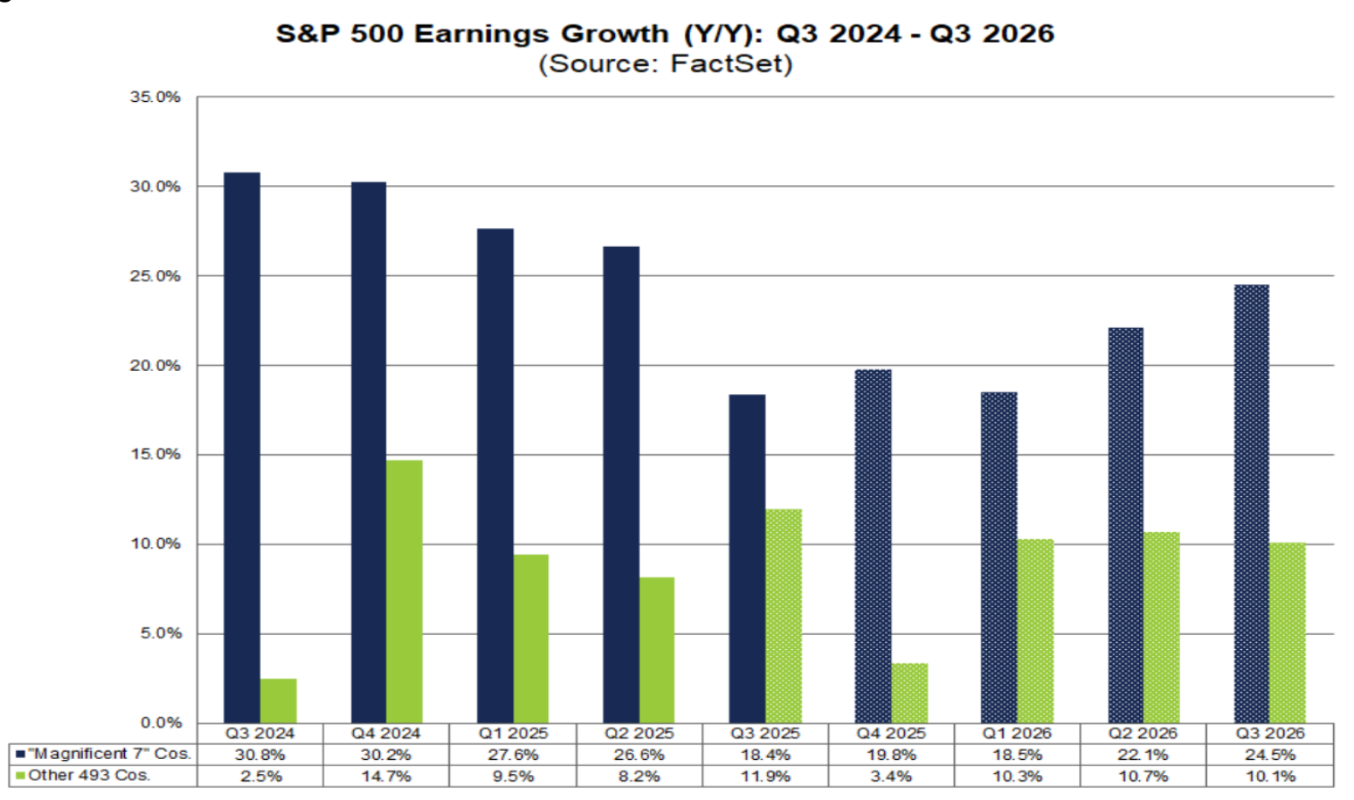

Magnificent Seven earnings are still beating expectations - but by less than before

The Magnificent Seven stocks remain the main drivers of the S&P 500’s earnings growth. However, its outperformance is slowing down. The group delivered 18.4% growth versus the 11.9% growth for the “S&P 493”*. This exceeded the roughly 14% growth projected by analysts heading into the reporting period. But that was down from the nearly 27% and 28% growth delivered in Q1 and Q2.

(Source: FactSet)

Earnings growth is broadening out

Earnings growth was deeper and broader for the S&P 500 in Q3. 83% of companies posted upside surprises for the quarter*. Meanwhile, the number of sectors reporting earnings growth widened to nine. Every sector also posted topline expansion, suggesting a cyclical upswing for S&P 500 companies.

Analysts expected strong earnings growth in the year ahead

Solid guidance has led analysts to upgrade expectations for future earnings growth across the S&P 500. EPS growth projections for Q4 have been revised higher to 7.5%, with double digit earnings expected for FY26. This includes forecasts of 12.2% and 13.3% EPS growth in Q1 and Q2 respectively*.

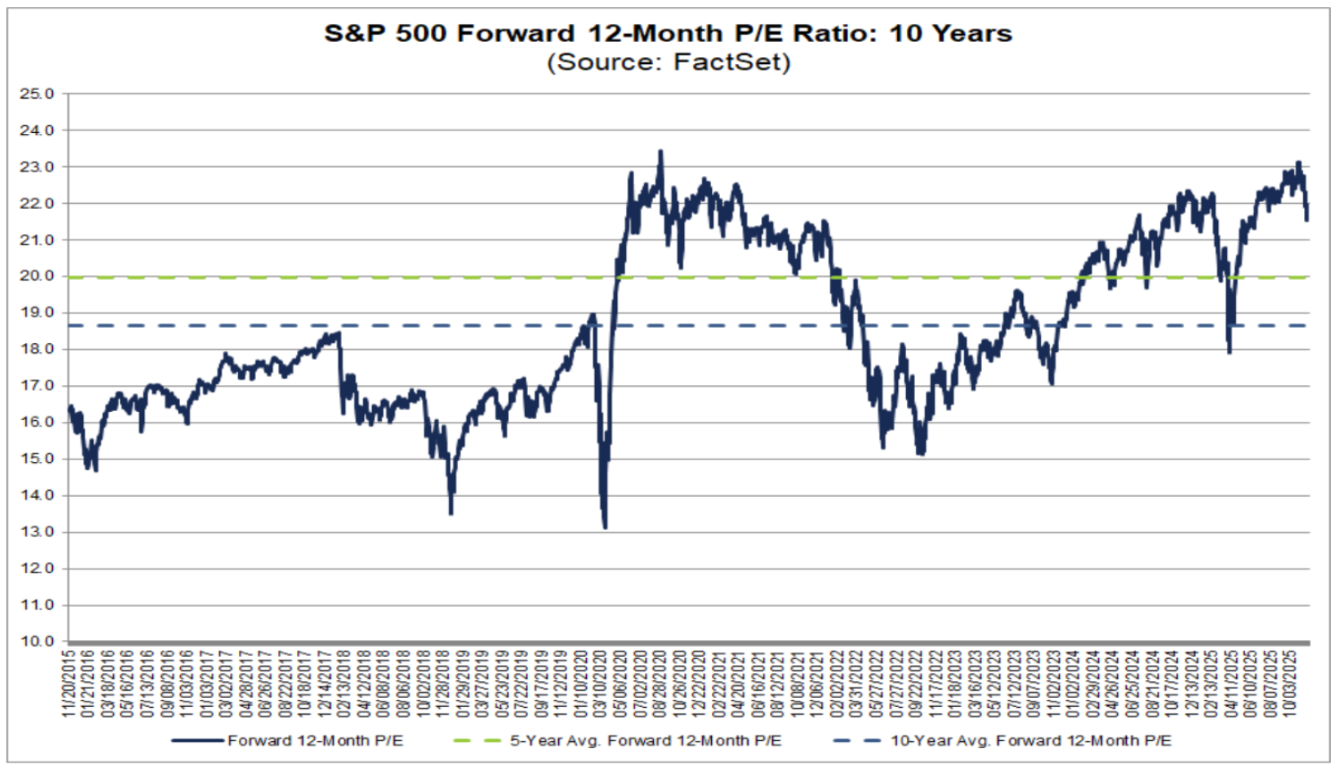

Valuations are rich but not as rich as before

The S&P 500 remains richly valued, historically speaking. However, valuations moderated throughout the earnings period, courtesy of the upward revisions to the earnings outlook and the drop in stock prices seen throughout November. The S&P 500’s Forward 12-Month P/E Ratio fell from above 23 and levels reminiscent of the COVID bubble and Dot.com boom, to a still high but less extreme 21.5*.

(Source: FactSet)

* Data according to FactSet as of 21st of November, 2025