Market Analysis: Europe feels the pinch of Trump’s tariffs and higher CPI

European stocks face downside pressure as Trump’s tariff threats weigh on investor sentiment.

Markets are bracing for another volatile week as Trump's tariff policies take centre stage. The confirmation of 25% tariffs on Mexico and Canada over the weekend caught markets somewhat off guard, despite Trump's prior hints. The lack of a clear economic rationale behind this decision—justified primarily as a measure to curb illegal immigration and fentanyl imports—has unsettled investors, leading to a risk-off sentiment at the start of the week.

The initial market reaction has favoured safe-haven assets, with the US dollar, Japanese yen, and gold gaining momentum this morning. Equities, on the other hand, are struggling. Tariffs weigh on corporate earnings by squeezing profit margins and slowing future growth. They also impact valuations by reducing the likelihood of a Federal Reserve rate cut. As a result, major US equity futures opened lower during the Asian session. This decline comes at a time when equities were already considered overextended and expensive, with confidence still shaken from last week’s DeepSeek meltdown. The introduction of tariffs has further dampened the outlook for equities.

US 100 daily chart

Past performance is not a reliable indicator of future results.

The ramifications of this tariff announcement extend beyond North America. Trump has also threatened tariffs against Europe, though the market reaction across the Atlantic has been more subdued. The FTSE 100 was the worst performer in early trading, opening lower but recovering some ground.

In Mainland Europe the STOXX 600 has dropped to 530 this morning as concerns over potential European tariffs weighed on investor sentiment. The move erased last week’s gains following the DeepSeek scare. However, momentum remains firmly on the upside as the index holds above 525. A dip below this level could call the bullish drive into question, as resistance may emerge once again. The pullback has also allowed the RSI to retreat into neutral territory after surpassing the overbought threshold, which could generate renewed buying interest in the coming days.

STOXX 600 daily chart

Past performance is not a reliable indicator of future results.

ECB Policy and Inflation Concerns

A key differentiator for European stocks compared to their US and UK counterparts is the European Central Bank's (ECB) proactive approach to monetary policy. The prospect of additional rate cuts this year improves the valuations of European companies, which are already relatively cheap on a price-to-earnings basis. A dovish ECB is likely to continue supporting European equities, as the central bank aims to mitigate the negative effects of restrictive policies on economic growth. However, inflation remains a pressing concern.

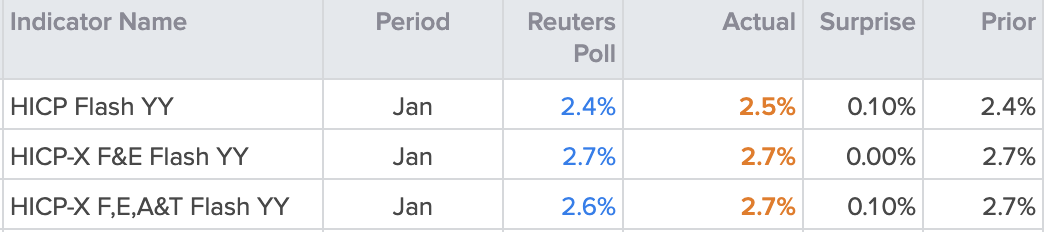

The flash CPI reading for January, released this morning, showed headline inflation rising unexpectedly once again. This development has likely exacerbated bearish sentiment in European stocks. Markets continue to price in an almost certain chance that the ECB will cut rates at its next meeting in March. However, if inflation continues to trend higher, the central bank’s flexibility may become increasingly limited.

Eurozone CPI January flash readings

Source: refinitiv

Outlook and Key Considerations

With tariffs, inflation, and central bank policies all shaping market sentiment, European stocks are facing a delicate balance. While monetary easing from the ECB could provide some relief, persistent inflation and geopolitical uncertainty remain key risks. Investors will be closely watching upcoming economic data and central bank decisions for further clarity on the market’s direction.