Market Mondays: Energy Shock, Risk-Off Sentiment and a Shifting Tech Narrative

Risk-off flows spread through markets as the escalation of attacks in the Middle East increases the risk premium.

Markets have entered a highly fluid and uncertain phase following a dramatic escalation in the Middle East. The situation remains fast-moving, and developments are unfolding in real time. What follows is a snapshot of how events over the past 48 hours have reshaped the global market landscape, and what investors are grappling with now.

A Rapid Escalation

The crisis began with US and Israeli strikes inside Iran, including an attack on the Ayatollah’s offices, later confirmed to have resulted in his death. Retaliation followed quickly. Iranian forces launched attacks on US assets, Gulf states and Israel. In the last 24–36 hours, US military personnel have reportedly been killed, flights across the Middle East have been grounded, and freight traffic through the Strait of Hormuz has fallen dramatically, reportedly by as much as 80%.

Further developments have intensified tensions. Iran has stated it will not negotiate with the United States, and strikes have reportedly targeted a Saudi energy facility. The US has signalled that regime change is an objective, while Tehran has made clear it will not capitulate. The rhetoric from both sides suggests this may be the beginning of a prolonged conflict rather than an isolated flare-up.

Markets De-Risk

The initial market reaction has been textbook risk-off. Oil surged roughly 13% at the open in Asian trade. Gold jumped sharply. The US dollar strengthened. Equities across Asia fell, particularly in energy-importing economies such as Japan and China. Yields have been volatile but not disorderly.

While oil had been creeping higher in recent sessions amid rising tensions, broader markets had shown signs of complacency. Betting markets had been pricing in a high probability of escalation, but equities and FX had not meaningfully reflected that risk. The events of the weekend have forced rapid de-risking and repositioning.

Brent Oil daily chart

Past performance is not a reliable indicator of future results.

The key issue now is duration. Unlike previous flare-ups, including strikes seen last year, the assassination of a head of state — particularly a religious leader with enormous influence — changes the strategic calculus. Incentives now appear tilted toward escalation rather than de-escalation. That uncertainty is difficult to price.

Energy Shock and Inflation Risk

The central market theme is energy. Even without a formal blockade of the Strait of Hormuz, reduced shipping, insurance withdrawal and targeted strikes could significantly constrain supply flows. OPEC has indicated it may step in to increase production, but logistical bottlenecks remain a concern.

If oil prices remain elevated or continue to rise toward $100 Brent, the shock could complicate the global inflation outlook. That would muddy the interest rate path, particularly in the US where markets still expect rate cuts. A sustained energy spike introduces stagflationary risk — higher inflation alongside weaker growth — which is historically challenging for both equities and bonds.

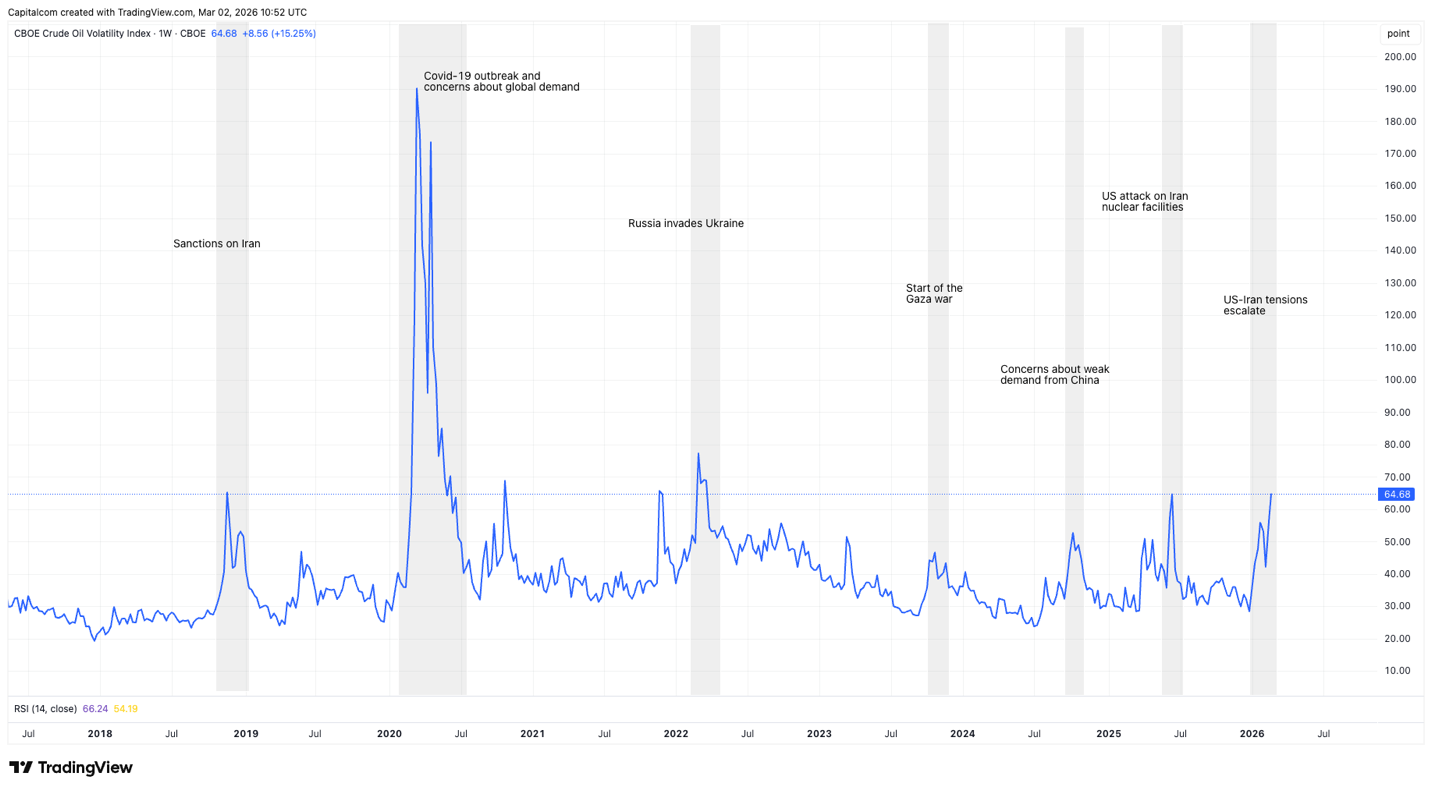

Meanwhile, oil volatility, as measured by the CBOE crude oil volatility index, has surged. History shows that volatility around geopolitical supply shocks can persist for weeks. Even if prices stabilise, rapid swings are likely to continue as markets assess headlines.

Oil volatility chart with overlay of geopolitical events

Past performance is not a reliable indicator of future results.

Gold has resumed its upward trend, breaking back above key resistance levels and approaching prior record highs. While a 2.5% move may not seem dramatic given recent volatility, it is substantial in historical context — especially alongside a stronger dollar, which typically acts as a headwind for precious metals.

Equities: Early Days, Limited Pricing

Equity markets have reacted negatively, but not dramatically so — at least so far. European indices such as the DAX are under more pressure, given Europe’s sensitivity to energy shocks. However, broader global equities have not yet fully priced in a prolonged conflict scenario.

There is a sense that equities may be lagging. Historically, markets sometimes struggle to price external shocks immediately. Early commodity and FX signals often precede larger equity moves. That said, Iran’s relative isolation from the global financial system limits direct contagion risk, and its economic footprint is modest compared to past systemic crises. The question is whether this is a short-lived geopolitical spike or the start of a sustained volatility regime.

In FX, the US dollar and Japanese yen have strengthened, reflecting safe-haven flows. Energy-importing currencies have come under pressure. The firm dollar also hints at tighter financial conditions — a development worth watching if volatility persists.

Nvidia and the Tech Narrative

Before geopolitical tensions took centre stage, the dominant market story was technology and AI investment. Nvidia delivered blockbuster earnings last week, beating expectations across revenue, margins and guidance. CEO Jensen Huang reiterated exponential demand for compute power, reinforcing the structural AI buildout narrative.

Yet despite stellar results, Nvidia struggled to sustain a breakout above the psychologically important $200 level. The stock initially rallied but failed to follow through, with some of the price action attributed to mechanical options flows around large call positions.

More importantly, the broader tech sector did not meaningfully re-accelerate higher. That is perhaps the stronger signal. If even exceptional earnings cannot reignite momentum, it suggests investor sentiment toward AI-driven equities may be shifting. Concerns about overinvestment and diminishing returns have not disappeared. The rotation seen in recent months — away from mega-cap tech and toward cyclicals and non-US equities — may continue if geopolitical risks persist and the bar for upside surprises in tech remains exceptionally high.

NVIDIA daily chart

Past performance is not a reliable indicator of future results.

Where Markets Stand

At this stage, the defining feature of the market is uncertainty. Oil and gold have reacted decisively. Currencies reflect risk aversion. Equities are softer but not panicked.

The crucial question is whether this remains a contained regional conflict or evolves into a prolonged and disruptive energy shock. If escalation continues and supply routes remain constrained, markets may need to reprice more meaningfully.

For now, investors are navigating the fog of war — balancing the immediate energy shock against broader systemic resilience. The coming days will determine whether this episode becomes a brief volatility spike or the beginning of a more persistent risk regime.