NVIDIA hits $5 Trillion: What’s driving it and what’s next

NVIDIA has become the first publicly traded company to exceed a $5 trillion market capitalization.

The milestone underscores how NVIDIA has transformed from a niche graphics-chip designer into the backbone of the global artificial-intelligence (AI) infrastructure boom.

NVIDIA weekly chart

Past performance is not a reliable indicator of future results.

What’s fuelled the rise

NVIDIA’s stellar performance has been driven by a combination of factors which include strong earnings performance, demand growth, and a leading position in AI infrastructure at a time when the sector is growing exponentially.

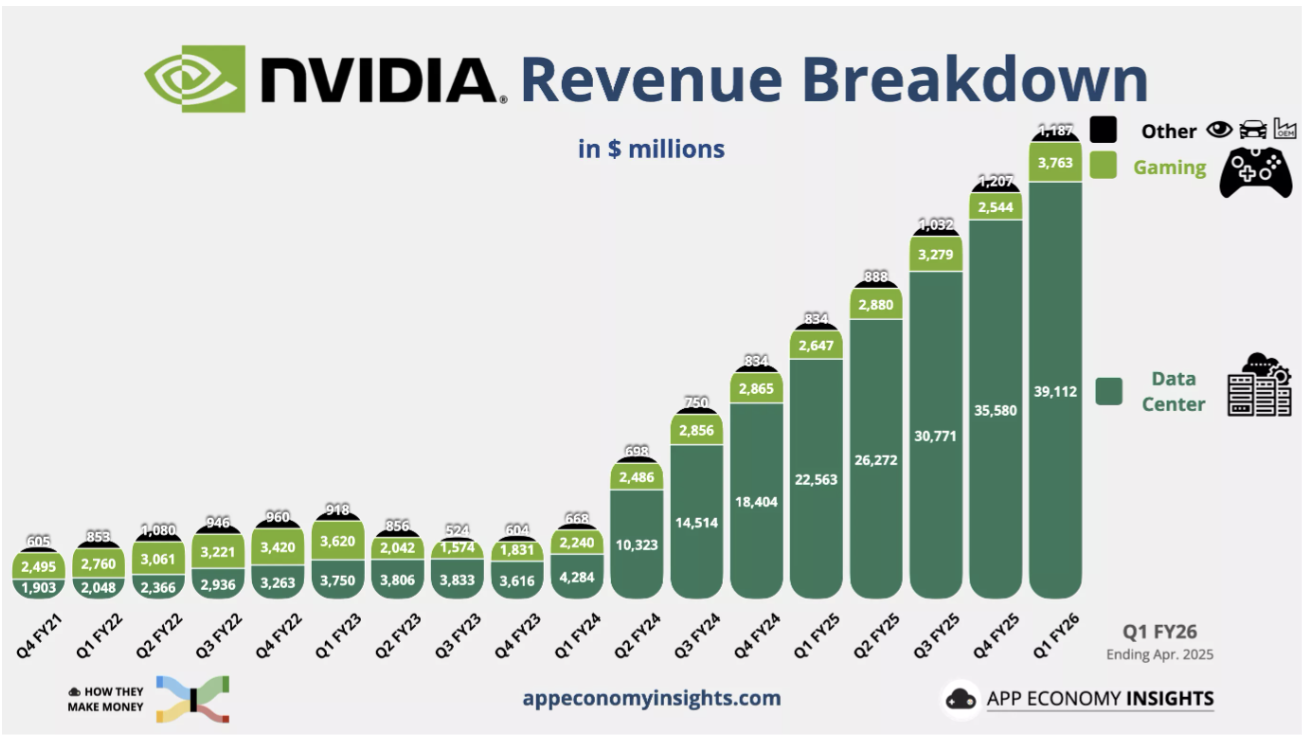

NVIDIA’s leadership in GPUs and AI hardware is at the heart of its valuation. Its Blackwell GPU architecture powers the large-language-model training and inference that underpin tools like ChatGPT. The company disclosed that in its recent quarter, data-centre revenue was $41.1 billion — up 56 % year-over-year, and up 17 % sequentially for Blackwell-related revenues. Revenue came in at $46.7billion, up 56% year-over-year, with net income up 59%. The consistency of qualitative beats in earnings and upgrades in guidance has helped push investor expectations upward.

Past performance is not a reliable indicator of future results.

Furthermore, the company’s growth outlook remains positive as it has announced significant orders for its AI chips and systems. In fact, potential re-entry or expansion into China—once U.S. export controls ease—represents a very large addressable market.

Because NVIDIA is so central to the AI narrative, funds and indexes allocate to it heavily. Its dominance gives the company pricing power and influence over the broader tech index trajectory. That amplifies its valuation relative to peers.

Risks and headwinds

NVIDIA still faces several notable risks despite its historic run. Geopolitical and export-control uncertainties remain a major overhang, as U.S. restrictions on advanced chip exports to China continue to limit access to one of its most important markets. Any escalation in trade tensions or additional regulatory action could blunt future growth prospects. Another concern is concentration risk and inflated expectations — markets are already assuming breakout growth for years to come, meaning any disappointment in quarterly results or guidance could trigger sharp volatility.

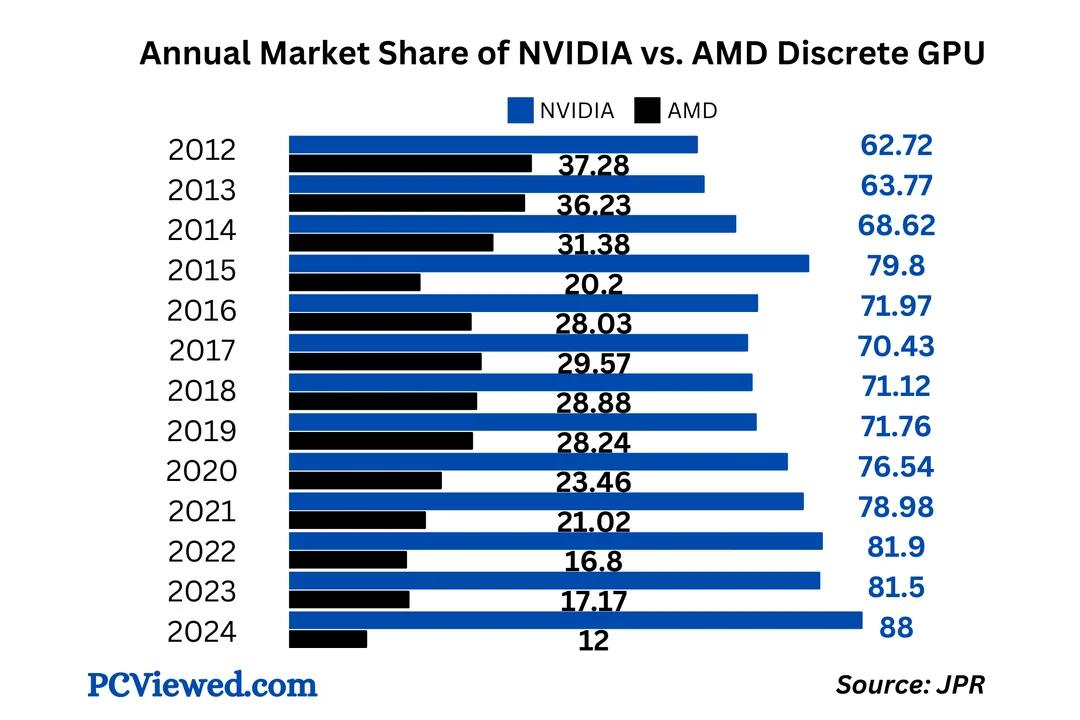

Valuation is another factor under scrutiny, as NVIDIA’s current market price already reflects much of its future potential, leaving little margin for error. Meanwhile, competitive and cyclical risks are rising. Rival chipmakers such as AMD and other system-level players are investing heavily in AI infrastructure, and any slowdown in data-centre demand — whether due to a pause in model training or a shift toward inference workloads — could pressure NVIDIA’s momentum. Collectively, these factors highlight that while NVIDIA’s leadership remains undisputed, sustaining its current growth trajectory will require navigating a far more complex and competitive landscape ahead.

Past performance is not a reliable indicator of future results.

Tailwinds that could sustain the momentum

NVIDIA continues to benefit from powerful structural tailwinds that could sustain its long-term growth story. The global build-out of AI infrastructure still has many years to run. As demand for advanced compute power accelerates, NVIDIA is well-positioned to capture a significant share of this investment.

New product cycles, including the rollout of its Blackwell architecture and future generations, will likely extend this momentum. As models grow larger and computing requirements intensify, the company stands to gain from the transition away from older hardware. Geographic expansion and deeper ecosystem integration also provide additional support — particularly as access to China potentially improves and NVIDIA’s dominance across software, hardware, and services strengthens its competitive moat.

Finally, NVIDIA’s influence within global equity indices has created a feedback loop that reinforces its market leadership. Strong earnings results tend to attract further inflows from institutional and passive investors, which in turn lift valuations and fuel continued momentum. Collectively, these dynamics suggest that while NVIDIA’s growth may eventually moderate, its structural advantages and strategic position in the AI economy could continue to give it an edge. However, rising competition in the sector could also reshape the landscape.

Is it Sustainable?

It increasingly depends on execution and the macro backdrop aligning. NVIDIA’s leadership position gives it a unique runway. However, the margin for error is much smaller. In prior years, strong growth alone was enough to impress. Going forward, growth must be very strong, and guidance must stay aggressive. Any sign of deceleration—or a major regulatory/geopolitical reversal—could pose a sharp re-rating.