Fed, BOJ, and ECB Take Centre Stage

The next couple of days will be a defining moment for US equity markets and markets globally, with the Fed, the BOJ, and the ECB all making monetary policy announcements and decisions.

The next couple of days will be a defining moment for US equity markets and markets globally, with the Fed, the BOJ, and the ECB all making monetary policy announcements and decisions, alongside mega-cap earnings from companies such as Microsoft, Meta, and Alphabet on Wednesday, 29 October, and Amazon and Apple on Thursday, 30 October. These events are likely to be a significant development cumulatively and could shape market performance for the rest of the year, across multiple asset classes. Positive earnings released may accelerate the stock market's bull run, while disappointing results could leave markets floundering and potentially lead to a sharp decline into year-end.

Still, central bank policy will matter for broader market volatility measures, and, more importantly, for FX markets. This means one cannot overlook the potential impacts of these upcoming announcements, along with the press conferences that follow.

Fed Policy Announcement

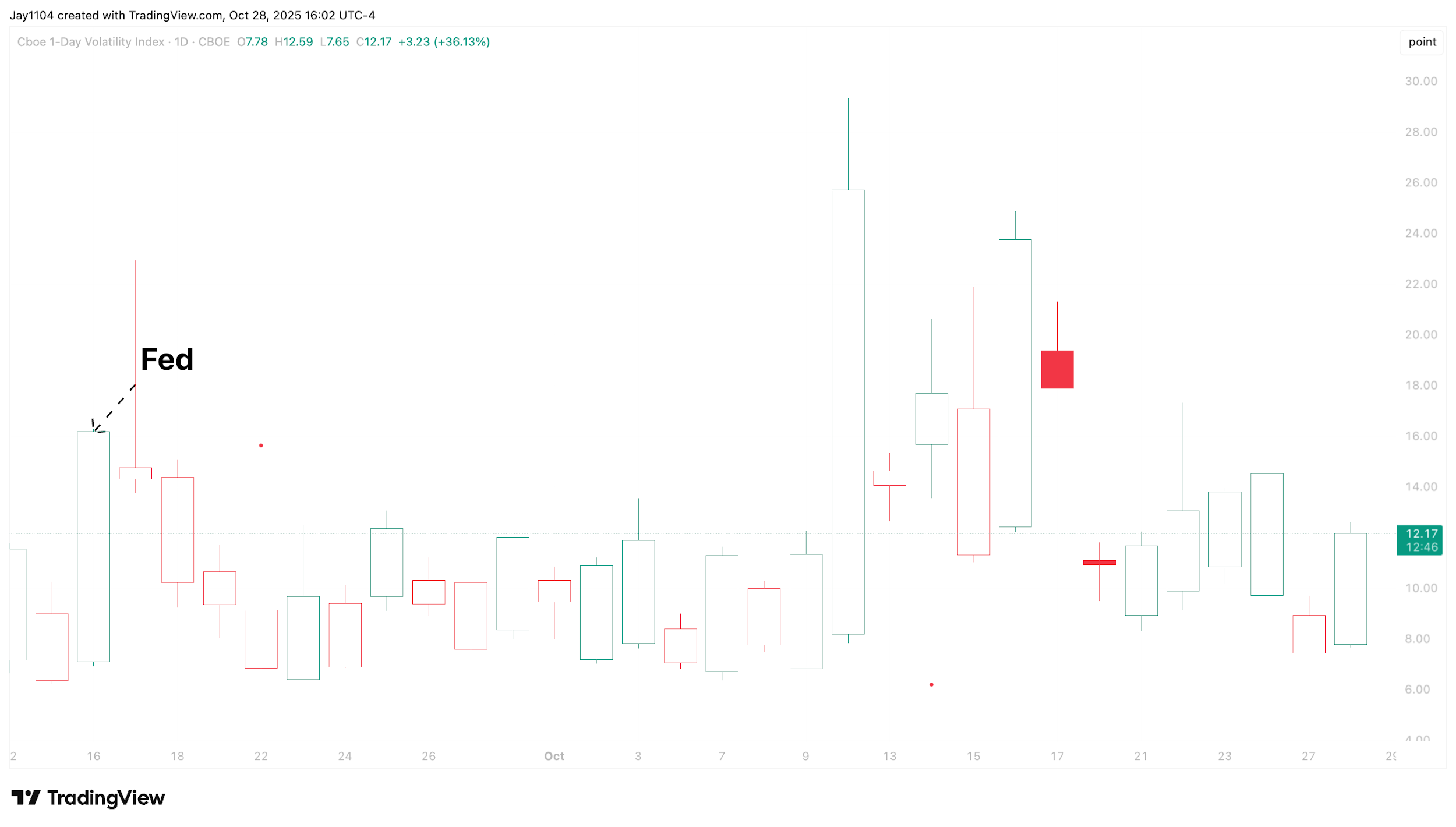

Implied volatility is likely to move sharply higher on Wednesday, 29 October, ahead of the 2PM ET Fed announcement, as measured by the VIX 1-day. Typically, we see the VIX 1-day rise ahead of a Fed event and then fall sharply following the press conference, or during it. Therefore, if implied volatility is elevated and then declines sharply after the Fed announcement and press conference, stocks could rally regardless of the meeting's outcome. At times, when implied volatility does not reset during the press conference, it can tend to do so overnight in the futures market, which can set the stage for a rally on Thursday. However, given the upcoming major earnings releases, and overnight reset this time could also change depending on those results.

(Source: TradingView)

(Past performance is not a reliable indicator of future results)

Bank Of Japan

The Bank of Japan's rate decision will come on Thursday, 30 October. At present, expectations are for the bank not to raise rates at this meeting. However, there is growing pressure on the Bank of Japan to raise rates at some point, and investors will be listening very closely for any subtleties or changes in the language the BOJ may offer at this month's meeting, which could signal a potential rate hike as soon as December.

This would, of course, mean the yen could strengthen materially against the US dollar. The yen has weakened back towards 153 and appears to be forming a potential double-top pattern. If the yen were to fall below 151, it could drop further towards 149.5 or possibly fill an open gap down at 147 near the lower end of the trend line in the coming days, should the BOJ strike a hawkish tone and indicate that a rate hike may be coming sooner than markets had previously expected.

(Source: TradingView)

(Past performance is not a reliable indicator of future results)

ECB

The ECB meeting will also take place on Thursday, 30 October, and market participants will be listening closely to see whether the ECB has any further rate cuts in store in the future. If it turns out that the ECB is indeed finished cutting rates, one might expect the euro to strengthen significantly against the dollar.

At present, the euro is sitting at resistance around 1.165, and we are beginning to see signs of momentum shifting once again. The euro has been stuck in a trading range for some time, making it difficult to establish a clear direction. However, a move above 1.165 could see the euro rise towards 1.175 and possibly as high as 1.19. Should the ECB strike a more hawkish tone about its policy outlook—particularly if that outlook signals no further rate cuts—this scenario may support a stronger euro..

(Source: TradingView)

(Past performance is not a reliable indicator of future results)