Downward pressure on AUD/USD continues heading into Australian GDP data

Australia’s September quarter GDP data is released on Wednesday, 4th of December and is forecast to reveal ongoing weak demand.

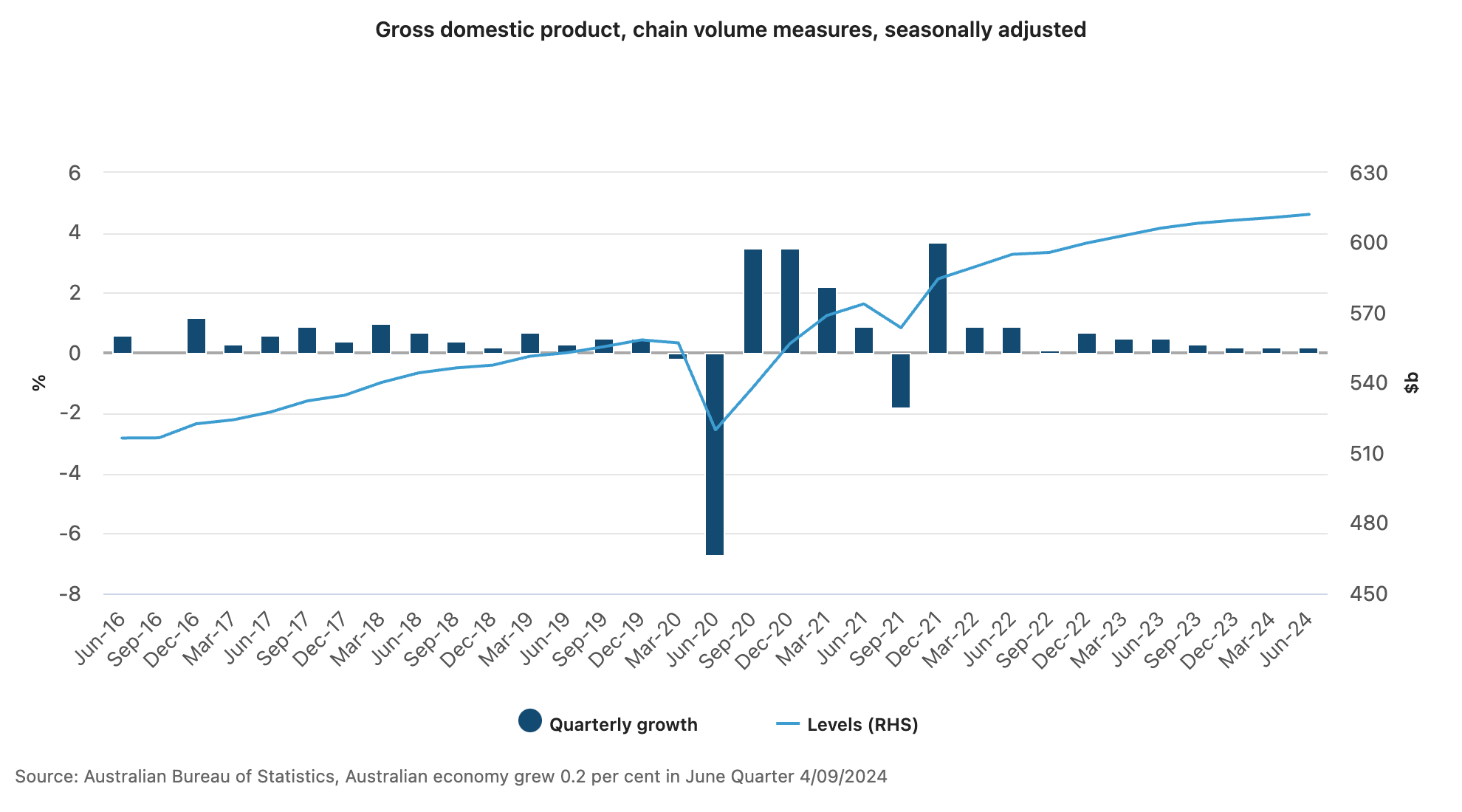

Australian economic growth remains anaemic

Australia’s recent GDP data paints a weak picture of the economy. The June quarter saw GDP grow modestly by 0.2%, marking the 11th straight quarter of expansion. Yet, beneath the headline figures lies a concerning trend: a 0.4% fall in GDP per capita, extending the per capita recession to six quarters—the longest streak on record. Driving growth has been net overseas migration, which accounted for 84% of Australia’s population growth in 2023. This has fueled aggregate demand, with migration underpinning key sectors like housing and retail. Public demand has also been a key contributor, adding 0.3 percentage points to GDP growth as government spending on health and social services remains robust. However, household consumption—a vital engine of growth—continues to falter, detracting 0.1 percentage points from the GDP figure. High inflation, rising interest rates, and stagnant real wages are squeezing household budgets, with discretionary spending taking a notable hit.

(Source: ABS)

Sluggish growth likely continued in September quarter

Australia’s September quarter GDP data is set to underline the economy’s ongoing challenges, with growth expected at a modest 0.4%. While this signals a slight improvement from the June quarter, the per capita recession looks likely to extend to seven quarters— marking a new record. The data will reflect the ongoing squeeze on household budgets from elevated interest rates and stubbornly high inflation, weighing heavily on private consumption. Public spending will probably continue to prop up growth, highlighting the dependence on government support. Overall, the numbers will paint a picture of an economy grappling with weak momentum and persistent headwinds.

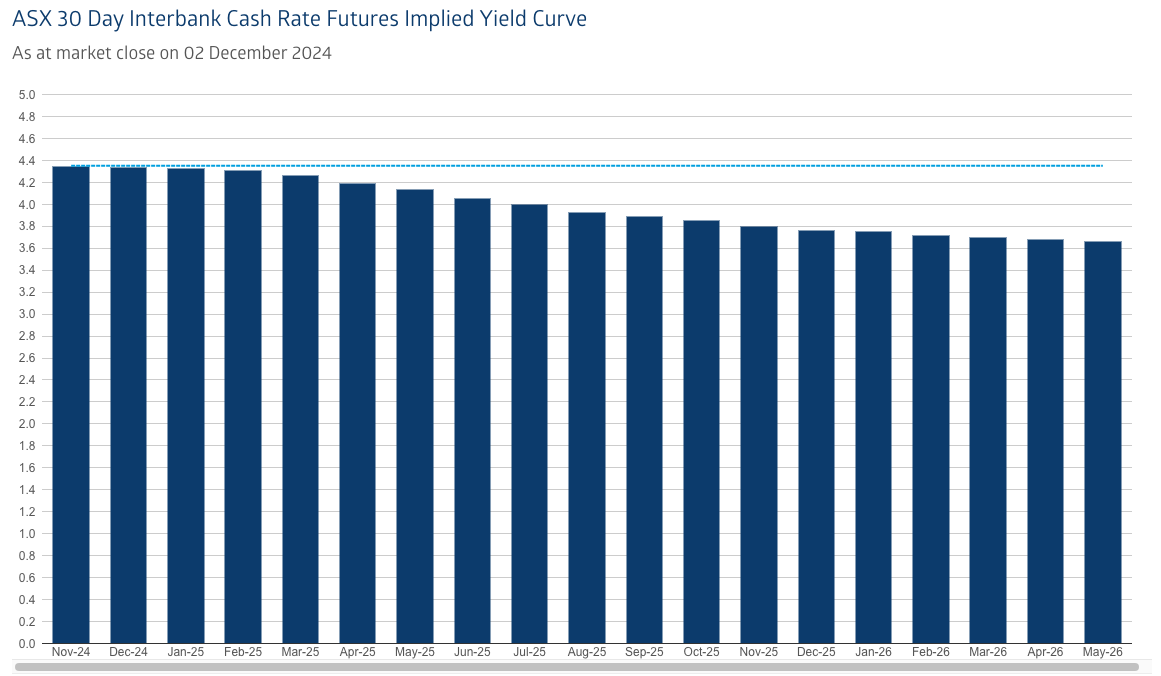

Weak demand unlikely to change RBA policy bias

Despite signs of weak demand in the Australian economy, the Reserve Bank of Australia has maintained a neutral policy bias, stating that it’s “not ruling anything in or out” about future policy. The guidance is rooted in ongoing inflationary pressures, which is keeping trimmed mean inflation above the central bank’s 2-3% target, and is due, according to the central bank, because of supply side issues maintaining an imbalance between aggregate supply and aggregate demand.

The markets are pricing-in that the next move from the RBA will be a cut at some point in 2025, although the timing of the first cut has fluctuated as markets discount the possible impact of the incoming Trump administration and its loose fiscal agenda and proposed tariffs.

(Source: ASX)

AUD/USD in a downtrend but shows signs of possible bottom

The Australian Dollar is largely trading as a proxy for a looming US-China trade war. The AUD/USD is depreciating as the markets price-in weaker economic activity in China and possibly a competitive devaluation of the Yuan by the Chinese to offset increased tariffs, both of which would weaken demand for Australian commodity exports. Another element of the pair’s weakness is the pricing-in of a stronger fiscal impulse in the United States next year because of Trump’s proposed tax cuts, which has led to expectations of persistent strength in US growth.

From a technical point of view, the AUD/USD is in a short-term downtrend. However, there are signals of a possible trend reversal. Price action is carving out a rounding bottom, while the daily RSI is in bullish divergence with price. A break through the 20-day moving average and a resistance zone in the mid-65 handle would be a bullish signal for the AUD/USD. Meanwhile, another sell-off and new lower-low would indicate an ongoing bearish bias in the market.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)