Non-performing loan definition: understanding their impact on financial stability

")

You know how garden weeds drain moisture and nutrients from the soil, choking your healthy plants and leaving none for crops? Non-performing loans (NPLs) act the same way in a bank’s balance sheet. They soak up capital, yield no returns, and can even suffocate healthier lending opportunities. Understanding what a non-performing loan is – and how it can ripple through banks and entire economies—gives you a stronger lens for interpreting non-performing loan news, especially when considering investments in the banking sector.

A non-performing loan is a loan for which interest or principal payments remain overdue, typically for 90 days or more. Because it no longer generates income, the loan ‘performs’ no more — it becomes a liability rather than an asset.

Staying abreast of non-performing loan news is important especially if you’re trading shares of the banking sector.

What is a non-performing loan?

An NPL is a debt you failed to pay back. This may mean that both the principal and interest remain unpaid. The loan is ‘non-performing’ because it is not earning money for the bank. It has stopped yielding returns.

The total amount of NPLs in a bank or an economy is called the NPL ratio. A high NPL ratio is a sign of financial distress. It suggests that many borrowers are struggling.

How do banks classify loans as non-performing?

Banks follow strict rules to classify loans. These rules come from regulators and industry standards. The main criterion is an extended period without payment.

It also applies if the borrower is unlikely to repay the loan in full. The time limit ensures that banks across different countries use the same standards.

If you miss a single payment, the loan is delinquent. It is not yet non-performing. Banks also look at other factors, such as your financial health. Even if a payment is not missed, the loan can be classified as non-performing. This happens if the bank is convinced that you cannot repay the debt. For instance, if you file for bankruptcy, the loan is immediately an NPL. The bank no longer expects to receive payments.

The classification process is vital for banks. It helps them manage risk. They must set aside capital to cover potential losses from NPLs. This is called provisioning. It protects the bank from a sudden hit to its finances. It also gives a true picture of the bank's financial health.

What happens when a loan becomes non-performing?

An NPL affects both the borrower and the bank.

An NPL or even a missed payment would lower your credit score. An NPL classification causes a major drop. This can make getting any new loans harder. It also impacts your future credit applications, like for a mortgage or a car loan. In a worst-case scenario, you may face legal action from the bank. The bank may seize the assets you used as collateral for the loan.

For the bank, NPLs cause a direct financial loss. They reduce the bank's profitability. The bank must use its own funds to cover the loss. This can lead to a shortage of capital. A high number of NPLs can hurt a bank's reputation. It can make investors and depositors lose confidence in the bank’s due diligence.

The bank may also have to divert resources to deal with bad debt or reassess its creditworthiness assessment criteria. This slows down the bank's ability to lend new money.

The impact of non-performing loans on financial markets

Apart from the definition of non-performing loans, it’s important to learn their impact. A large volume of NPLs can be a sign of a troubled economy. It can also be a cause of a crisis. When many borrowers cannot repay their loans, banks suffer. They become hesitant to lend new money. This is called a credit crunch. Businesses and people cannot get new loans. This slows down economic activity. Companies may fail, and unemployment may rise.

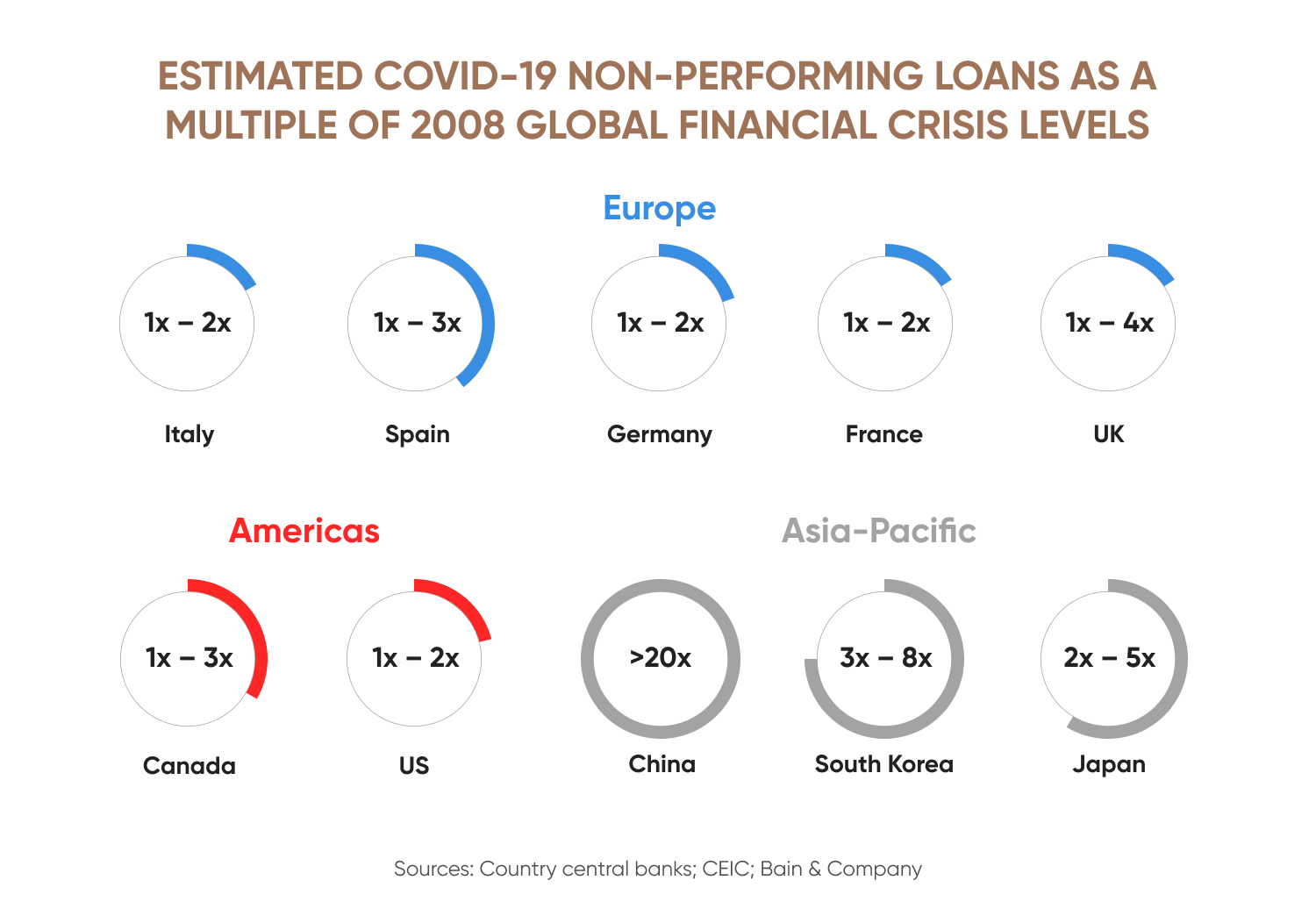

If left unaddressed, a high NPL ratio can cause a banking crisis. The covid-19 pandemic took a toll on the health of millions, and several businesses shut down. Post the pandemic, most banks had about 10% of NPLs. In fact, a Bain and Company report found that most regions would have more NPLs than they did in 2008, during the global financial crisis.

The 2008 crisis had already shown how interconnected the financial markets are. A problem in 1 area can quickly spread. Non-performing loan news from 1 sector led to a worldwide economic collapse. Such situations call for strategic NPL management. Banks worldwide issued moratoriums, allowing borrowers to not repay loans for a while.

Wondering whether you could have navigated the pandemic? Open a demo account and backtest your trading strategy.

Strategies banks use to manage and reduce NPLs

Banks use various strategies to manage and reduce their NPLs. The goal is to recover as much of the loan as possible. This also helps to improve the bank's financial health.

Restructuring

The bank may discuss with you and agree on new terms. This can include a longer repayment period. It might also involve a lower interest rate. This makes it easier for you to start paying again. It helps the bank avoid a total loss.

Asset sales

The bank sells the NPL to a third party. This buyer is often a debt collection company. The bank sells the loan at a discount. The buyer then tries to collect the debt. This allows the bank to quickly get some cash back.

Provisioning

Banks usually set aside funds to cover potential losses. This is a buffer against a rise in NPLs. It helps to absorb the financial shock. The amount of provisioning is often regulated by central banks. For instance, banks across the US and EU increased their credit provisions in early 2025, after the Trump administration announced high tariffs.

Banking regulations on non-performing loans

Global and national regulators have strict rules for NPLs. These rules are designed to prevent financial crises. The Basel Committee on Banking Supervision (BCBS) sets global standards for bank capital. Basel III rules require banks to hold more capital to prepare for potential losses from NPLs. In addition, regional central banks set rules for lenders in their country.

The European Central Bank (ECB) also has strict NPL guidelines. The ECB sets a target for NPL ratios. It also requires banks to have clear plans for dealing with NPLs. This ensures banks are well-prepared.

The US Federal Reserve also supervises banks and conducts stress tests. These tests check if banks can handle a rise in NPLs. These regulations ensure banks are financially sound and protect the global financial system. The rules promote good governance and risk management. This makes the entire system more resilient, helping to prevent a repeat of past financial crises.

Wish to trade stocks of banks that have a high health score? Open a live account to get started.

FAQs

What is a non-performing loan, and why is it important?

A non-performing loan is a debt where the borrower has not made payments for at least 90 days. It is important because a high volume of NPLs can threaten a bank's stability and the entire financial system.

How do banks classify loans as non-performing?

Banks classify a loan as non-performing based on the period of missed payments. The standard is usually 90 days. The bank also considers the borrower's ability to repay the loan in the future.

What happens when a loan becomes non-performing?

For the borrower, their credit score is severely damaged, and they may face legal action. For the bank, it results in a financial loss. The bank must set aside funds to cover the loss. This hurts its profitability and stability.

How do non-performing loans affect banks and financial stability?

NPLs hurt a bank's finances. They reduce profits and capital. A high number of NPLs can cause a credit crunch. This can slow down the economy. A widespread problem can lead to a financial crisis.

How can banks reduce their NPL ratios?

Banks can reduce NPLs through loan restructuring. This involves changing the loan terms. They can also sell the debt to third parties. Strong risk management and early intervention are key.