September US Non-Farm Payrolls Preview

Kyle Rodda, Senior Market Analyst at Capital.com, previews the US Non-Farm Payrolls report for September. The article discusses market expectations of a stable labor market with 150,000 new jobs, an unchanged unemployment rate of 4.2%, and steady annual wage growth at 3.8%. It also highlights potential rate cuts by the Federal Reserve, revisions to past payroll data, and the reaction of various markets such as the US Dollar, S&P 500, and gold.

Economists expect a stable labour market in September

Market economists expect that the US labour market remained in a steady position in September. Forecasters project that the US economy added 150,000 jobs for the month, greater than the 142,000 in August, with the unemployment rate holding steady at 4.2%. While less of a concern owing to softening inflation and a rising unemployment rate, annual wage growth is expected to remain unchanged at 3.8%.

Potential revisions of previous month’s data will be closely monitored by the markets. Recent Non-Farm Payrolls reports have come with downgrades to employment change figures, stoking fears about a weaker US labour market than previously thought. An historically high annual revision from the Bureau of Labor Statistics in August was another catalyst for the markets pricing in aggressive Fed rate cuts going forward, amidst expectations of a steep drop in hiring activity in the US.

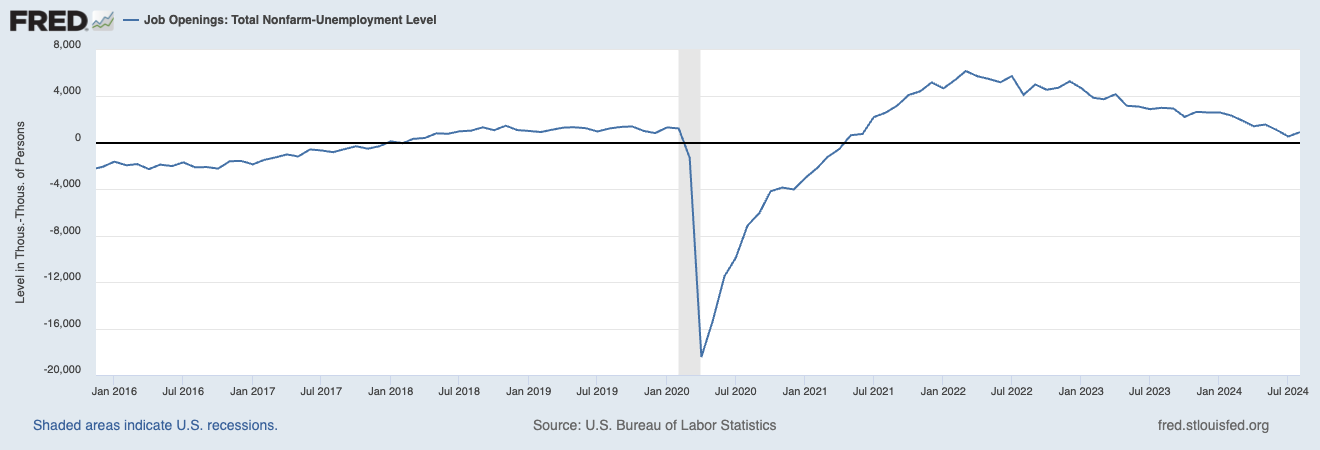

Despite these fears, the official Non-Farm Payrolls data doesn’t show a US labour market falling off the proverbial cliff. In addition, recent unemployment claims data has revealed a drop in applications for jobless benefits, countering the notion of a weakening US economy. This week’s monthly JOLT’s Job Openings data also revealed a surprise jump in job vacancies, signalling some lasting tightness in the labour market.

Source: St Louis Fed

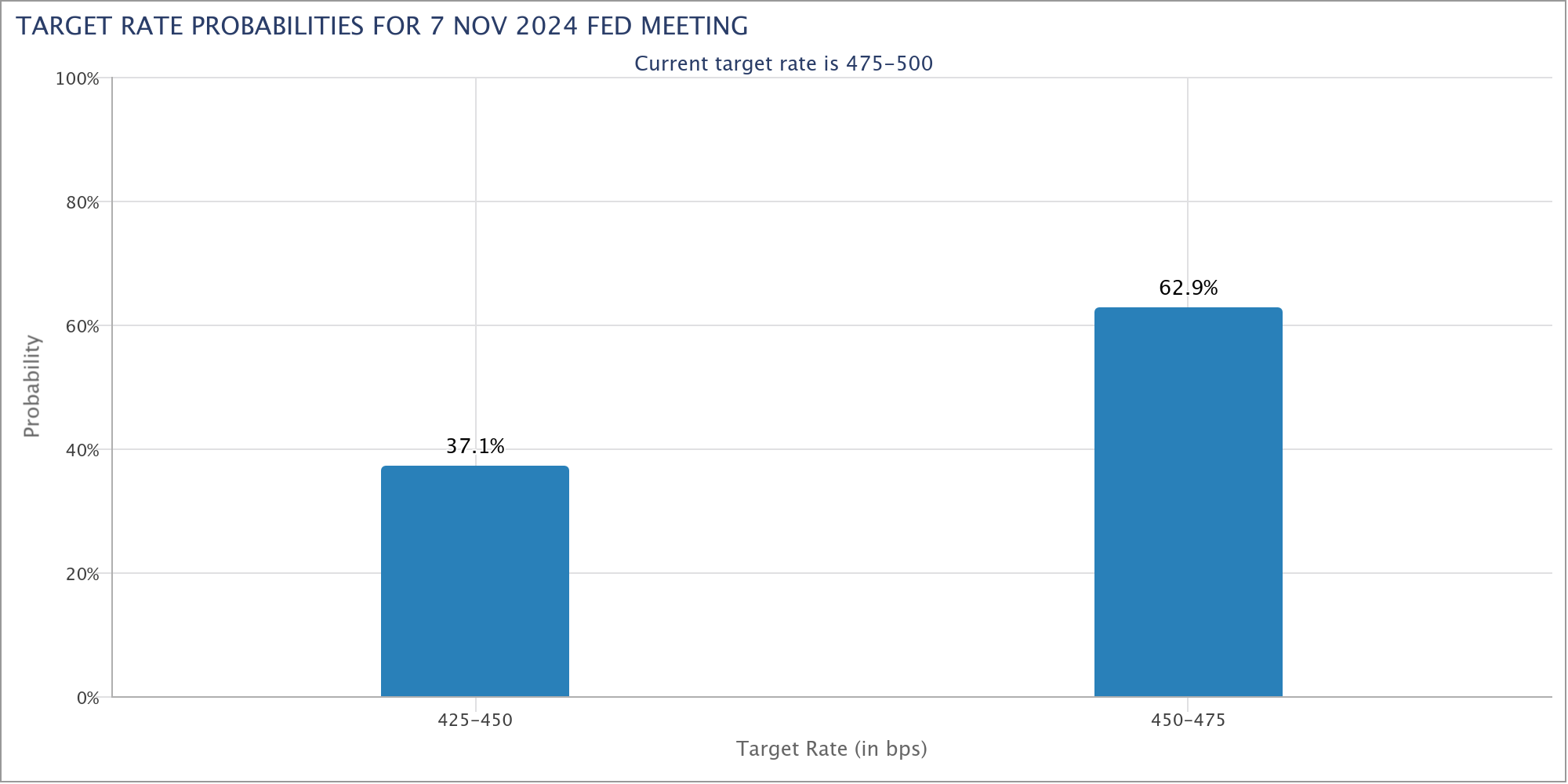

Rates markets split on size of November rate cut

Federal Funds Futures point to a high probability that the Fed cuts rates by a further 75 basis points before the end of the year. Leading into the Non-Farm Payrolls release, the futures curve is fully discounting 70 points of cuts – 5 points shy of reflecting three standard 25 basis points of reductions by the December meeting. Essentially, the markets imply that the Fed will cut rates by 50 points at one of the Fed’s remaining two meetings of the year, with the curve currently implying a 37.1% chance it happens in November.

Source: CME Group

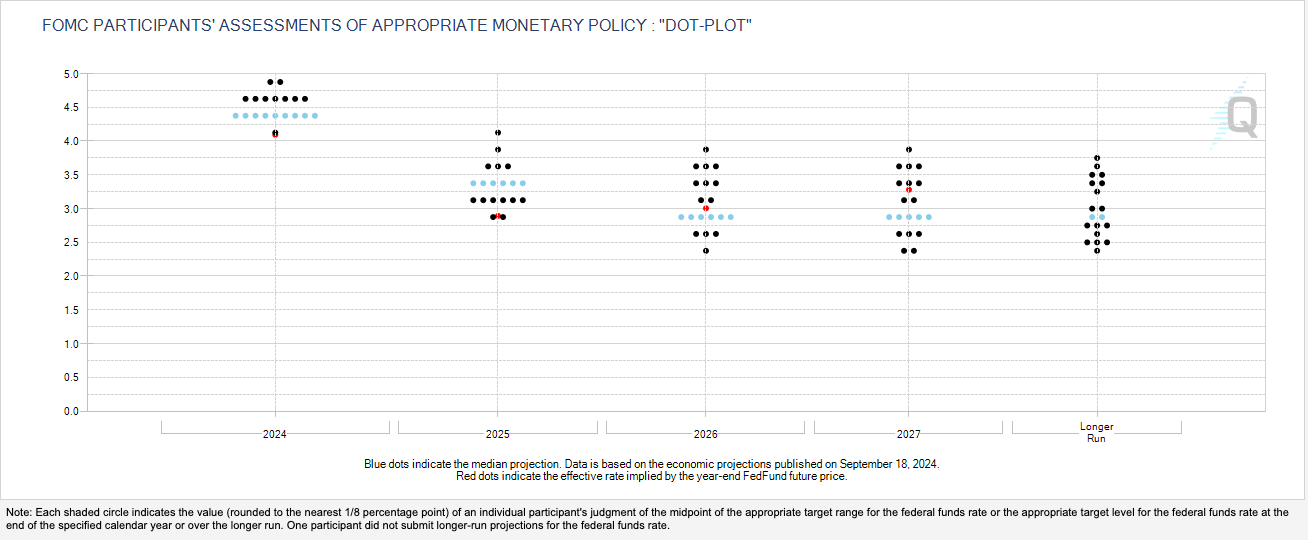

Despite the US Federal Reserve’s “dovish pivot” at its September meeting, which included a drastic downward revision in the central bank’s so-called “dot-plots”, market pricing remains ahead of the Fed in discounting the number of rate cuts likely to occur this cycle. The dot plots implied the Federal Funds Rate is likely to end this year at 4.25% - 4.50%, while the markets are baking-in a range of 4.00% - 4.25%. Meanwhile, the dot plots suggest rates will end 2025 in the mid-3% range, while the markets expect it in the high 2% range.

Source: CME Group

How could the markets react to the NFP data?

The markets remain concerned about the strength of the US labour market. Given current pricing, this Non-Farm Payrolls release represents two-way volatility risk. If the data signals resilient labour demand, it could water down expectations of a 50 basis point cut from the Fed in November. If it is particularly strong, then the nearly 75 basis points worth of cuts, representing the equivalent of three 25 point point rate cuts, baked into the futures curve before the end of the year, could be reduced materially. Conversely, an upside surprise in the unemployment rate, similar to what was seen in July, could lead the markets to price-in a higher chance of a 50 point cut in November and open the prospect of two 50-point moves in the final two Fed meetings of the year.

The US Dollar has firmed heading into the September Non-Farm Payrolls release. The Greenback has been battling crosswinds including resilient economic data, expectations of ECB rate cuts, a mixed outlook for Japanese monetary policy, and the recovery in China’s growth expectations. The EUR/USD has broken an ascending wedge pattern and retested support at approximately 1.1050, having failed to break resistance at 1.1200.

Source: Trading View

Past performance is not a reliable indicator of future results

While the benchmark S&P 500 has hit record highs following the Powell-pivot, the NASDAQ has failed to hit the milestone, with the shift in the policy cycle driving a rotation from growth stocks into economically sensitive cyclicals. The index managed to break out of a consolidation pattern as it looks to continue its primary uptrend. A critical confluence of support levels appears around 19,200, with the most recent high around 20,260 a potential short-term resistance level.

Source: Trading View

Past performance is not a reliable indicator of future results

Several factors continue to support gold, including geopolitical tensions in the Middle East. However, the biggest driver of the yellow metal’s uptrend is the weaker Dollar and lower yields derived from expectations of aggressive US rate cuts going forward. The charts remain bullish for Gold, which is in a clear pattern of higher-highs and lower-lows; price action is currently carving out a continuation pattern, with resistance around a downward sloping trendline and support at roughly $US2625.

Source: Trading View

Past performance is not a reliable indicator of future results