Gold breaks below $4,000 as Warsh's Fed rewrites the narrative

Gold has fallen below the psychologically important $4,000 level for the first time in seven months, extending its correction as investors increasingly embrace a stronger dollar and a higher-for-longer interest-rate outlook.

The selloff marks a significant shift in sentiment for an asset that spent much of the past two years supported by geopolitical uncertainty, central-bank buying and expectations of easier monetary policy. Instead, the dominant narrative has become one of renewed dollar strength and a Federal Reserve determined to restore price stability.

Gold (XAU/USD) daily chart

Past performance is not a reliable indicator of future results.

The Warsh Fed era reinforces the focus inflation

The catalyst has been Kevin Warsh's first meeting as Federal Reserve Chair. His reputation as an inflation hawk had already raised doubts over whether the Fed would continue the easing path many investors had anticipated earlier this year. Any lingering belief that policymakers might look through renewed inflation pressures was largely dispelled during his maiden press conference, where Warsh repeatedly emphasised price stability and deliberately avoided offering dovish forward guidance. Treasury yields moved higher, the dollar climbed to 13-month highs and gold, which offers no yield, came under renewed pressure.

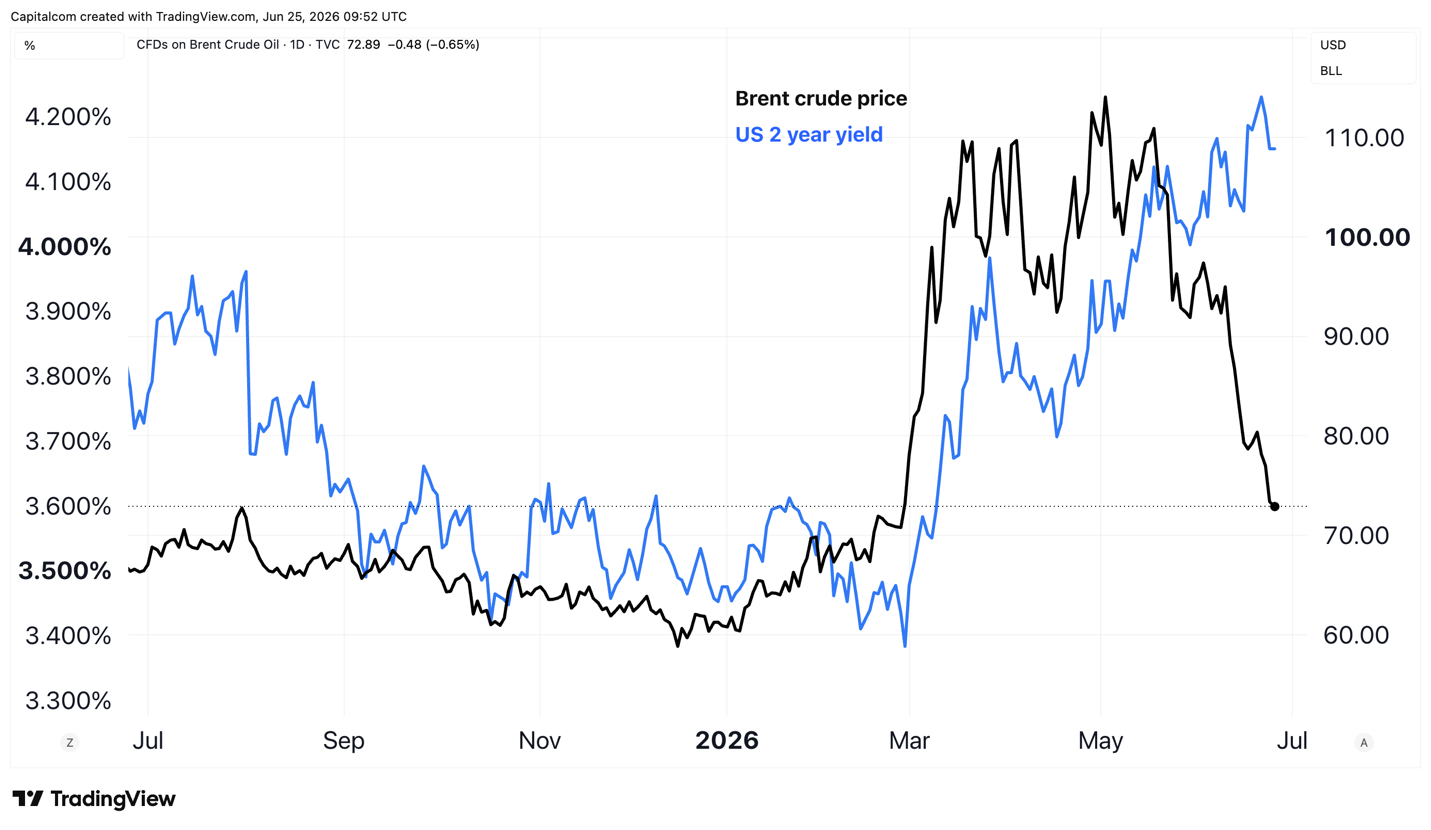

Yet the story is more nuanced than simply "hawkish Fed equals weaker gold." The geopolitical backdrop has changed dramatically. The ceasefire agreement between the US and Iran and the reopening of the Strait of Hormuz have triggered a sharp decline in oil prices, removing one of the most immediate upside risks to inflation. Under normal circumstances, that would be expected to give the Fed greater flexibility to ease policy over time. If Warsh ultimately wants room to lower rates, the collapse in the energy risk premium arguably moves the economy closer to that objective.

Economic data supports a higher-for-longer stance

The complication is that inflation is not an energy story alone. Strong April CPI data, resilient May non-farm payrolls and elevated underlying inflation measures all point to price pressures that are becoming more deeply embedded in the economy. The AI investment boom, continued fiscal support and robust consumer demand have created inflationary forces that extend well beyond oil prices. In other words, while the energy shock may be fading, the broader inflation challenge remains concerning.

US 2-year yields and Brent Crude daily chart

Past performance is not a reliable indicator of future results.

That creates an unusual macroeconomic setup. Lower oil prices would normally be viewed as disinflationary. However, they also reduce costs for households and businesses, effectively acting as a tax cut that boosts disposable income and demand. If the economy is already operating close to capacity, stronger demand could itself become inflationary. That is the counterintuitive scenario markets are increasingly beginning to price: reopening the Strait of Hormuz may ultimately support growth enough to keep inflation elevated, forcing the Fed to maintain a restrictive stance or even tighten policy further.

This shifting narrative helps explain why the dollar has continued to strengthen despite the easing of geopolitical tensions. Rather than focusing solely on lower oil prices, investors are looking at the broader macro picture and concluding that the Fed still has work to do. The market is increasingly pricing a meaningful probability of a rate hike before year-end, widening yield differentials in favour of the dollar and weighing on precious metals.

$4000 is a significant phycological level

Technically, the break below $4,000 is significant. Gold has now fallen beneath all of its major moving averages, confirming the loss of momentum that has been building since February. The move also represents a break of an important psychological support level, opening the door to further consolidation if yields remain elevated. While the longer-term structural drivers, including robust central-bank demand and concerns over sovereign debt and currency debasement, remain intact, they are currently being overshadowed by the opportunity cost of holding a non-yielding asset. However, the structural forces have not disappeared simply because the Fed has adopted a firmer stance. Instead, they appear to have taken a back seat while markets reassess the trajectory of US monetary policy.

For now, the balance of risks has shifted decisively in favour of the dollar. Whether that continues will depend less on oil prices and more on whether the underlying inflation story begins to soften. If it does, the Fed may eventually gain the flexibility to ease policy without sacrificing credibility. If it does not, gold could remain under pressure for longer as investors continue to favour higher-yielding dollar assets.