US Data Preview: Growth wobbles, inflation cools, Fed caught in a balancing act

US economic growth appears to have stalled sharply heading into the first quarter of 2025.

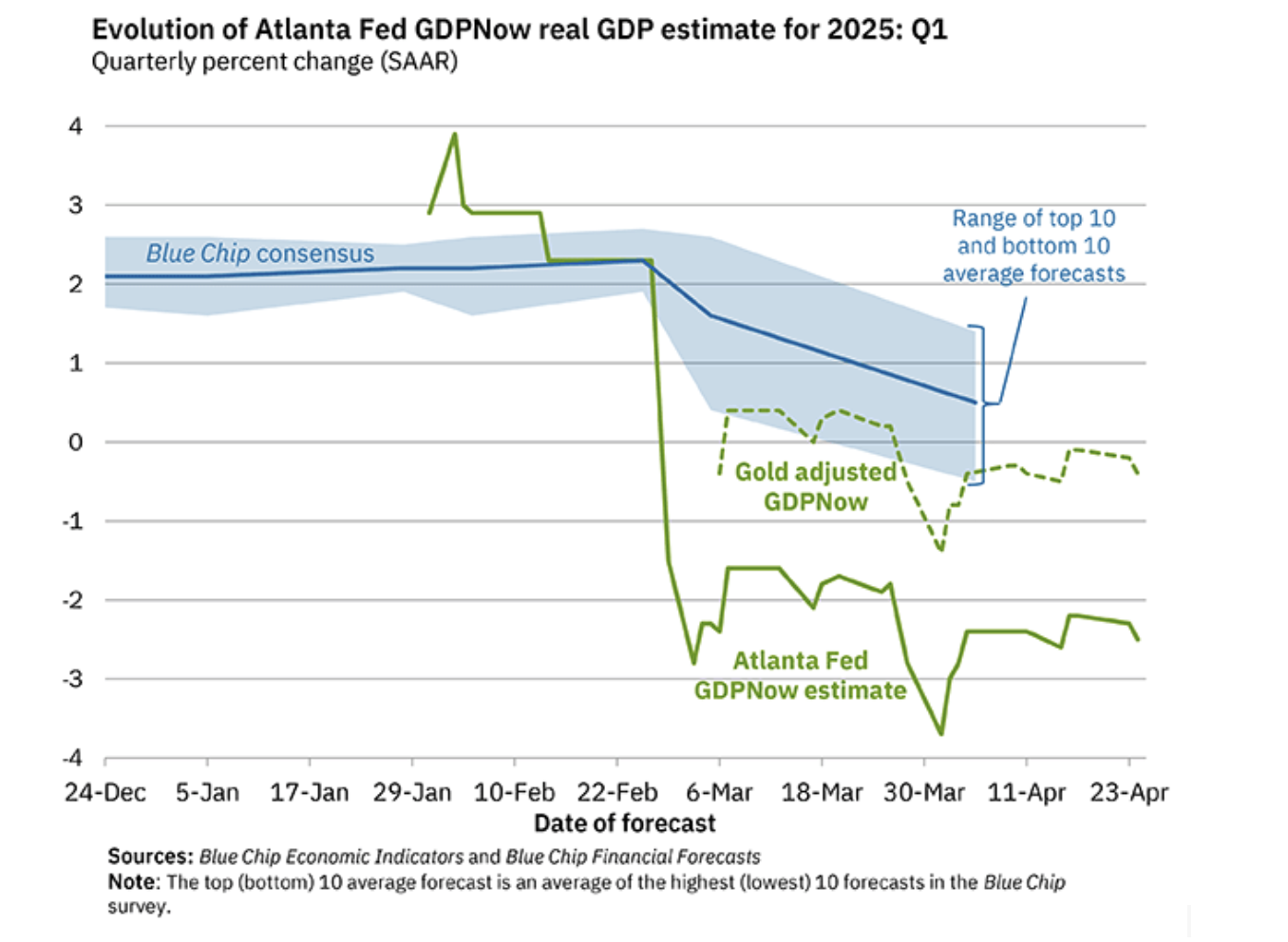

US GDP Data: A Sharp Deceleration

US economic growth appears to have stalled sharply heading into the first quarter of 2025. According to Bloomberg estimates, consensus expectations for Q1 GDP growth (annualised) sit at just 0.4%, a steep slowdown from the 3.4% pace recorded in Q4 2024. The latest Atlanta Fed GDPNow model paints an even starker picture, forecasting nearly a 3% annualised contraction in Q1. The widening gap between the Blue Chip consensus and the real-time GDPNow estimate highlights rising recession risks.

(Source: Atlanta Federal Reserve)

The slowdown has been broad-based. Importantly, personal consumption — which accounts for roughly 70% of the economy — is tipped to slow sharply from 4.0% in Q4 2024 to just 1.2% in Q1 2025. Business investment and housing activity have also softened amid tighter financial conditions and rising uncertainty around new trade barriers.

US PCE Data: Inflation Moderating but Still Above Target

Inflation pressures are continuing to ease, although only gradually. The March PCE Price Index — the Federal Reserve’s key inflation measure — is forecast to rise 2.2% year-on-year, down from 2.5% previously. The more important Core PCE Price Index, which strips out food and energy, is expected to slow to 2.6% year-on-year, from 2.8% in February.

On a monthly basis, inflation is tipped to moderate sharply. The PCE Price Index is expected to rise just 0.1% month-on-month in March, down from 0.4% the month prior — a material cooling that will offer some relief to policymakers watching for evidence of a sustained disinflationary trend.

Although the cooling trend in inflation is encouraging, core inflation remains above the Fed’s 2% target, keeping the central bank cautious about declaring victory too soon as it gauges the impact of tariffs on prices.

US Non-Farm Payrolls Data: Labour Market Cooling

Labour market data suggests that hiring momentum is slowing materially. The upcoming April Non-Farm Payrolls report is expected to show a gain of just 130,000 jobs, down from the 228,000 added in March. Private sector hiring is forecast at 120,000, while manufacturing jobs are tipped to contract by 5,000. The unemployment rate is projected to remain steady at 4.2%, suggesting resilience despite the weaker economic backdrop and deteriorating confidence.

US Tariffs: Stagflation Risks Emerge

Adding to the economic headwinds is the reimposition of US tariffs on strategic imports, particularly from China. Historically, tariffs tend to lift inflation, suppress growth, and weaken labour markets — a combination that resembles stagflation.

The risk is that fresh cost pressures feed into consumer prices at the same time as domestic demand softens. The Atlanta Fed’s GDPNow model already points to a near 3% contraction in Q1 GDP, suggesting underlying weakness even before tariff effects fully filter through.

If realized, the twin shocks of slower growth and rising costs could further stress an already fragile economy, complicating both fiscal and monetary policy responses.

Fed Policy Outlook: Caught Between a Rock and a Hard Place

The latest Fed Funds Futures curve reflects the growing tension. While no move is expected at the May 7 FOMC meeting, the market is pricing roughly 125 basis points of easing by December, implying a fed funds rate closer to 3.2–3.3% by year-end.

The Fed faces a difficult balancing act:

- Holding rates higher to counteract tariff-driven inflation risks deepening a potential recession.

- Easing rates prematurely risks reigniting inflation at a time when price pressures have not fully receded.

Given the softer inflation data — particularly the moderation in monthly PCE inflation to 0.1% — and emerging cracks in the labour market, the Fed is likely to maintain a cautious, data-dependent posture.

The US Dollar struggles to sustain rebound as economy slows

Although equity markets have recovered, the US Dollar continues to reflect a slowing economy due to tariffs. Data that suggests more resilient growth could help boost the currency. Meanwhile, soft growth and labour market data combined (crucially) with a soft inflation read may weaken it further. Data that points to possible stagflation could likely weaken the currency, although the response could be more mixed. From a charts perspective, resistance at 100 on the US Dollar Index needs to break to build confidence in a rebound. A break below support at 98 would all but confirm a further downtrend.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)