Palladium price forecast: Third-party outlook

Palladium trades within a market shaped by industrial use, limited supply and evolving economic expectations. These influences often intersect in ways that drive short-term volatility, setting the context for recent movements in XPD/USD prices.

Palladium (XPD/USD) is trading around $1,753.9 per troy ounce in intraday dealings on 7 January 2026, sitting between the session low of $1,691.6 and high of $1,834.8 on Capital.com’s platform as of 11:32am (UTC). Past performance is not a reliable indicator of future results.

The metal’s price action comes amid broader moves across precious and platinum group metals. Data from third-party providers point to a pullback in palladium futures alongside softness in platinum and other PGMs, as a firmer US dollar and upcoming US macroeconomic releases shape expectations around interest-rate policy (Investing.com, 6 January 2026). Market commentary continues to highlight automotive demand for catalytic converters and evolving expectations around internal combustion engine versus electric vehicle adoption as key medium-term influences on palladium prices. These factors are considered alongside supply signals from major producers and ongoing sanctions-related trade uncertainty (The Oregon Group, 25 November 2025).

Palladium price forecast 2026-2030: Analyst price target view

Analyst palladium price forecasts looking into 2026 reflect a wide range of expectations, shaped by autocatalyst demand, substitution trends with platinum and mine-supply risks. Most institutions focus on annual average prices rather than specific year-end targets, reflecting uncertainty around timing and magnitude of market shifts.

Reuters (analyst poll)

A Reuters poll of 30 analysts and traders, published on 26 October 2025, reports a median forecast for palladium to average about $1,262.5 per ounce in 2026, compared with a 2025 expected average of $1,106 and a prior 2026 projection of $1,100. Respondents cite tight mine supply, tariff uncertainty and shifting investment flows within platinum group metals as factors supporting a higher average profile for 2026 following palladium’s 2025 rally (MINING.COM, 27 October 2025).

Investing News Network (sector overview)

The InvestingNews Network’s palladium outlook highlights that some analysts expect the metal to trade within a higher range into 2026 following an over 80% gain in 2025. Forecasts are typically framed as annual averages rather than single-point targets. The publication notes that expectations remain closely linked to auto-sector demand, the pace of electric vehicle adoption and the potential for continued market deficits after several years of subdued prices (Investing News Network, 19 December 2025).

UBS (investment bank update)

According to a palladium-focused note summarised by Investing.com, UBS raised its palladium price forecasts by around $50 per ounce across its projection horizon. The bank points to a slightly higher expected path for near-term and following-year averages, with analysts suggesting the market may remain modestly undersupplied through the next year. Options-market indicators are described as signalling sentiment that is moderately positive, though less pronounced than earlier in 2025 (Investing.com, 25 November 2025).

BullionVault (retail and analyst projections)

BullionVault’s palladium forecast reports that its user survey indicates a December 2026 price expectation of around $1,689 per ounce. This compares with an LBMA analysts’ 2025 average of $991 and a December 2025 LBMA average of $1,586. The platform adds that palladium forecasts have often proved overly optimistic in recent years, highlighting continued uncertainty around autocatalyst demand and the potential for oversupply between 2025 and 2030 (BullionVault, 2 January 2026).

Past performance is not a reliable indicator of future results. Forecasts are not guarantees and should not be the sole basis for an investment decision

Palladium price: Technical overview

The palladium price is hovering around $1,753.9 as of 11:32am (UTC) on 7 January 2026, with the spot CFD holding above its short- and medium-term moving-average cluster after recovering from lower levels in recent sessions. Simple moving averages remain stacked higher across tenors, with the 20-, 50-, 100- and 200-day averages at approximately 1,726 / 1,558 / 1,419 / 1,241, keeping the broader trend upward while price remains well above this band.

Momentum indicators show the 14-day RSI near 56.7, placing it in the upper-neutral zone, while an ADX reading around 40 suggests an established directional phase rather than a range-bound market. On the upside, the Classic R1 pivot near 2,038.9 is the first level to monitor, with R2 around 2,426.5 coming into focus on a sustained daily close above that area. On pullbacks, initial support is located near the Classic pivot at 1,741.5, followed by the 100-day SMA around 1,419 as a more significant downside reference. A clear break below that zone would increase the risk of a move towards the S1 area near 1,353.9 (TradingView, 7 January 2026).

This technical analysis is provided for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any instrument.

Palladium price history

Palladium CFD prices have experienced pronounced volatility over the past two years, moving from below $900 in early 2024 to rallies above $1,700 by early 2026. Through much of 2024, the metal traded within a $900–$1,050 range, with periodic spikes towards $1,100–$1,200 in September and October that later faded as selling pressure returned.

In 2025, palladium began the year just under $1,000 before gradually trending higher through mid-year and accelerating in the second half. Prices broke above $1,500 in October, rising from around $1,060 on 20 June to more than $1,926 by late December. By 7 January 2026, the market closed at $1,760.30, well above levels seen at the start of 2025 and mid-2024, illustrating how quickly price dynamics and sentiment can shift in this market.

Past performance is not a reliable indicator of future results. Share prices are indicative and may differ from live market prices.

Palladium price outlook: Capital.com analysis

Palladium’s price action into early 2026 has been marked by sharp swings rather than a steady trend. The metal rebounded from multi-year lows in 2024 to trade above $1,700 in early January 2026 on the Capital.com CFD trading platform. Price movements have tracked changing expectations around global growth, interest rates and broader risk appetite, alongside evolving views on the pace at which the automotive sector transitions from traditional combustion engines to hybrids and fully electric vehicles. These shifting expectations can support prices during periods of improving sentiment, while also leaving the market exposed to abrupt reversals when the outlook deteriorates.

From a fundamental perspective, palladium’s reliance on autocatalyst demand and relatively concentrated mine supply means that tighter emissions standards, stable hybrid vehicle sales and supply disruptions can lend support to prices. Conversely, faster electric vehicle adoption, increased platinum substitution and expectations of future surpluses can weigh on the market.

Past performance is not a reliable indicator of future results.

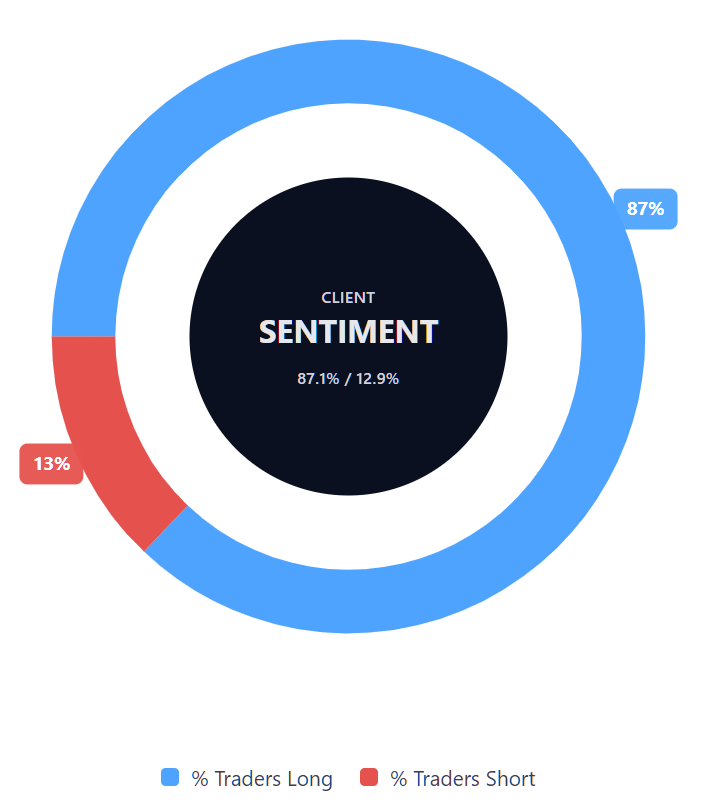

Capital.com’s client sentiment for palladium CFDs

As of 7 January 2026, Capital.com client positioning in palladium CFDs shows 87.1% buyers versus 12.9% sellers, resulting in a net long bias of approximately 74.2 percentage points. This indicates a strongly one-sided tilt towards long positions rather than a broadly balanced distribution between buyers and sellers. The data reflect open positions on Capital.com at the time of reporting and may change as new trades are opened or existing positions are closed.

Summary – palladium price 2026

- Palladium traded within a wide range during 2025 on Capital.com, rising from around $930 in January to close the year above $1,630, with sharp rallies and pullbacks concentrated in the fourth quarter.

- Price action was influenced by shifting expectations around global growth, interest-rate policy and the pace of the automotive sector’s transition towards hybrid and electric vehicles, resulting in alternating periods of buying and selling pressure.

- Third-party forecasts for 2025–2026 reflect a broad spread of views, with surveys and bank research generally centred on four-figure annual averages and highlighting uncertainty around autocatalyst demand and the risk of oversupply.

- Technical indicators in early 2026 show palladium trading well above its 20-, 50-, 100- and 200-day moving averages, with RSI in upper-neutral territory and ADX pointing to an established trend environment.

Past performance is not a reliable indicator of future results.

FAQ

What is the palladium price forecast?

Palladium price forecasts vary widely and are typically expressed as annual averages rather than specific price targets. Analyst views for 2025–2026 commonly centre on four-figure levels, reflecting uncertainty around autocatalyst demand, substitution with platinum and mine-supply conditions. Forecasts also take into account macroeconomic influences such as interest-rate expectations and currency movements. These projections are based on assumptions that may change over time, and published forecasts are not guarantees of future price performance.

Could palladium’s price go up or down?

Should I invest in palladium?

Whether palladium is suitable depends on individual circumstances, objectives and risk tolerance. Palladium is often viewed as a higher-volatility metal due to its reliance on industrial demand and concentrated supply, which can increase the potential for both gains and losses. This information is provided for general purposes only and does not constitute investment advice. Anyone considering exposure should assess the risks carefully, consider diversification and seek independent advice where appropriate before making any financial decision.

Can I trade palladium CFDs on Capital.com?

Yes, you can trade palladium CFDs on Capital.com. Contracts for difference (CFDs) allow exposure to price movements without owning the underlying metal, letting you take positions on both rising and falling prices. CFDs are traded on margin, and leverage amplifies both profits and losses.