Trading the Dow 30 Ahead of More Earnings

Last week was mostly a story of recovery shaking off a couple key negative factors, but it’s about to get more interesting with more earnings this week.

US equity index futures are edging higher this morning with far larger gains out in Japan for its Nikkei 225 (+3%) thanks to the expected coalition agreement between the LDP and Ishin that puts pro-stimulus Takaichi back in play for the Japanese prime minister. It follows a week of gains for the S&P 500 (w/w +0.6% to 6,664), Nasdaq 100 (w/w +0.8% to 24,817), and Dow 30 (w/w +1.1% to 46,190). Lighter comments/action on the trade front combined with a strong start to the earnings season helped boost risk appetite and pushed market participants to try and look past credit concerns with shares of key regional banks partially rebounding off Thursday’s lows.

Although not components of the large-cap Dow 30 index, investors and traders alike were noting how shares of regional banks would fare last Friday, breathing a sigh of relief following the partial lift off the lows including Jeffries (+6%) enjoying an upgrade out of Oppenheimer to outperform as it sees its exposure to the First Brands bankruptcy as “very limited”, Zions (+5.8%) also getting an upgrade out of Baird, and Western Alliance (+3.1%) also finishing higher.

On the trade front, comments from Treasury Secretary Bessent helped as he thinks “things have de-escalated” with China and is likely to meet with his Chinese counterpart this week reducing the likelihood that the November 1st 100% additional tariffs will occur, and US President Trump wants China to buy soybeans at least the same amount as before and that they’re getting along with them.

Treasury yields ended lower w/w (week-on-week) across the curve, and market pricing (CME’s FedWatch) shows consecutive 25bp (basis point) rate cuts out of the Federal Reserve (Fed) this month and December nearly fully priced in and via slight majority on another interest rate reduction in January, in all aiding the rate cut narrative stocks have been looking for to. Speaking of the Fed, there was FOMC (Federal Open Market Committee) member Musalem speaking late last week that if inflation is contained and more risks to the jobs market emerge, then he could support a path with another rate cut.

Week ahead

Earnings released thus far have managed to impress including one of the Dow 30’s components last Friday (American Express jumping 7.3% on its earnings and revenue beat), with more on offer today including from a key regional bank even if not a component. We’ll get Netflix, Coca-Cola and defense giants tomorrow, Tesla on Wednesday, Intel on Thursday, and Big Oil on Friday. Those looking for US economic data are going to have to make do without it due to the government shutdown, with hopes rising we’ll get CPI this Friday else rely on preliminary PMIs (Purchasing Managers’ Index) and UoM’s (University of Michigan) revised figures.

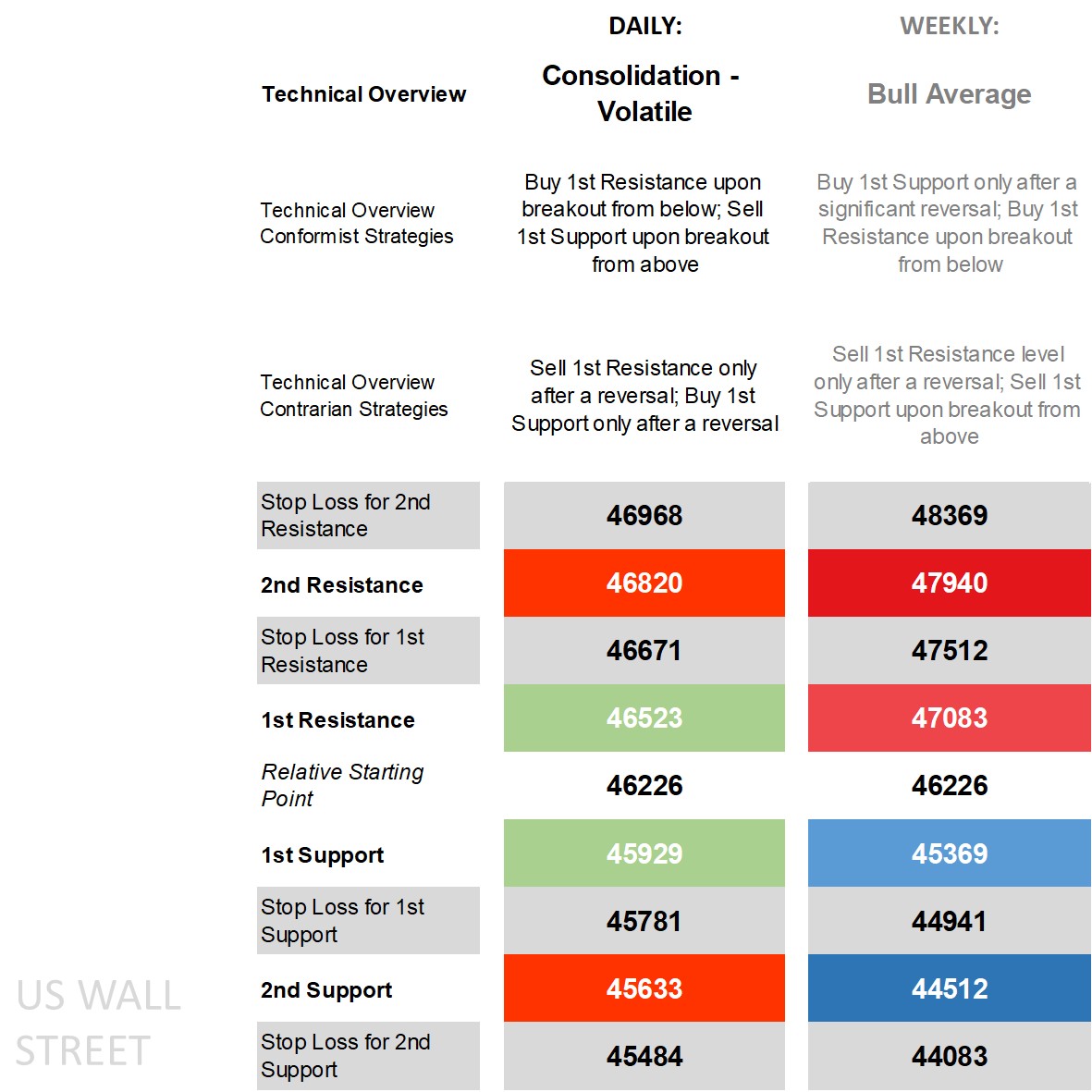

Dow 30’s technical overview, strategies and levels

Looking at the daily time frame and price is still above its main long-term moving averages (MA) but not all its short-term ones and hovering near the middle of the Bollinger Bands, on the DMI (Directional Movement Index) front the -DI over the +DI by one calculation enough to label it as ‘negative’, an RSI (Relative Strength Index) stuck near the middle, and an ADX (Average Directional Movement Index) by one calculation no longer in trending territory. Most of its key technical indicators are neutral and mixed where they aren’t, making the technical overview on the daily time frame ‘consolidation – volatile’ as it doesn’t show signs it’ll settle here and in turn keeping breakout strategies in the conformist camp even if they’ve had to wait interday for follow-through movement while reversals are for contrarians.

Zooming out to the weekly time frame and the technical overview remains ‘bull average’ with a few key technical indicators still positive but huddling closer to each other combined with a non-trending ADX and means buying off the weekly 1st Support only after a significant reversal for those wanting to go conformist avoiding getting stopped out on any major pullback while going for a buy-breakout off the weekly 1st Resistance. Those who see this as being the top or near it fall into the weekly contrarian group working with sell strategies whether via reversal off the weekly 1st Resistance or breakout off the 1st Support.

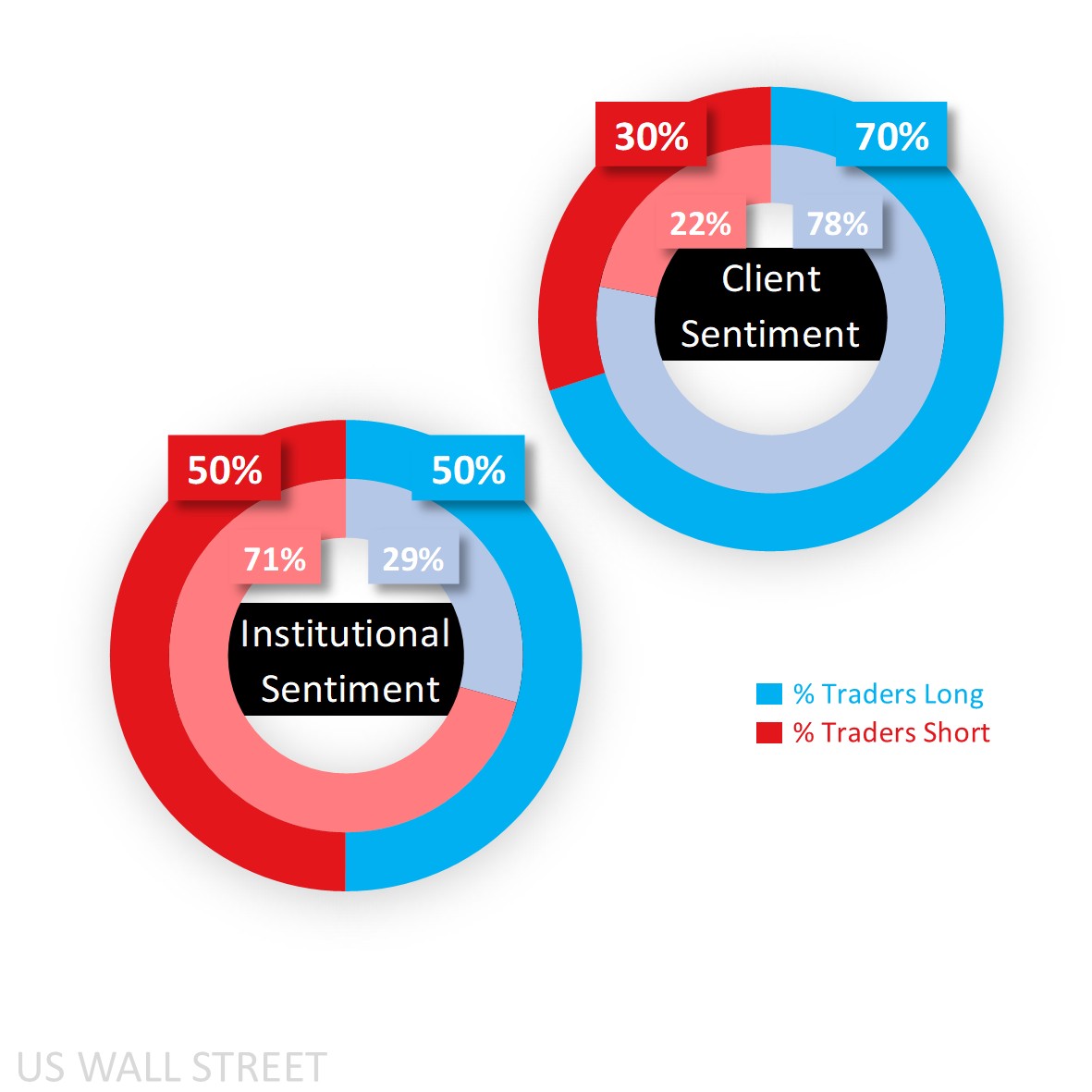

Capital.com’s client sentiment for Dow 30

Client sentiment was an extreme buy 79% at the start of last week given some shorts had closed out on the pullback witnessed on Friday the 10th, but the recovery over the past week saw fresh longs close out and some shorts initiate taking that long bias to a heavy 70% at the start of this week. Long sentiment also dropped since a week ago in the S&P (76% from 78%), Nasdaq (60% from 68%) and so too the Russell (75% from 80%).

The ongoing government shutdown means CoT (Commitment of Traders) reports are delayed again, and in turn institutional sentiment is based off the figures from before the shutdown where it showed larger speculators in the Dow shift from a net sell 71% to the middle.

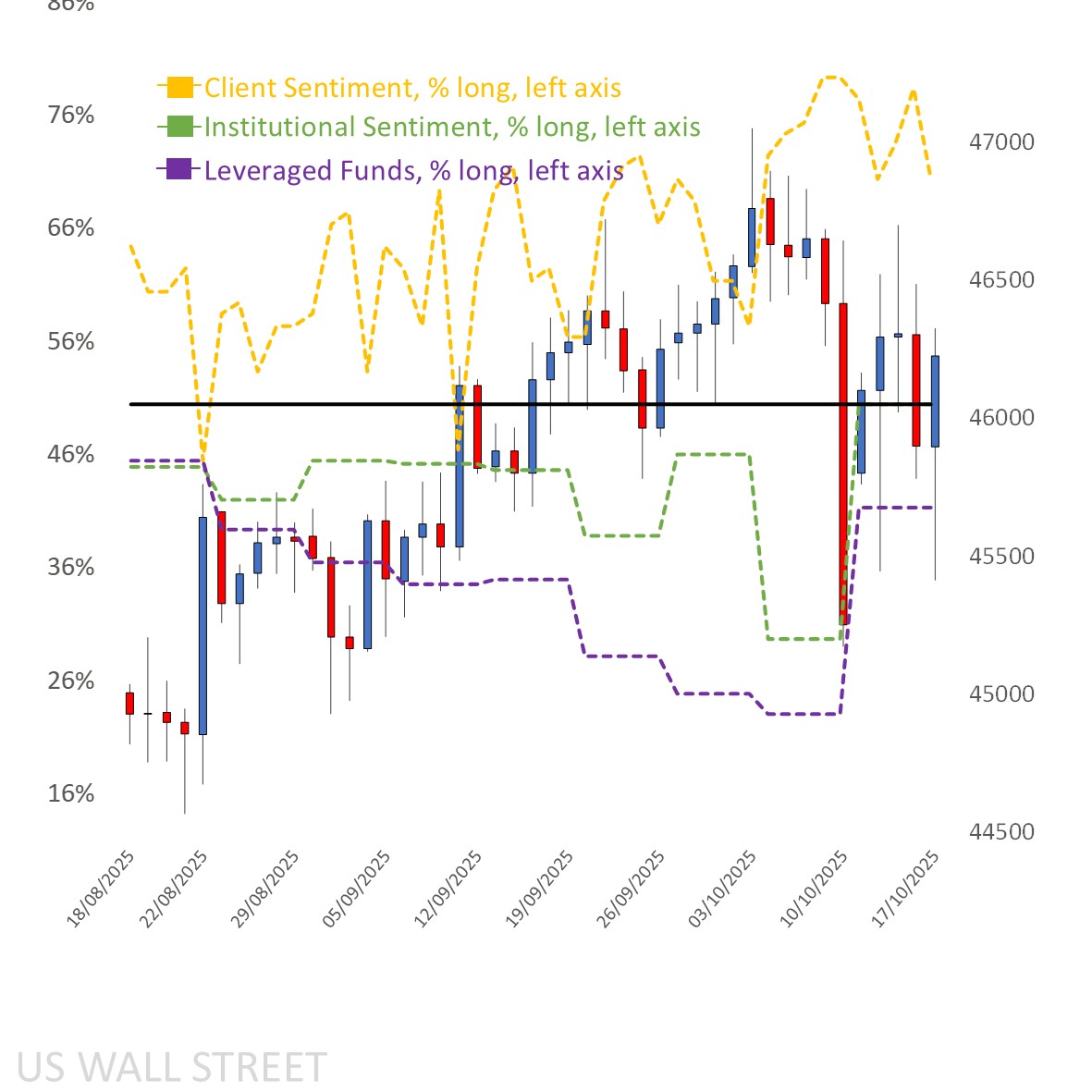

Client sentiment mapped on the daily chart

Source: Capital.com

Source: Capital.com

Period: AUGUST 2025 – OCTOBER 2025

Past performance is not an indicator of future results.

Dow 30’s chart on Capital.com’s platform with key technical indicators

Source: Capital.com

Period: JULY 2025 – OCTOBER 2025

Past performance is not an indicator of future results