Trading the Nasdaq 100 After the Tariff Posts

Trade war is back on the menu even after cautious optimism it’ll get sorted and throws a wrench into shorter-term technicals, while sentiment shows it’s still a story of majority buy bias.

US equity index futures have jumped following US President Trump’s post telling participants not to worry “about China, it will all be fine! Highly respected President Xi just had a bad moment. He doesn’t want Depression for his country, and neither do I”. That has undone a significant portion of Friday’s notable losses for the S&P 500 (-2.7% to 6,552) and Nasdaq 100 (-3.5% to 24,221) as Trump’s comments late last week regarding China “becoming very hostile” over its rare earth export controls and placing 100% tariffs “over and above any Tariff that they are currently paying” starting November 1 as well as “Export Controls on any and all critical software” weighed on risk appetite.

Shares of heaviest Nvidia closed 4.9% lower with larger losses for rival AMD down 7.7% as tech stocks were in for a red session following the trade threats and export controls, and included heavyweight Apple (-3.5%). Shares of Qualcomm were down significantly as well, by 7.3% after China said they were suspected of violating antitrust laws. A notable beneficiary of Friday’s session were rare earth miners in the US including MP Materials (+8.4%), Energy Fuels (+3.3%), and USA Rare Earth (+5%).

Otherwise, let’s not forget that the government shutdown persists in the meantime with no agreement thus far, and “Reductions in Force” permanent layoffs “have begun” according to the OMB’s (Office of Management and Budget) Vought. It has resulted in an absence of significant data, and where we have been getting figures it has generally disappointed. UoM’s (University of Michigan) preliminary consumer sentiment worsened slightly to 55 and so too consumer expectations to 51.2, and inflation expectations remained high even if dropping a notch for the 1-year (to 4.6% from 4.7%) while holding for the 5-year (at 3.7%).

Over in the bond market, Treasury yields dropped notably across the curve last Friday with the bond market closed today due to the bank holiday, and market pricing (CME’s FedWatch) is nearly full in favor of a 25bp (basis point) rate reduction later this month out of the Federal Reserve (Fed) and not far off another one in December while nearing coin-toss likelihoods in January. Speaking of the Fed, there was the FOMC’s (Federal Open Market Committee) Waller in favor of moving “towards cutting rates, but you’re not going to do it aggressively and fast, in case you make a big mistake on which way things go”, and Musalem that the central bank’s goals are in tension as inflation is running high and the labor market is showing signs of potential weakness, and in turn they ought to tread cautiously.

Week ahead

As for the week ahead, it starts off light and will remain light in terms of data should the Senate fail to agree on ending the shutdown when they resume tomorrow. That means the focus will generally be on (1) Fed Chairman Powell speaking tomorrow, and (2) earnings from the financial heavyweights including JPMorgan Chase, Citi, Wells Fargo, and Bank of America.

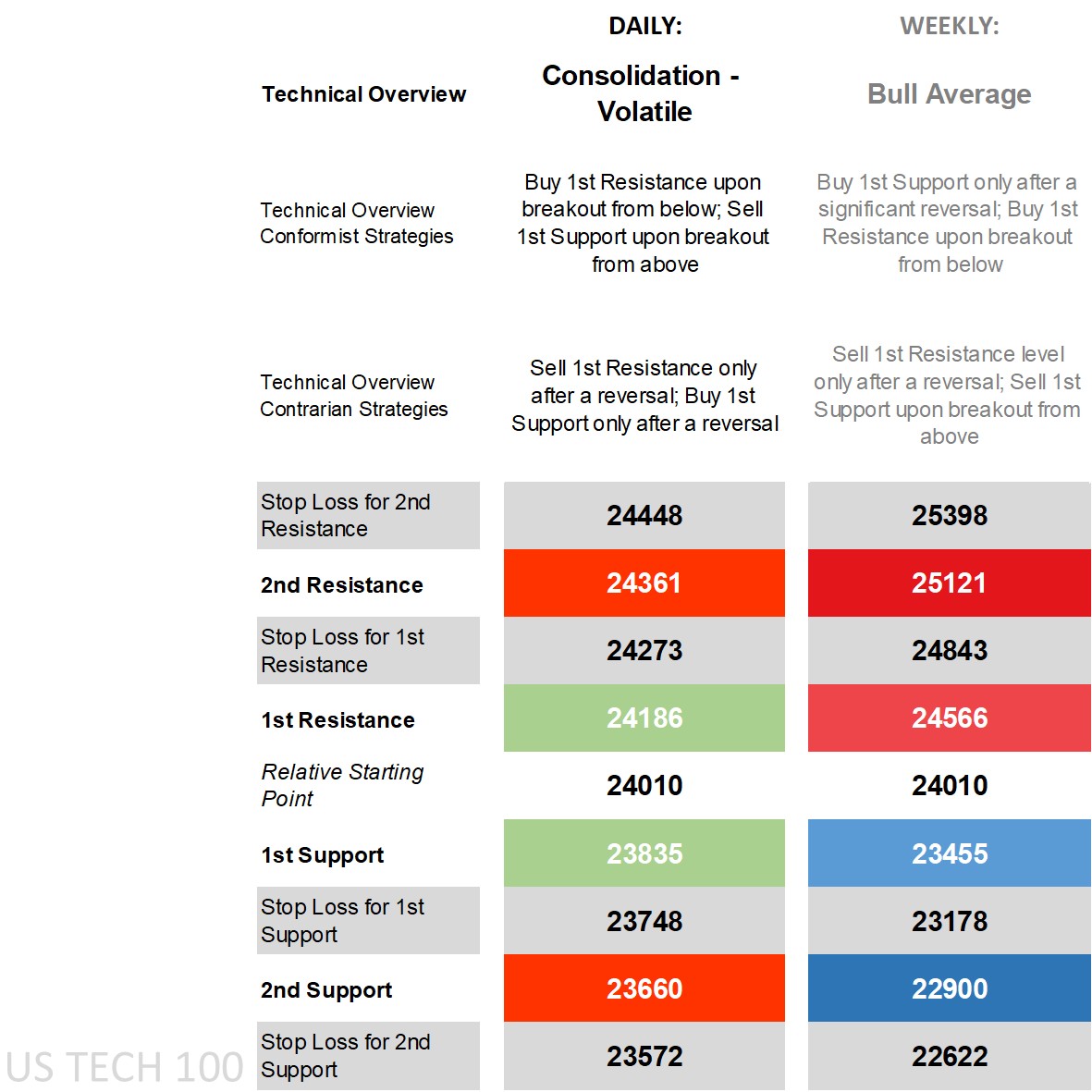

Nasdaq 100’s technical overview, strategies and levels

Looking at the daily time frame and price is still above all its main long-term moving averages (MA) and was briefly below all its main short-term ones, on the DMI (Directional Movement Index) front the -DI crossing over the +DI following Friday’s pullback, an RSI (Relative Strength Index) falling out of overbought territory back to the middle, and an ADX (Average Directional Movement Index) only just in trending territory. The technical overview was ‘bull average’ on the daily time frame prior to the pullback, shifting since to ‘consolidation – volatile’ where breakouts off key levels are in the conformist camp as prices aren’t expected to settle here from a technical standpoint, while reversals are for contrarians. The gap from the Relative Starting Point has meant prices have breached both 1st and 2nd Resistance levels today.

Zooming out to the weekly time frame and the overview was and remains ‘bull average’ with last week’s weekly 1st Support level holding only after incorporating this week’s gap, and price already above this week’s weekly 1st Resistance level giving the edge to conformist buy-breakout strategies though still away from the 2nd Resistance level. That doesn’t mean contrarian sell-after-reversals ought to be ruled out just yet, as any move back down would trigger reversal strategies for those that see the latest price gains as failing to hold.

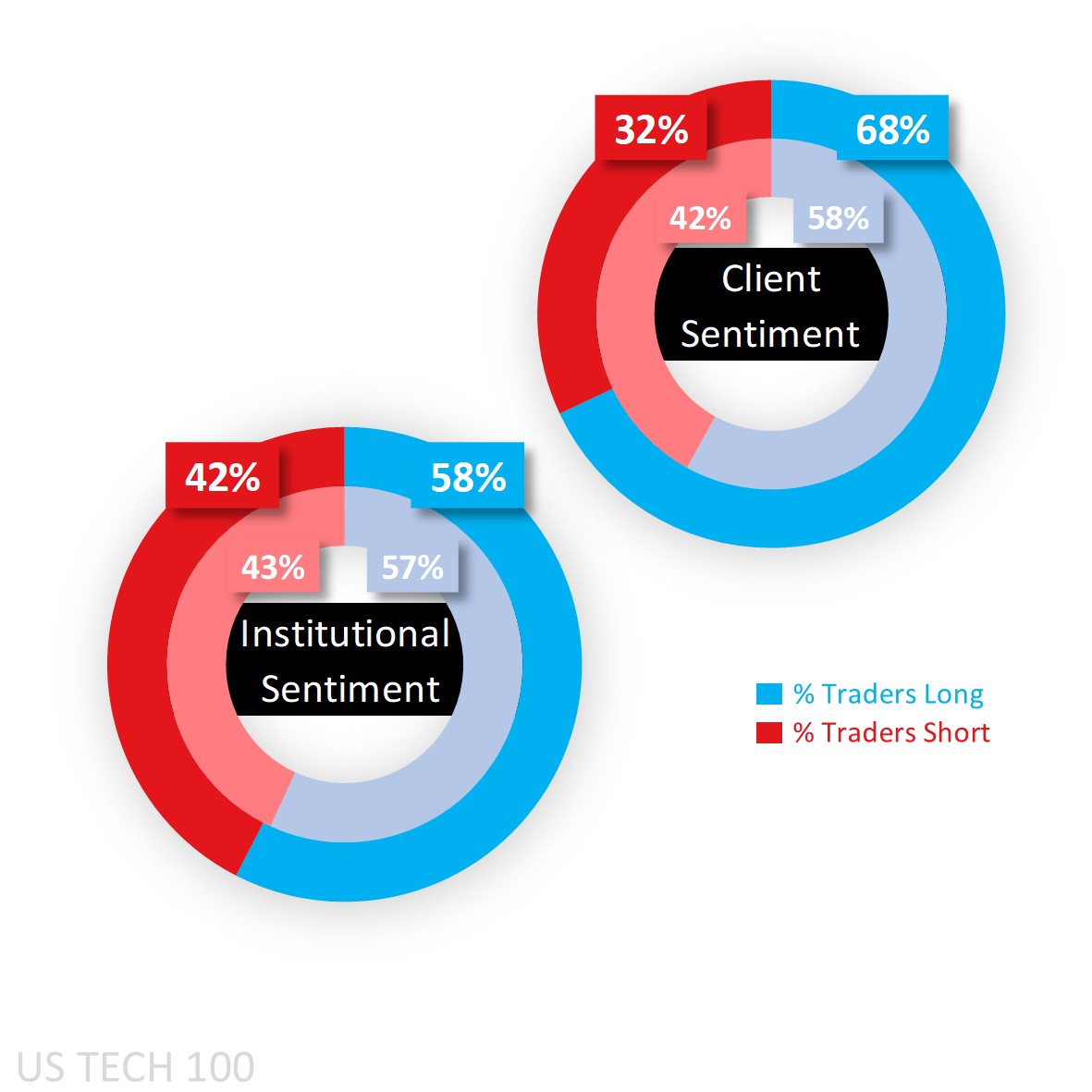

Capital.com’s client sentiment for Nasdaq 100

There’s been a real climb in buy bias among Capital.com’s clients jumping from a majority long 58% to a heavy 68% at the start of this week as plenty of fresh shorts closed out last Friday while longs initiated some of whom have seen notable gains this morning after the gap. They’ve reached extreme buy territory in the S&P 500, Dow, and Russell and means the long bias is lighter here in the Nasdaq 100 (US Tech 100 on the platform) due to its relatively strong price gains prior to last Friday’s drop.

As for CoT speculators, we don’t have the latest figures due to the US government shutdown, and as a result the figures for late September showed an ongoing net long bias in the tech-heavy index that reached 58% and is the highest buy sentiment when compared to the other key US equity indices.

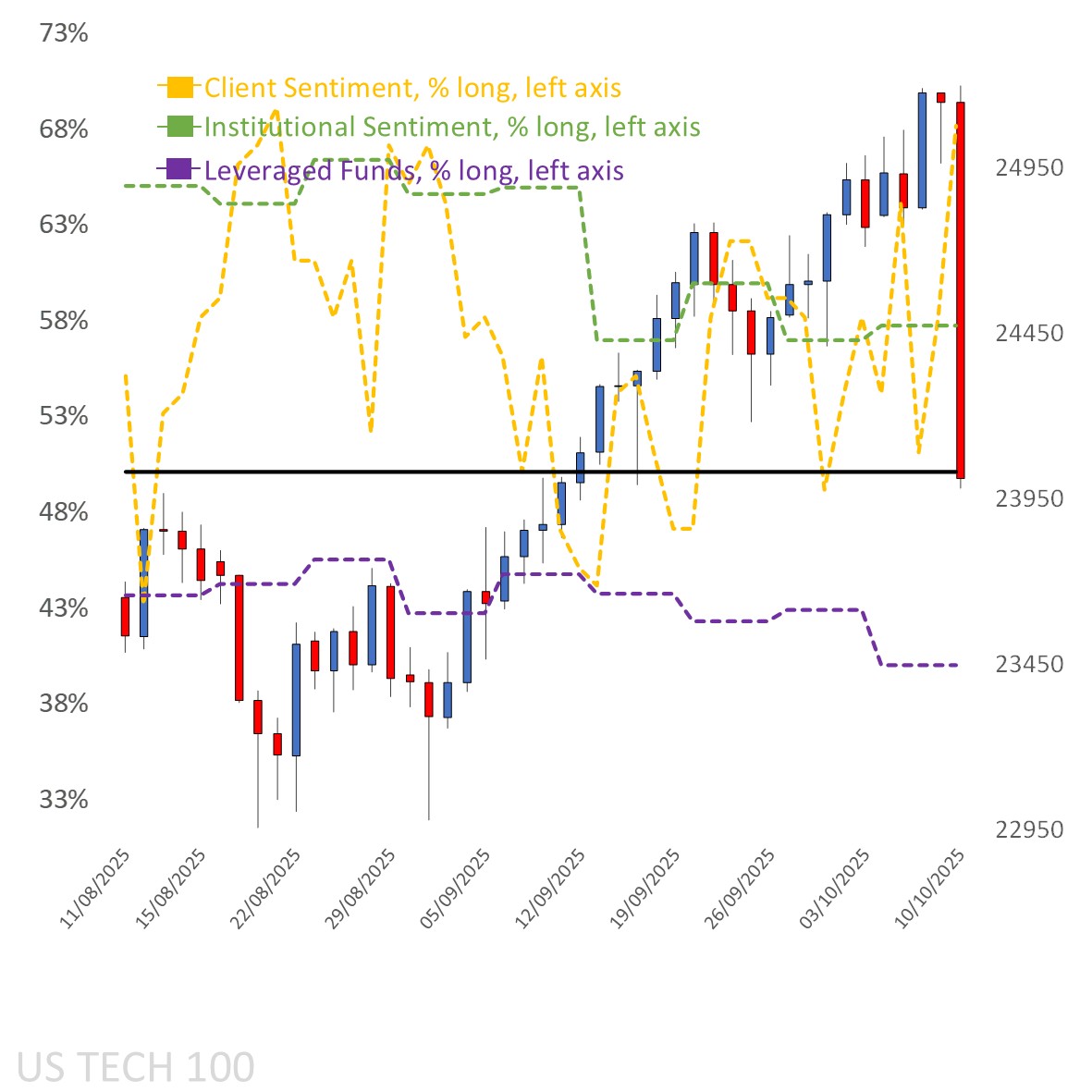

Client sentiment mapped on the daily chart

Source: Capital.com

Period: AUGUST 2025 – OCTOBER 2025

Past performance is not an indicator of future results.

Nasdaq 100’s chart on Capital.com’s platform with key technical indicators

Source: Capital.com

Period: JULY 2025 – OCTOBER 2025

Past performance is not an indicator of future results.