FOMC Preview: Fed to Hold as Trade Tensions Undermine Growth Outlook

FOMC Preview May 2025

The US Federal Reserve is widely expected to hold interest rates steady at this week’s policy meeting as the central bank grapples with a deteriorating growth outlook, persistent inflationary risks, and mounting political pressure. Financial markets are now leaning towards a “dovish hold”, with traders betting that a rate-cutting cycle will recommence later in the year—though the precise timing remains uncertain.

US economy slows as trade policy weakens growth

Recent US economic data paints a picture of a slowing economy. The advanced estimate of Q1 2025 GDP growth came in below expectations at -0.3%, down sharply from 2.4% in the previous quarter. Much of the slowdown was attributed to a spike in imports as businesses front ran looming tariffs. However, there were signs of softer consumer activity, too.

The March PCE Price Index, the Fed’s preferred inflation gauge, showed signs of moderation, with headline PCE flat month-on-month, down from 0.4% in February. On a year-over-year basis, the index slowed to 2.3%, while the Core PCE deflator eased to 2.6% from 2.8%—moving gradually towards the Fed’s 2% target and keeping the door open for future interest rate cuts.

Labour market data has also begun to soften, although the April payrolls surprised to the upside. The latest Non-Farm Payrolls report showed employment increased by 177,000, exceeding the 130,000 estimate but extending a downward trend. The unemployment rate held steady at 4.2%, but the drop in job creation suggests that momentum is fading. Wage growth remained subdued, indicating that inflationary pressures from the labour market are moderate.

Trade-uncertainty complicates Fed rate outlook

The economic backdrop is being complicated by renewed uncertainty over trade policy. President Donald Trump has escalated tensions with key trading partners, increasing tariffs on imports under the so-called “Liberation Day” framework. Proposals under consideration include levies as high as 145% on Chinese goods. Other tariffs announced on “Liberation Day” have been paused for other trading partners and negotiations are reportedly underway to strike new trade deals. However, uncertainty persists, with business and consumer surveys showing weaker activity and confidence as a result.

For the Fed, this presents a classic policy dilemma: respond to potential inflationary shocks with tighter policy, or support growth by looking through temporary price pressures. With the outlook clouded by trade-related volatility, the Fed’s reaction function remains difficult to pin down and a critical focus of market participants at this meeting.

FOMC expected to keep policy unchanged

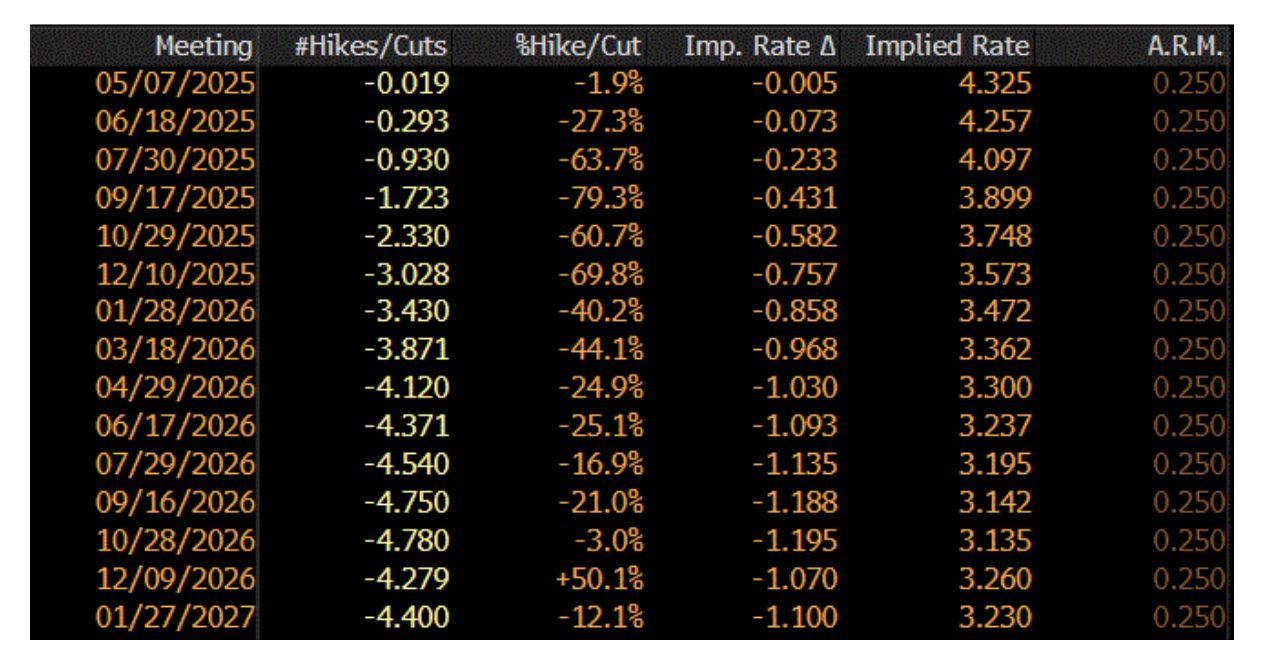

Markets overwhelmingly expect the Fed to hold the Federal Funds Rate at 4.25%-4.50% this week. According to pricing in Fed Funds Futures (as of May 6), the probability of a cut at the May meeting is effectively zero. Traders are assigning roughly a 27% chance of a rate cut by the June meeting and are fully pricing in the first cut by September.

As shown in the chart below, the implied path of the Fed Funds Rate points to nearly 100 basis points of cuts by mid-2026, with the implied rate falling below 3.3% by late next year. However, with recent inflation data proving sticky and risks of tariff-induced price shocks mounting, the Fed is likely to remain cautious in the near term.

In essence, the FOMC is expected to adopt a "wait and see" approach, keeping policy unchanged while assessing the evolving balance of risks.

(Source: Bloomberg)

The markets look for guidance and a clear reaction function

Given that the Fed is unlikely to adjust policy this week, attention will turn to Chair Jerome Powell’s press conference and the accompanying statement. Traders will be looking for signs of how the Fed might respond to the dual threats of slowing growth and renewed inflationary pressures.

Specifically, markets want clarity on whether the Fed is prepared to "look through" transitory inflation resulting from tariffs if the broader economy continues to weaken. Alternatively, any indication that policymakers are willing to delay or pare back cuts in the face of headline inflation could disappoint investors and roil financial markets.

Powell’s communication challenge will be to maintain flexibility without sowing confusion, a balancing act that has become more difficult in a politically charged environment.

The political pressure piles up on Powell and the Fed

President Trump has once again ramped up public criticism of the Federal Reserve, accusing the central bank of “crippling American industry” and “refusing to support US jobs”. In recent weeks, the President has even threatened to replace Jerome Powell—a threat that carries limited legal weight but nonetheless underscores the pressure facing the Fed.

The likely decision to keep policy unchanged at this meeting will likely result in significant backlash from US President Trump who is looking for support for the economy and possibly a scape goat to blame the trade induced slow down on.

Markets positioned for a dovish Fed

Despite the recent inflation risks, rates markets remain positioned for a dovish Fed. Equities have rebounded from their April lows in part on expectations that rate cuts remain on the horizon and the Fed will act to support the economy if data continues to weaken.

However, if the Fed delivers a message that appears too cautious or implies that cuts may be delayed beyond current expectations, it could trigger a reassessment of market pricing. That may lead to a stronger US Dollar and downward pressure on risk assets, particularly in rate-sensitive sectors like tech. Conversely, any indication that the Fed is actively preparing to ease—should growth risks intensify—could support equities and risk appetite more broadly.

Heading into the Fed’s decision, the NASDAQ (and S&P 500) sit just below their critical 200-day MAs, of which a break or failure to break may determine the short-term direction for Wall Street.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)