Trading the Russell 2000 as Rate Cut Likelihoods Rise

We’re at levels unseen since December of last year as the small-cap index outperforms, with technicals turning bullish and price action moving in favor of majority client sentiment.

Key US equity index futures are generally steady after a session of gains and another record close for both S&P 500 (+0.3% to 6,466) and Nasdaq 100 (+0.04% to 23,849). But for those wanting healthier percentage gains, they had to look to the Dow (+1% to 44,922) and more so the small-cap Russell 2000 (+2% to 2,328) as market participants rotated into areas seen as bigger beneficiaries of rate cuts built on expectations inflation will be tamer.

CPI (Consumer Price Index) figures released last Tuesday seemed to have set the tone for raising hopes that the Federal Reserve (Fed) will cut rates, and there was a pullback in Treasury yields across the board yesterday. Market pricing (CME’s FedWatch) is (at last) fully pricing in a rate cut in September out of the Fed with a small minority gunning for a larger 50bp (basis point) reduction as Treasury Secretary Bessent urged the US central bank to cut rates by 150bp or more, and via majority (from a previous coin toss likelihood) seeing a third reduction in December.

But while markets are anticipating one thing, there has still been pushback from some FOMC (Federal Open Market Committee) members including Goolsbee more concerned about rising underlying and services inflation and cited a “pretty strong, pretty solid” labor market, and Bostic also hinting at strength in the labor market with unemployment rate remaining historically low at 4.2%.

There wasn’t much to go on yesterday in terms of economic data with the weekly mortgage applications (out of MBA) showing another increase, this time by a larger 10.9%. But that’ll change with PPI (Producer Price Index) releasing today the next key item on the inflation front for traders to digest alongside the weekly claims before retail sales, trade pricing data, and UoM’s (University of Michigan) preliminary consumer inflation expectations and sentiment readings tomorrow.

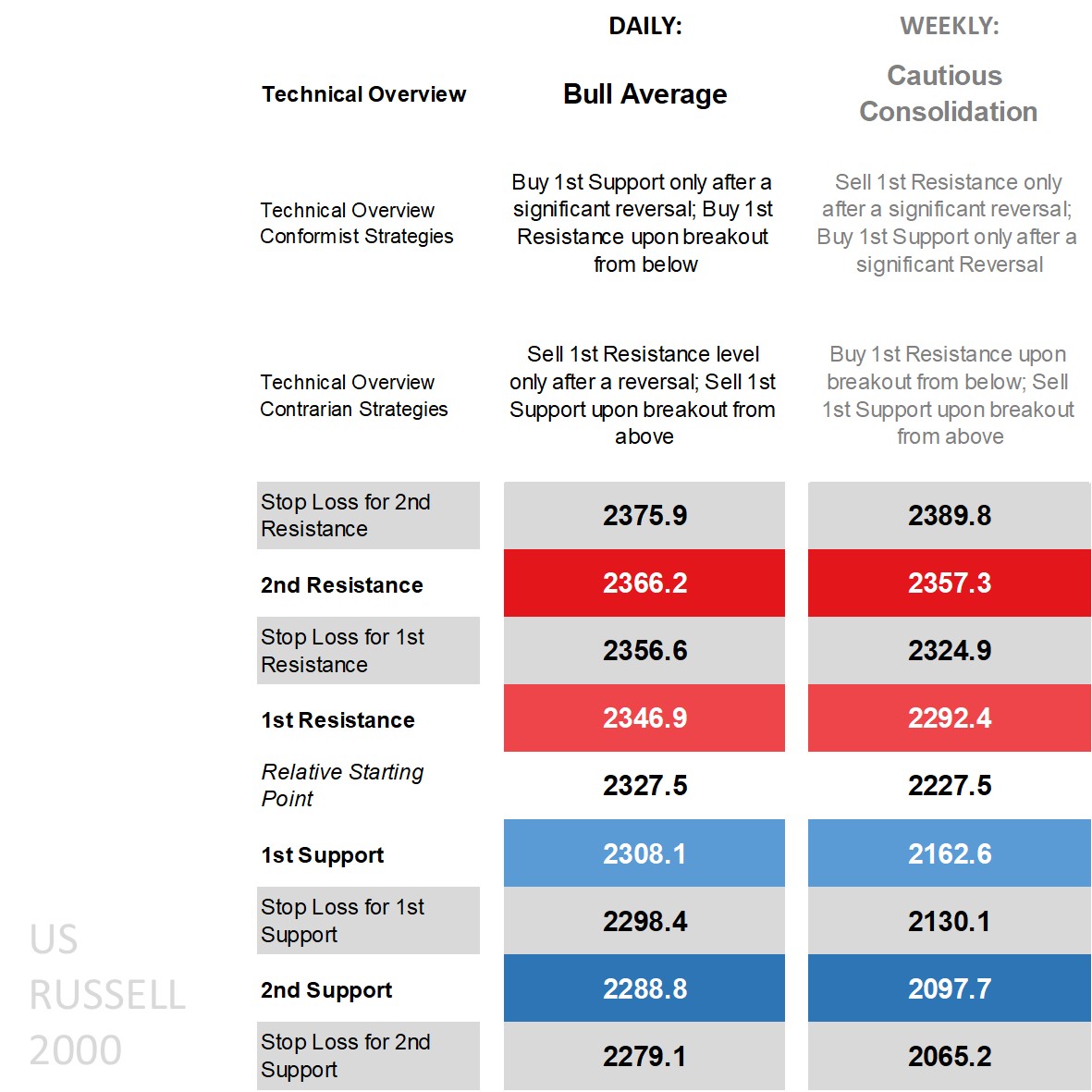

Russell 2000’s technical overview, strategies and levels

Looking at the technicals on the daily time frame and price is above all its main moving averages and piercing the upper end of the Bollinger Band, on the DMI (Directional Movement Index) front positive with a big margin for the +DI over the -DI, an ADX (Average Directional Movement Index) not in trending territory just yet and an RSI (Relative Strength Index) shy of overbought territory. That usually translates into a bullish overview, but the huddling prior of indicators due to largely rangebound price action has made it easier for technicals to turn green, and as a result more ‘bull average’ where any conformist strategy buys off the 1st Support level ideally done only after a significant reversal (letting price break beneath it by a significant amount and only initiate if price recovers back) and keeping in mind that the narrowed levels due to price action before CPI have yet to catch up to a clear uptick in volatility. Those who see the latest price gains failing to hold fall into the contrarian camp with a sell-after-reversal off the 1st Resistance and sell-breakout off the 1st Support.

That’s the daily time frame. Zooming out to the weekly and while there’s no denying the positive technical bias that’s building thanks to the recent price gains with a positive DMI cross occurring, it’ll require more to shift the technical overview to match the large-cap equity indices where it’s ‘bull average’. The overview and levels are as of the start of this week and you’ll notice price is already above this week’s (weekly) 1st Resistance level, with a play on offer for conformists only if price goes back down else targeting a second attempt at the weekly 2nd Resistance level of 2,357.3 which isn’t too far off today’s 1st Resistance level.

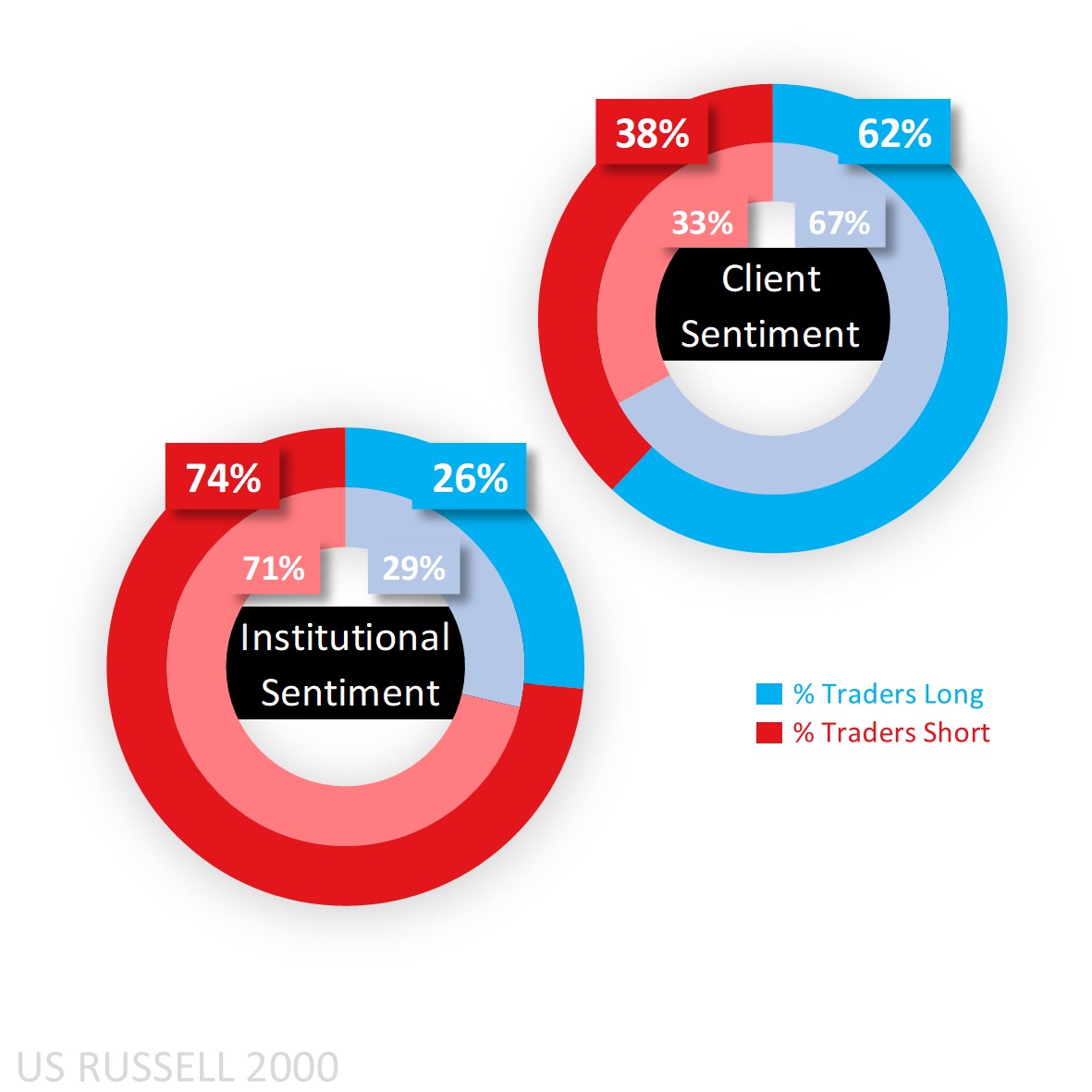

Capital.com’s client sentiment for the Russell 2000

Client sentiment was and still is majority to the buy side when it comes to the small-cap index, but there’s been a notable drop from what were extreme long levels prior to the CPI release and falling out of heavy buy territory to 62% as of today morning as longs get further enticed into closing out and some fresh shorts initiate.

CoT (Commitment of Traders report) speculators are on the wrong end of this one given they were net short as of last week and raised that bias from 71% to 74% due to a drop in longs (by 1,516 lots) and a simultaneous (and notable) increase in shorts (by 11,335). The next report is released on Friday but positioning is as of Tuesday meaning to get the full reaction of their likely unwinding of sell bias in the face of the latest price gains might not be fully visible until the report after next.

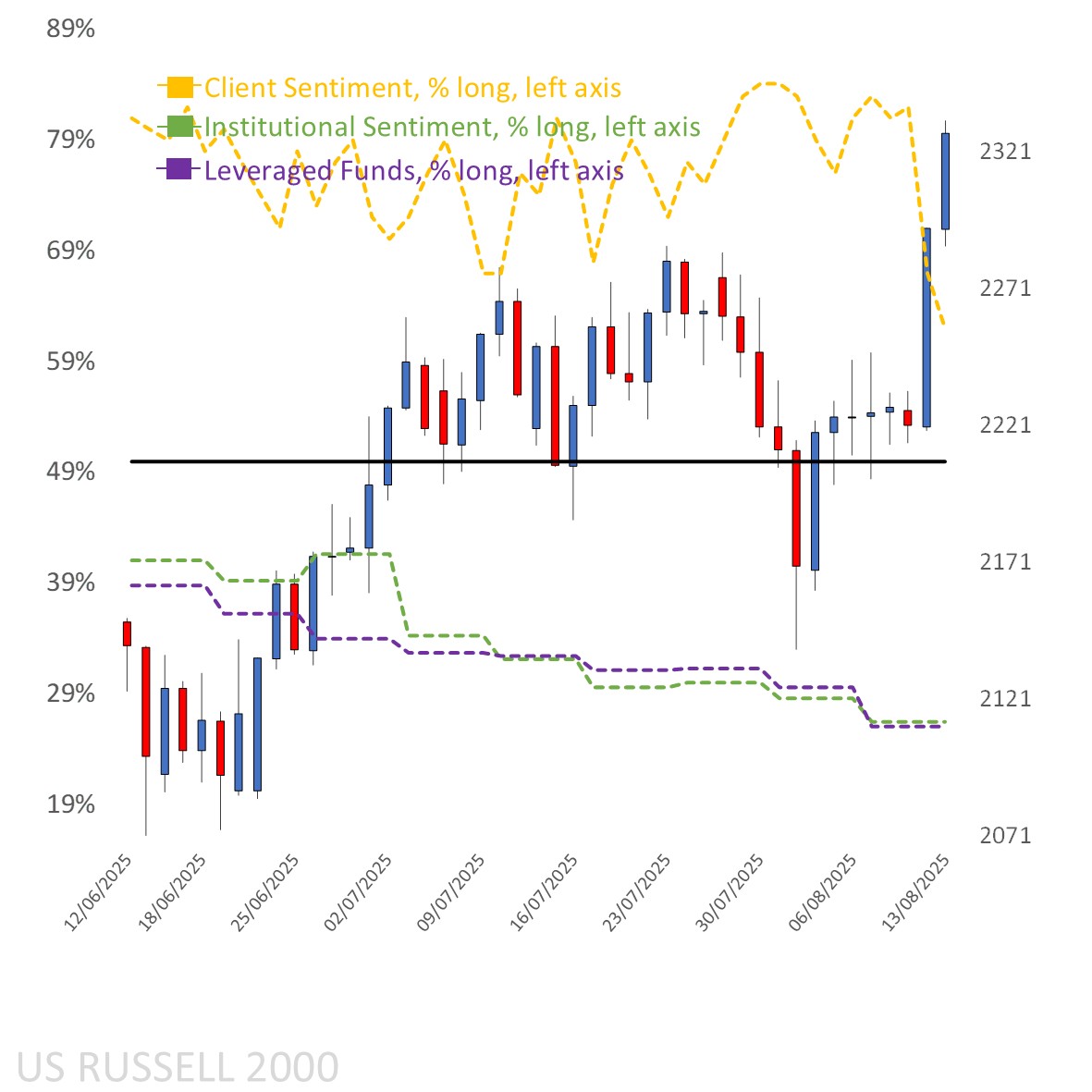

Client sentiment mapped on the daily chart

Source: Capital.com

Period: JUNE 2025 – AUGUST 2025

Past performance is not an indicator of future results.

Russell 2000’s chart on Capital.com platform with key technical indicators

Source: Capital.com

Period: MAY 2025 – AUGUST 2025

Past performance is not an indicator of future results.