ADP Report Could Set Tone for Dollar and Treasury Markets This Week

The ADP jobs report on Wednesday, 5 November, at 8:15 a.m. Eastern Time is expected to show that hiring in October improved, rising by 25,000 jobs — a significant improvement from the September reading, which showed a decline of 32,000 jobs.

Given the absence of official government data, the market will place extra emphasis on this report to gain a clearer understanding of the trend and direction of employment. It is worth noting that ADP now publishes a weekly jobs report that provides the average weekly change in employment.

According to this data, for the four weeks ending 11 October, private employers added an average of 14,250 jobs per week — better than the average of 10,750 recorded on 4 October, but weaker than the 33,500 seen on 27 September. This likely explains why analysts are forecasting that 25,000 jobs were created in October.

It is also worth noting that the betting website Kalshi is projecting that the ADP employment change for October will increase by 41,000 jobs.

Fed Survey’s Less Optimistic

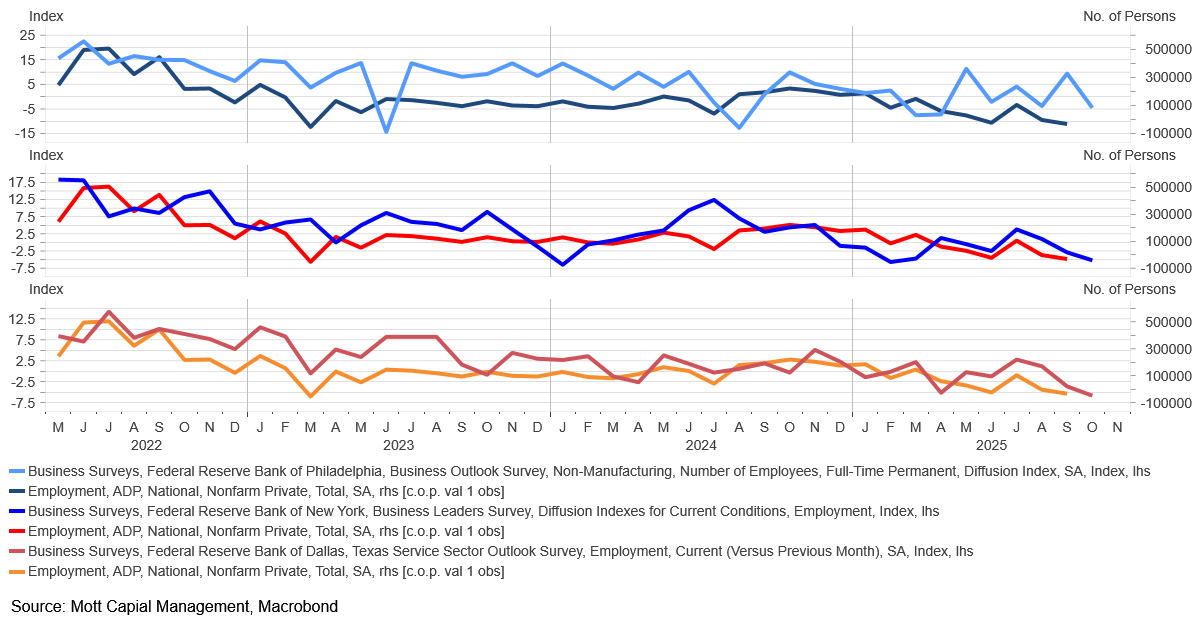

However, the Dallas, New York and Philadelphia Fed Service Sector Outlooks indicated that employment likely declined in October compared with September. These indices tend to closely track the monthly rate of change in the ADP employment report and therefore suggest another weak month for the labour market. Such a result would contradict some of the more positive signals seen so far from the ADP data and could catch the market off guard if the report comes in weaker than expected.

(Source: TradingView)

(Past performance is not a reliable indicator of future results)

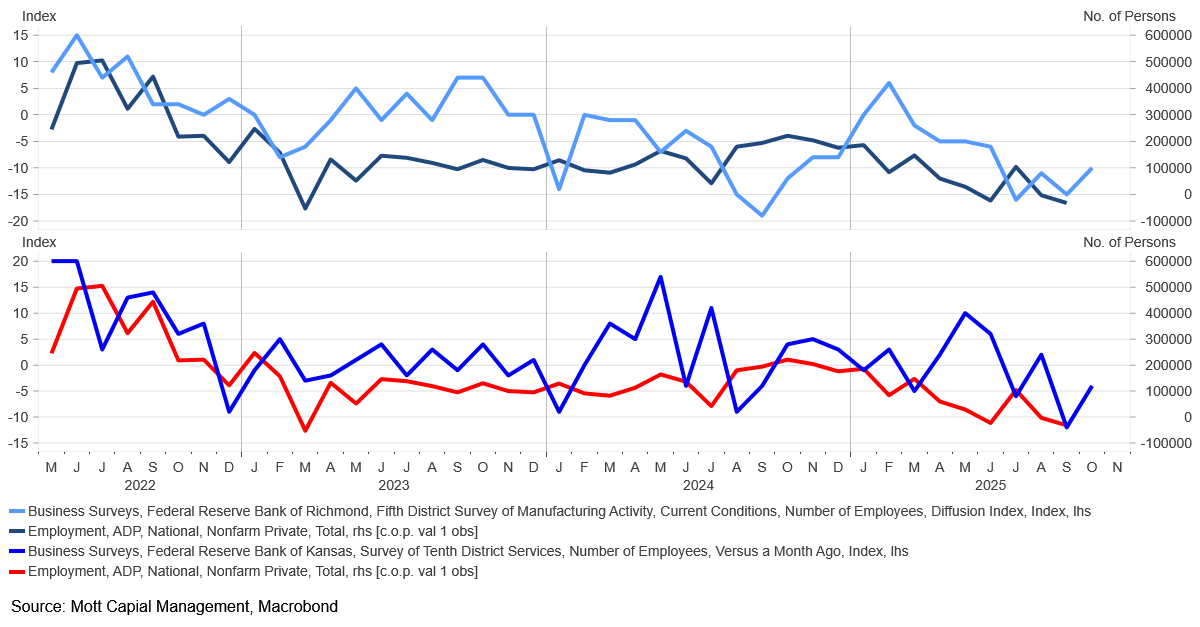

Additionally, the Richmond and Kansas City Fed surveys showed improvements in employment data during October. However, it is worth noting that in recent months these surveys have tended to move in the opposite direction to the ADP report. Therefore, it is important to recognise that these two surveys may not align closely with the actual ADP figure.

(Source: TradingView)

(Past performance is not a reliable indicator of future results)

When looking through the data, it becomes clear why the ongoing government shutdown is so significant — without the official government jobs report, we lack the most comprehensive view of what is truly happening in the economy. It is the only report that provides a complete, nationwide picture of employment conditions and offers a reliable gauge of broader labour market trends.

Stronger Dollar, Steeper Yield Curve

Should the data come in line with, or even better than, expectations — as the betting markets appear to imply, alongside the improving trends seen in the ADP weekly data — the recent rise in the dollar is likely to continue as the market bets against an FOMC December rate cut. This has already led to notable strength against the Japanese yen.

The USD/JPY has risen to a technical resistance level at 154.50, and a push beyond that could see the yen weaken further towards 156.20. The Relative Strength Index is clearly trending higher and remains below 70, indicating that it is not yet in overbought territory.

(Source: TradingView)

(Past performance is not a reliable indicator of future results)

It is a similar story for the EUR/USD, which has also been weakening against the dollar. The pair has fallen below support at 1.156 and is now on course to potentially weaken further towards 1.141 in the near term. The RSI for EUR/USD is trending lower and suggests the move down is not yet oversold.

(Source: TradingView)

(Past performance is not a reliable indicator of future results)

It could also affect Treasury yields, pushing the back end of the curve higher and creating a bear steepener — a scenario in which longer-dated yields rise faster than those at the front end. The 10-year minus 2-year Treasury spread has been consolidating for some time and likely has further room to steepen. Stronger economic data could provide the catalyst for this move, leading the curve to steepen from its current position as the 10-year yield rises and moves away from the 2-year yield.

(Source: TradingView)

(Past performance is not a reliable indicator of future results)

At this point, the weekly ADP data suggests improving labour market conditions following the summer slowdown, while betting markets imply a stronger outcome than analysts’ estimates. The issue lies in the conflicting signals from the regional Fed surveys, which are inconclusive and suggest there is a chance the labour data could come in weaker than expected. Such an outcome could lead to a weakening of the dollar and a decline in interest rates, further flattening the yield curve.