AMD stock forecast: Advancing AI event, Q2 earnings

AMD is a US semiconductor company whose shares have drawn attention from AI data centre demand and its upcoming ‘Advancing AI 2026’ event in July. Explore third-party Advanced Micro Devices price targets and technical analysis. Past performance is not a reliable indicator of future results.

Advanced Micro Devices Inc (AMD) traded at $544.72 as of 1:18pm UTC on 22 June 2026, near the upper end of its intraday range of $518.15–$544.54, as buying interest remained active during afternoon trading. Past performance is not a reliable indicator of future results.

Sentiment around AMD has been supported by the AI infrastructure spending cycle, with cloud and hyperscaler capital expenditure commitments of approximately $750bn projected for 2026 helping to underpin data centre chip demand (Goldman Sachs, 1 May 2026). The stock had risen sharply since early June, recovering from a sector-wide sell-off on 5 June 2026, when AMD shares fell 10.86% to $466.38 amid a cautious AI chip outlook from Broadcom and concerns over memory supply chain disruptions (Kavout, 9 June 2026). Attention has also turned to AMD's forthcoming 'Advancing AI 2026' event on 22–23 July in San Francisco, where CEO Dr Lisa Su is expected to present next-generation MI450 accelerators and EPYC 'Zen 6' CPUs, keeping the company's product pipeline in focus (WCCFTech, 31 March 2026).

Third-party AMD outlook: AI demand lifts analyst targets

As of 22 June 2026, third-party AMD stock predictions point to a broadly positive market view, supported by AI infrastructure demand, strong Q1 2026 earnings, and upward revisions to server CPU and data centre GPU estimates. The following targets summarise leading broker and consensus forecasts for AMD shares.

Bank of America (house upgrade)

Bank of America analyst Vivek Arya reiterated a Buy rating on AMD and raised the 12-month price target to $560 from $500, based on a 42x multiple of his 2027 non-GAAP EPS estimate. The revision reflected higher CPU and GPU revenue estimates, as the firm lifted its 2030 server CPU total addressable market projection to $170bn or more from $125bn, citing AMD's growing share of hyperscaler data centre procurement (The Street, 12 June 2026).

Citi (rating upgrade)

Citi analyst Atif Malik upgraded AMD to Buy from Neutral and raised the 12-month price target to $575 from $460, as his sum-of-the-parts model values AMD's data centre GPU business alone at $281 per share. Malik also raised his long-term CPU market forecast, citing AMD's accelerating server market share and improved revenue visibility from multi-year hyperscaler GPU supply commitments (The Street, 13 June 2026).

Bernstein (target raise)

Bernstein analyst Stacy Rasgon raised AMD's 12-month price target to $600 from $525, maintaining an Outperform rating, with projected 2027 EPS of $14.60 and a path toward $20 in 2028 if AI adoption trends continue. The revision was the second material upward adjustment in two months, with Rasgon citing sustained momentum in AMD's MI-series GPU ramp and expanding enterprise and cloud customer commitments (GuruFocus, 17 June 2026).

MarketBeat (broker consensus)

MarketBeat aggregates 44 analyst ratings on AMD and reports a Moderate Buy consensus with an average 12-month price target of $430.68, spanning a range from $235 to $665. The consensus reflects a broad majority of Buy-equivalent ratings, with 31 of the 44 analysts assigned a Buy, while the average target trails the current market price following the stock's sharp year-to-date rally (MarketBeat, 20 June 2026).

Public.com (Wall Street consensus)

Public.com tracks 35 Wall Street analysts covering AMD and reports a Buy consensus rating as of 22 June 2026, with an average 12-month price target of $444.80. In its panel, 43% of analysts assign a Strong Buy and a further 43% assign a Buy. The aggregation notes that targets and ratings are subject to frequent revision in line with earnings updates and market conditions (Public.com, 22 June 2026).

Predictions and third-party forecasts are inherently uncertain, as they cannot fully account for unexpected market developments. Past performance is not a reliable indicator of future results.

Advanced Micro Devices earnings: Q1 2026 results and Q2 2026 outlook

AMD reported Q1 2026 results on 5 May 2026, posting adjusted earnings per share of $1.37, above the consensus estimate of $1.29, while quarterly revenue rose 37.8% year on year to $10.25bn, ahead of analyst expectations of $9.90bn (AMD Investor Relations, 5 May 2026). Data centre segment revenue climbed 57% year on year to $5.80bn, and AMD's stock rose approximately 15% in after-hours trading following the release (CNBC, 6 May 2026). CEO Dr Lisa Su noted that the data centre had become the 'primary driver of our revenue and earnings growth', with increasing visibility into the growth trajectory from MI450 series customer commitments (AMD Investor Relations, 5 May 2026).

For Q2 2026, AMD guided revenue to approximately $11.20bn, plus or minus $300m, above the then-prevailing consensus of $10.52bn (AMD Investor Relations, 5 May 2026). AMD's next earnings date, covering Q2 2026 for the fiscal quarter ending June 2026, is estimated for 4 August 2026 after market close; that date had not yet been formally confirmed by the company as of 22 June 2026 (MarketBeat, 21 June 2026).

Advanced Micro Devices stock price: technical overview

The AMD stock price traded at $544.72 as of 1:18pm UTC on 22 June 2026, holding well above its key moving-average cluster. The 20/50/100/200-day simple moving averages sat at approximately $502 / $411 / $310 / $261, with price extended notably above each layer after the stock’s sharp year-to-date run.

The 20-over-50 alignment remained intact across both the simple and exponential moving-average families. The 14-day relative strength index stood at 61.19, placing momentum in the upper-neutral band – firm but not stretched – while the average directional index at 28.32 pointed to an established trend. The Hull moving average (9) at $534.74 sat just below the last price, providing a near-term dynamic reference.

On the topside, the classic R1 pivot at $582.63 is the first reference above current levels; a daily close through there could bring the R2 zone near $649 into view. On pullbacks, the classic pivot point at $460.67 represents initial support, with the 50-day SMA shelf near $411 the next meaningful level below. A move toward S1 near $394 would come into consideration only on a loss of that moving-average shelf (TradingView, 22 June 2026).

This is technical analysis for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any instrument.

AMD share price history (2024–2026)

AMD’s stock price opened June 2024 trading around $160, part of a broader consolidation that followed the stock’s prior AI-fuelled run-up. Shares drifted lower through the summer, slipping to a two-year low of $120.66 on 5 August 2024 amid a sharp global equity sell-off tied to recession fears and an unwinding of yen carry trades. A recovery followed into the autumn, with AMD climbing back toward $180 by mid-October before fading again and closing 2024 at $120.59, roughly flat versus its June 2024 levels.

The stock entered 2025 near $120 and moved sideways through the first half, as investors questioned AMD’s pace of AI revenue conversion relative to Nvidia. A trough came in April 2025, when AMD touched $76.19 on 9 April amid broad market turbulence following the announcement of sweeping US tariffs. Shares then recovered gradually through the summer and autumn, reclaiming the $160–$170 range by late October 2025, before retreating again to close the year near $214.

2026 has been a defining period for AMD’s share price. AMD opened January at around $224 and accelerated sharply after Q1 2026 earnings on 5 May, when revenue of $10.25bn beat expectations and the stock rose from roughly $345 to above $414 in a single session. A brief pullback to the $219–$246 range in mid-April, coinciding with renewed tariff anxiety, gave way to a strong rally, with AMD closing at $544.64 on 22 June 2026, up approximately 154% year to date.

Past performance is not a reliable indicator of future results. Share prices are indicative and may differ from live market prices.

AMD (Advanced Micro Devices): Capital.com analyst view

AMD’s price performance in 2026 stands out for its scale and speed, with shares rising approximately 154% year to date as of 22 June 2026. The move has been supported by strong Q1 2026 earnings – revenue of $10.25bn beat expectations by around 4% – and a series of upward analyst revisions linked to AI data centre demand. The company’s expanding MI-series GPU ramp and growing server CPU market share have supported positive analyst coverage, with Reuters reporting that AMD now projects the server CPU addressable market to grow over 35% annually through 2030. That said, the stock has not risen in a straight line; a sharp sector-wide sell-off on 5 June 2026 saw AMD fall sharply in one session, illustrating how quickly sentiment can shift on macro or guidance concerns.

Risks remain meaningful on both sides. Export control uncertainty, particularly around AI chip sales to China, represents a potential headwind that could weigh on revenue visibility, while a high forward valuation leaves little room for execution missteps. AMD’s upcoming ‘Advancing AI 2026’ event on 22–23 July could reinforce positive momentum if new product disclosures meet market expectations. However, any shortfall relative to elevated investor expectations could also prompt a pullback.

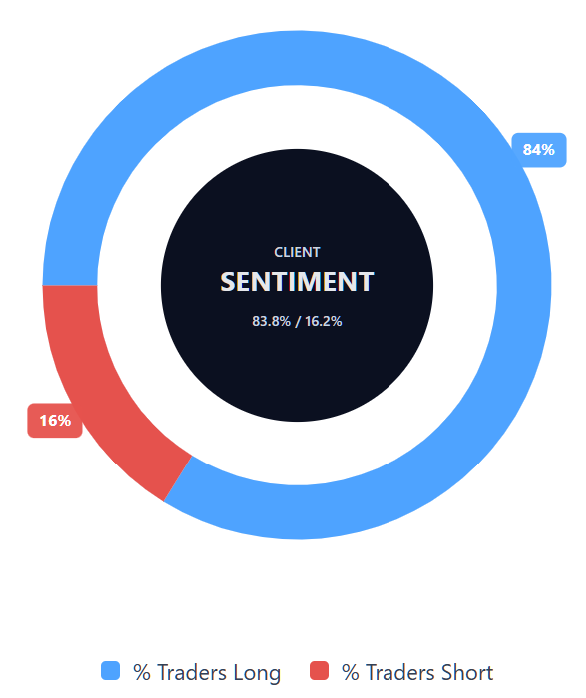

Capital.com’s client sentiment for AMD CFDs

As of 22 June 2026, Capital.com client positioning in AMD CFDs shows 83.8% buyers vs 16.2% sellers, putting buyers ahead by 67.6 percentage points and indicating a strong long bias among open client positions. This snapshot reflects open positions on Capital.com and can change.

Summary – AMD 2026

- As of 1:18pm UTC on 22 June 2026, AMD traded at $544.72, up approximately 154% year to date after rallying from $214.24 at the end of 2024.

- Key drivers include strong AI data centre demand, AMD’s growing server CPU and MI-series GPU market share, and a broader semiconductor sector rally.

- Risks include export control uncertainty around AI chip sales to China, elevated valuation, and the potential for sentiment to reverse sharply if guidance or product updates fall short of market expectations.

- AMD’s ‘Advancing AI 2026’ event on 22–23 July in San Francisco is drawing market attention ahead of the Q2 2026 earnings report, expected around 4 August 2026.

Past performance is not a reliable indicator of future results.

FAQ

Who owns the most AMD stock?

What is the five-year AMD share price forecast?

Is AMD a good stock to buy?

Could AMD stock go up or down?

Should I invest in AMD stock?

Can I trade AMD CFDs on Capital.com?

Yes, you can trade AMD CFDs on Capital.com. Trading share CFDs lets you speculate on price movements without owning the underlying asset and to take long or short positions. However, contracts for difference (CFDs) are traded on margin, and leverage amplifies both profits and losses. You should ensure you understand how CFD trading works, assess your risk tolerance, and recognise that losses can occur quickly.