Tesla expected to deliver soft Q1 results as investors look for a turning point

Tesla Q1 Earnings Preview

Tesla will report its first-quarter results on April 22, and the big question is whether the EV giant has hit the bottom in terms of deliveries and profitability. A combination of factory disruptions, soft demand, and intensifying competition—especially from China—means this quarter could mark an inflection point. But with new models shipping, energy storage expanding, and the potential for tariff tailwinds, there’s a lot riding on what comes next.

Earnings remain under pressure as sales slump

Consensus estimates point to revenue of $21.4 billion for Q1, a modest 0.6% rise year-on-year but a sizeable drop from $25.7 billion in Q4. Adjusted EPS is expected at $0.44—down nearly 11% quarter-on-quarter—marking a sixth earnings miss in eight quarters if Tesla falls short again. The company’s net income is tipped to fall to $1.57 billion, well off the Q4 pace and reflective of both softer volumes and thinner margins.

The decline in deliveries is already well known. Tesla shipped 386,810 vehicles in the quarter—a steep 20% slide from Q4—due to a temporary shutdown at its main Model Y plant.

Rising costs and defensive pricing squeeze margins

Tesla’s margins remain under pressure. Aggressive price cuts over the past year, especially in key markets like China, have eaten into profitability. In Q1, margins are expected to deteriorate again as Tesla continues to prioritize sales volumes. It’s a classic case of playing defence: fend off rivals like BYD by making your product cheaper—even if it hurts the bottom line.

There are some bright spots. Energy storage revenue is expected to more than double and now makes up roughly 30% of Tesla’s topline, with healthy margins to boot. Still, the segment remains a secondary driver at best and won’t offset the hit from auto margin compression. There are also fears that the company’s battery innovation is lagging behind some Chinese competitors.

Investors look for guidance amidst brand risks and higher costs

Looking forward, the focus shifts to recovery. Production is normalizing, the new Model Y is shipping, and Tesla is preparing to launch a more affordable model, although the roll out is being delayed. But brand damage is becoming a risk in its own right. Elon Musk’s public persona—once an asset—is now a lightning rod. The risk is that some consumers, particularly in progressive markets, are being turned off by Musk’s antics.

Analysts remain cautiously optimistic about Tesla’s outlook

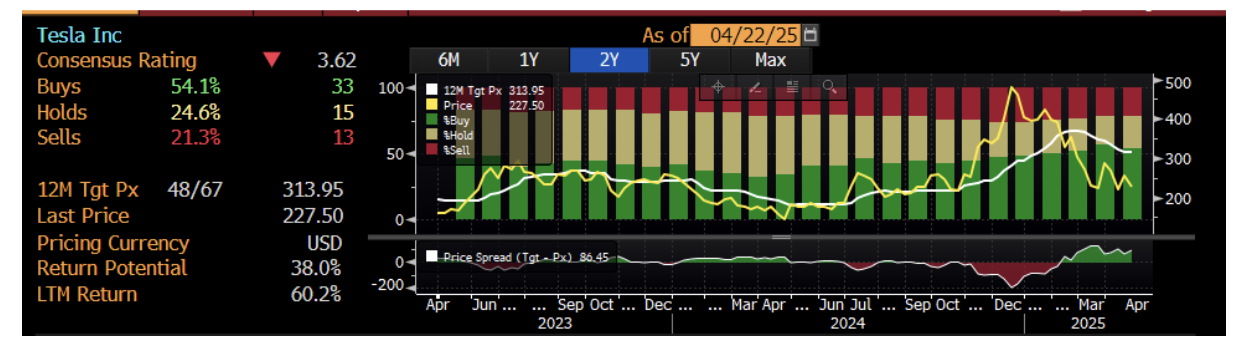

Analyst sentiment is mixed. Around 54% of analysts rate Tesla a buy, while 21% have a sell on the stock. The average 12-month price target is $313.95, suggesting nearly 40% upside from current levels around $227. But valuation remains rich: Tesla trades at over 90 times forward earnings.

(Source: Bloomberg)

Tesla shares reach critical inflection point

Despite being down approximately 45% year-to-date, Tesla shares are only a fraction below where they were prior to the election of US President Donald Trump, when the stock surged because of Elon Musk’s close relationship with the President. The stock is now at a critical inflection point, with price action pointing to short-term consolidation. The $210 to $215 zone appears to be a formidable level of support, which if broken could open up further downside. Meanwhile, a break of downward sloping resistance would be a bullish signal; a bullish divergence on the daily RSI is a positive sign for Tesla stock.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)