Important information

Regulations

Licenses

Capital Com SV Investments Limited is a regulated Cyprus Investment Firm, with registration number HE 354252, authorised and regulated by the Cyprus Securities and Exchange Commission (CySEC) under the license number 319/17 (brand name “Capital.com”).

Capital Com Group Ltd is a regulated Cyprus Investment Firm, with registration number HE 446198, authorised and regulated by the CySEC under the license number 463/25 (brand name “Capital.com”).

Based in the European Union, Capital.com complies with the requirements imposed by the Markets in Financial Instruments Directive (MiFID).

Segregated Funds

Capital.com keeps its clients’ money in segregated bank accounts in accordance with our regulator’s rules on client money. In other words, your funds are held separately from our funds and are thus not exposed to any unexpected financial difficulties that may arise in the Company. The Company does not claim any entitlement to these funds, as they belong to you.

Clients’ funds are spread across a number of prominent banks that are constantly reviewed to ensure they are in line with the Capital.com policies.

Investor Compensation warranties

Capital.com segregates all retail client funds from its own money in accordance with relevant regulations. Capital Com SV Investments Limited and Capital Com Group Ltd are members of the Investor Compensation Fund (the “ICF”), which provide compensation for Retail Investors should Capital.com declare default. For further details please refer to the Investor Compensation Fund Policy.

Fixing the amount of payable compensation

The amount of the compensation payable to each client is calculated in accordance with the legal and contractual terms governing our relationship with the client, subject to the set-off rules applied for the calculation of the claims between the client and Capital.com.

Key Documentation

Capital Com SV Investments Limited

- Terms and Conditions

- Terms and Conditions for share dealing services

- Risk Disclosure Statement

- Order Execution Policy

- Privacy Policy

- Client Categorisation Policy

- Investor Compensation Fund Policy

- Conflicts of Interest Policy

- Cookies Policy

- Leverage and Margin Policy

- Elective Professional Clients Terms and Conditions

- List of PSPs/EMIs

Capital Com Group Ltd

- Terms and Conditions

- Terms and Conditions for share dealing services

- Risk Disclosure Statement

- Order Execution Policy

- Privacy Policy

- Client Categorisation Policy

- Investor Compensation Fund Policy

- Conflicts of Interest Policy

- Cookies Policy

- Leverage and Margin Policy

- Ex Ante Cost and Charges Disclaimer (CFDs KOs)

- Ex Ante Cost and Charges Disclaimer (Stocks)

- List of PSPs/EMIs

- Key Information Documents (all languages)

Regulatory Publications (Capital Com SV Investments Limited)

Pillar 3 Disclosure - Standalone (2022)

Pillar 3 Disclosure - Consolidated (2022)

Pillar 3 Disclosure - Standalone (2023)

Pillar 3 Disclosure - Consolidated (2023)

Pillar 3 Disclosure - Standalone (2024)

Pillar 3 Disclosure - Consolidated (2024)

RTS 27 Quality of Execution Disclosure (Q3 2023)

RTS 27 Quality of Execution Disclosure (Q1 2024)

RTS 27 Quality of Execution Disclosure (Q2 2024)

RTS 27 Quality of Execution Disclosure (Q3 2024)

RTS 27 Quality of Execution Disclosure (Q4 2024)

RTS 28 Quality of Execution Disclosure (2022)

RTS 28 Quality of Execution Disclosure (2023)

RTS 28 Quality of Execution Disclosure (2024)

Key Information Document - CFDs on Indices

Key Information Document - KOs on Indices

Key Information Document - CFDs on Cryptos

Key Information Document - KOs on Cryptos

Key Information Document - CFDs on Commodities

Key Information Document - KOs on Commodities

Key Information Document - CFDs on Forex

Key Information Document - KOs on Forex

Key Information Document - CFDs on Shares

Key Information Document - KOs on Shares

Key Information Document - CFDs on Bonds

Key Information Document - KOs on Bonds

Key Information Document - CFDs on Interest Rates

Key Information Document - KOs on Interest Rates

Complaints Procedure

Complaints Procedure (Capital Com SV Investments Limited)

Whilst we always endeavour to offer the best possible service to you, we recognise that you may on occasion feel dissatisfied with an aspect of our service. In the event you are dissatisfied about a financial product or service provided to you by Capital Com SV Investments Limited (the Company), please raise your concerns to us according to the following procedure.

1. In the first instance, contact our Customer Support team by email to the email address support@capital.com or by telephone on +357 25024950. Most concerns can be resolved at this level. When contacting our Customer Support team, please provide as much information as possible, including:

- your full name and account number;

- a clear description of the issue(s); and

- references to any additional relevant documentation, screenshots, etc.

Our Customer Support team will then endeavour to resolve your concerns as quickly as possible and propose a resolution to your case. If, after the resolution is provided, we do not receive any response from you regarding your interest in further escalating the matter, we will regard your concerns to be successfully resolved.

2. If you will remain dissatisfied after the resolution is offered you may contact us at complaint@capital.com or fill the complaint form that can be found below to submit your complaint to our Complaints Department who will be responsible to examine your complaint competently, diligently and impartially to assess whether the Firm has acted fairly, within its rights and have met the Firm’s contractual obligations.

Please ensure that you have informed us of all the relevant facts and evidence to conduct a thorough and independent investigation into your complaint.

At this stage in order to resolve your complaint we will take the following steps:

(i) We will confirm, within five (5) days, receipt of your complaint and provide you with your Unique Reference Number. You should use said reference number in all future communication with us and/or the Financial Ombudsman of Cyprus regarding your complaint.

(ii) After thorough investigation, we will reply to your complaint within two (2) months, informing you about the outcome of our investigation. In our response we will review the relevant facts, findings and conclusions of our investigation and state whether your complaint has been upheld or rejected and, where appropriate, will offer redress and/or remedial action. If your complaint is rejected, we will explain the reasons for this.

In the event that we are unable to respond within two (2) months, due to the complexity of the complaint, we will inform you of the reasons for the delay and indicate the period of time within which it is possible to complete our investigation. This period of time shall not exceed three (3) months from the date of submission of the complaint.

-

In the event that our final response does not fully satisfy you, you may refer your complaint to the Financial Ombudsman of Cyprus. The Financial Ombudsman is an independent service for settling disputes for Cyprus Investment Firms and their clients.

It is important to contact the Financial Ombudsman using your Unique Reference Number within four months of receiving a final response from us otherwise the Financial Ombudsman may not be able to deal with your complaint. Please also note that the Financial Ombudsman will not consider a complaint until the Company has had the opportunity to address it.

The contact details of the Financial Ombudsman are the following:

Website: http://www.financialombudsman.gov.cy

Email: complaints@financialombudsman.gov.cy

Postal Address: P.O. Box: 2535, 1311 Nicosia, Cyprus

Telephone: +35722848900

Fax: +35722660584, +35722660118

Complaints Procedure (Capital Com Group Ltd)

At Capital Com Group Ltd (the “Company” or “we”), we are committed to delivering the highest standard of services to all our clients. However, we understand that you may, on occasion, feel dissatisfied with an aspect of our products or services. In the event, please raise your concerns to us according to the following procedure.

1. In the first instance, please contact our Customer Support team, who will make every effort to resolve your concerns promptly.

Contact details:

- Email address: support@capital.com

- Telephone: +357 25024950

Most concerns can be resolved at this level. When contacting our Customer Support team, please provide as much information as possible, including:

- your full name and account number;

- a clear description of the issue(s); and

- references to any additional relevant documentation, screenshots, etc.

Our Customer Support team will then endeavour to resolve your concerns as quickly as possible and propose a resolution to your case. If, after the resolution is provided, we do not receive any response from you regarding your interest in further escalating the matter, we will regard your concerns to be successfully resolved.

2. If you will remain dissatisfied after the resolution is offered you may contact us at complaints.eu@capital.com or complete the below form to submit your complaint to our Complaints Department who will be responsible to examine your complaint competently, diligently and impartially to assess whether the Company has acted fairly, within its rights and have met the Company’s contractual obligations.

To facilitate a thorough and independent investigation of your complaint, please ensure that you have provided all the relevant facts, supporting documents and evidence.

At this stage in order to resolve your complaint we will take the following steps:

(i) We will acknowledge, within five (5) days, receipt of your complaint and assign you with your Unique Reference Number. You should use said reference number in all future communication with us and/or the Financial Ombudsman of Cyprus regarding your complaint.

(ii) After thorough investigation, we will reply to your complaint within two (2) months, informing you about the outcome of our investigation. In our response we will review the relevant facts, findings and conclusions of our investigation and state whether your complaint has been upheld or rejected and, where appropriate, will offer redress and/or remedial action. If your complaint is rejected, we will explain the reasons for this.

In the event that we are unable to respond within two (2) months, due to the complexity of the complaint, we will inform you of the reasons for the delay and indicate the period of time within which it is possible to complete our investigation. This period of time shall not exceed three (3) months from the date of submission of the complaint.

3. Should you remain dissatisfied with our response, kindly note that you may refer your complaint to the Financial Ombudsman of the Republic of Cyprus, making reference to your unique reference number mentioned above. The contact details are the following:

Website: https://financialombudsman.org.cy/

Email: complaints@financialombudsman.gov.cy

Postal Address: P.O. Box: 2535, 1311 Nicosia, Cyprus

Telephone: +35722848900

Fax: +35722660584, +35722660118

It is important to contact the Financial Ombudsman within twelve (12) months of your complaint submission date otherwise the Financial Ombudsman of the Republic of Cyprus may not be able to deal with your complaint.

Please note that the Cyprus Securities and Exchange Commission (the “CySEC”) does not have restitution powers and therefore does not investigate individual complaints. However all complaints submitted to the CySEC are taken into consideration by the CySEC in the performance of its supervisory mandate.

Should you wish to inform CySEC about a complaint submitted to the Company, you may do so by making reference to your complaint unique reference number mentioned above. The relevant contact details are the following:

Website: http://www.cysec.gov.cy

Postal Address: P.O. BOX 24996, 1306 Nicosia, Cyprus

Telephone: +357 22506600

Fax: +357 22506700

Charges and fees

All charges and fees are documented and disclosed before any position is opened.

Account fees

Opening an account: NO FEE

Closing an account: NO FEE

Demo account: NO FEE

Deposits and withdrawal fees

Deposit fee: NO FEE

Minimum deposit: 20 USD/EUR/GBP or 100 PLN

For all payment methods,

except a wire transfer, which

has a minimum of 50 EUR (or equivalent in the currency

of your trading account)

Withdrawal fee: NO FEE

Minimum withdrawal: 20 EUR/USD/GBP for bank cards*

*The minimum you can

withdraw will vary depending

on your payment method

(check here for details).

If you have under the minimum withdrawal limit on your account,

you’ll only be able to withdraw your full balance.

Trading fees

CFDs

The spread: The spread is the difference between the buy and sell price of an instrument. It is the cost of executing a position.

Spreads are dynamic and adjust to underlying market conditions.

Trading commission: NO FEE

Overnight fee*: An interest adjustment applied when a position is held overnight.

*1:1 leverage (unleveraged) CFD positions are not subject to overnight funding, except on a limited number of markets.

The fee is paid or received depending on position direction.

Currency conversion: A conversion fee is payable on market denominated in a different currency to the trading account.

The same FX mark-up is applied when transferring funds between sub-accounts in different currencies.

0.7% of spot forex rate (retail clients)

0.5% of spot forex rate (Pro clients)

The fee is built into the exchange rate used for the conversion — not charged separately.

Guaranteed stop-loss orders (GSLs)*: A GSL closes a position at the price specified, eliminating slippage risk at execution. A fee applies when triggered.

The GSL fee varies by market, entry price and position size.

The fee is shown on the deal ticket before a position is opened. Details below.

Knock-outs

Knock-out distance: The knock-out distance is the cost of 1 knock-out option. The spread — the difference between the underlying market's buy and sell prices — is built into this distance.

Call options: market price — knock-out level

Put options: knock-out level — market price

Trading commission: No commission is charged on knock-out trades.

NO FEE

Knock-out fee:

The knock-out fee is reserved when a knock-out trade is opened. It functions as a guaranteed stop premium: maximum risk is fixed at entry. If the position closes without reaching the knock-out level, the fee is returned in full.

Calculated as a percentage of the trade's total exposure (underlying price × number of contracts).

Example (Germany 40 — major indices): Germany 40 is trading at €10,000. A Call knock-out is opened with a knock-out level at €9,900. The knock-out fee for major indices is 0.02% of notional value: €10,000 × 0.02% = €2.

Overnight funding adjustment:

An overnight funding adjustment applies when a knock-out position is held beyond the end of the trading day.

Currency conversion:

If the account's base currency differs from the currency of the underlying market, an FX conversion may apply when a position is opened or closed. This is separate from the knock-out fee. The prevailing platform exchange rate applies at the time of the transaction.

No FX conversion markup is charged on knock-out options at Capital.com.

The conversion rate is applied directly, with no markup added.

Spread fee

The bid-ask spread is the difference between the sell (bid) and buy (ask) price of an instrument. The ask price is always higher than the bid, meaning the market must move beyond the spread before a position turns positive.

Spreads reflect underlying market conditions, including supply, demand and liquidity. In more liquid markets, spreads tend to be narrower.

CFD spread example:

- 1 contract is held on the EU Stocks 50, quoted at 5200/5201.

- The spread is 1 point.

- Half the spread is paid on opening and half on closing. The total spread cost is €1 x 1 point = €1.

Overnight funding fee

When a position is held overnight, an interest adjustment applies. Whether this amount is paid or received depends on the position direction and the underlying rate. The calculation is based on defined rates and market factors, outlined in the examples below.

For most markets, a 1:1 leverage (unleveraged) CFD position will not incur an overnight funding fee. The following instruments are exceptions, where overnight funding applies regardless of leverage:

- Natural Gas

- US Cocoa

- Volatility Index (VIX)

- Forex pairs with Turkish Lira (TRY)

Indices

Formula: Our daily fee +/- Interest-rate benchmark

The benchmark* tracks the currency of the underlying market. USD-denominated indices use SOFR. GBP-denominated indices use SONIA.

Our daily fee is 4% per year. The annual rate is divided by 360 or 365 days depending on the currency convention:

GBP, CAD, SGD and similar currencies: 4% / 365 = 0.01096% per day USD, EUR, CHF, JPY and similar currencies: 4% / 360 = 0.01111% per day

The divisor matches the day-count standard applied in each currency's market.

*The relevant interest-rate benchmark already includes an underlying spread adjustment. This is reflected within the published rate (for example, SOFR or SONIA).

CFD example

- 0.6 contracts are held on the US Tech 100, priced at 20,140. Total exposure is $12,084.

- The US Tech 100 is denominated in USD. The relevant benchmark rate is SOFR, assumed here at 5.01448% annually, or 0.01393% daily.

- The platform daily fee is 0.01111%.

- For a long position: 0.02504% (SOFR + platform fee) = $3.03 paid.

- For a short position: 0.00282% (SOFR − platform fee) = $0.34 received.

Commodities

Formula: Our daily fee (0.01096%) +/- Daily Premium Adjustment (futures basis)

The Daily Premium Adjustment on spot commodities isn't a charge or fee but rather a price rollover which exists independently of the administrative fee. Because spot commodity prices are based on futures contracts that expire and get replaced by new ones, this adjustment keeps your position's price continuous as we move from one contract to the next. Depending on which way you're trading, it may show as a small credit or debit, but it has no net impact on your overall P&L. You can find more information here.

CFD example

- 200 barrels of Crude Oil are held, priced at $57.86. Total exposure is $11,572.

- The overnight basis adjustment for Crude Oil is currently 0.031. At the prevailing spot price of 57.86 that equates to 0.05358% daily.

- The platform daily fee is 0.01096%.

- For a long position: 0.06454% (platform fee + basis adjustment) = $7.47 paid.

- For a short position: 0.04262% (platform fee - basis adjustment) = $4.93 received.

Forex

Formula: Our daily fee (0.00411%) +/- Underlying market adjustment (TomNext)

The TomNext rate reflects the overnight interest rate differential between the two currencies in the pair.

CFD example

- A position of $10,000 is held on USD/JPY.

- The overnight swap (TomNext) rate for USD/JPY is currently -0.0182. At the prevailing spot price of 132.80 that equates to -0.0137% daily.

- The platform daily fee is 0.00411%.

- For a long position: 0.00959% (platform fee + swap rate) = $0.96 received.

- For a short position: 0.01781% (platform fee - swap rate) = $1.78 paid.

Shares

Formula: Our daily fee +/- Interest-rate benchmark

The benchmark tracks the currency of the underlying market. USD-denominated shares use SOFR. GBP-denominated shares use SONIA.

Our daily fee is 4% per year. The annual rate is divided by 360 or 365 days depending on the currency convention:

GBP, CAD, SGD and similar currencies: 4% / 365 = 0.01096% per day USD, EUR, CHF, JPY and similar currencies: 4% / 360 = 0.01111% per day

The divisor matches the day-count standard applied in each currency's market.

The relevant interest-rate benchmark already includes an underlying spread adjustment. This is reflected within the published rate (for example, SOFR or SONIA).

CFD example

- A position equivalent to 50 shares in Tesla is held, priced at $252. Total exposure is $12,600.

- Tesla trades in USD. The relevant benchmark rate is SOFR, assumed here at 5.01448% annually, or 0.01393% daily.

- The platform daily fee is 0.01111%.

- For a long position: 0.02504% (platform fee + SOFR) = $3.16 paid.

- For a short position: 0.00282% (platform fee - SOFR) = $0.36 received.

Crypto

Formula: Fixed overnight funding rates apply to Bitcoin and Ethereum CFDs.

Long positions pay 0.06164% daily (22.5% annually).

Short positions receive 0.0137% daily (5% annually).

Rates do not vary by benchmark and are not linked to an external interest-rate index.

CFD example

- 1 CFD on Bitcoin is held overnight, with a closing mid price of $50,000.

- The applicable overnight funding rate for Bitcoin and Ethereum CFDs is 0.06164% daily for long positions and 0.0137% daily for short positions.

- For a long position: 0.06164% of ($50,000 x 1) = $30.82 paid.

- For a short position: 0.0137% of ($50,000 × 1) = $6.85 received.

Bonds/Interest rates

Formula: Our daily fee +/- underlying market adjustment (futures basis)

Our daily fee is 0.01096%. The futures basis adjustment reflects the cost of rolling a bond futures position overnight and varies by instrument and prevailing market conditions.

CFD example

- A position on the US 10-Year T-Note CFD is held, priced at $112.50 per 100 face value. Total exposure is $200,000.

- The overnight basis adjustment is -0.0008. At a price of 112.50 that equates to (-0.0008 / 112.50) x 100 = -0.0711% daily.

- The platform daily fee is 0.01096%.

- For a long position: 0.01096% - 0.0711% = -0.06014%. Funding = $200,000 x -0.06014% = $120.28 received.

- For a short position: 0.01096% + 0.0711% = 0.08206%. Funding = $200,000 x 0.08206% = $164.12 paid.

Guaranteed stop-loss fee

A standard stop-loss order closes a position at a specified level. It is not guaranteed to execute at exactly that price — during a market gap, execution may occur at the next available price. Slippage can occur in volatile or low-liquidity conditions.

A guaranteed stop-loss order (GSL) closes a position at exactly the specified price, regardless of slippage or market gaps. A fee — the GSL premium — applies if the order is triggered.

The GSL fee is calculated using three components: the guaranteed stop premium (percentage), the position's open price, and the quantity.

GSL fee = GSL premium × position open price × quantity

The applicable GSL fee is shown on the deal ticket when a GSL is selected.

Currency conversion fee

Applies when a transaction is in a different currency to the account's base currency.

Applies to:

- Realised profit and loss

- Overnight funding adjustments

- Guaranteed stop-loss order fees

- Dividends

- Standalone currency conversions (manual conversions of account balance)

Example — closing a trade

- Account currency: EUR. US stock trade closed with a profit of $11.30.

- At spot rate (1.1300): €10.00

- At all-in rate including 0.7% fee (1.1379): €9.93

- Conversion fee: €0.07

Example — overnight funding adjustment

- US stock position. Overnight funding adjustment of -$4.00 applied in USD.

- At spot rate (1.1300): €3.54

- At all-in rate including 0.7% fee (1.1221): €3.57

- Conversion fee: €0.03

The all-in exchange rate used for each conversion is visible in the Reports section and when closing a position.

Knock-out fee

Knock-out options are available in selected countries only. The knock-out fee is reserved at the point of opening a knock-out trade. It functions as a guaranteed stop premium: the maximum risk on the position is fixed at the moment of entry.

If the position closes without reaching the knock-out level, the fee is returned in full.

The fee is calculated as a percentage of the trade's total exposure (underlying price × number of contracts).

Example – Germany 40, major indices

- Germany 40 is trading at €10,000.

- A Call knock-out is opened with a knock-out level of €9,900.

- The knock-out fee for major indices is 0.02% of notional value: €10,000 × 0.02% = €2.

Markets Pricing

How our markets are priced

CFDs are priced differently depending on various factors. Here, we’ll run through how we price our markets by asset class, detailing the way in which prices are derived from those of exchanges and other institutions.

Cryptocurrencies

We derive our cryptocurrency prices by taking sell and buy prices from various well-known cryptocurrency exchanges. We then aggregate these prices to give us a consolidated mid-price which we then use to wrap our own spread around. This provides a much more stable spread through different times of the day.

Example

Let's look at how we price Bitcoin (BTC) at a hypothetical point in time.

We draw on current pricing from three exchanges of $99,500/$99,700, $99,550/$99,750, and $99,520/$99,720. Then, we calculate the mid-prices and aggregate them for a price of $99,623.

To this price, we apply a spread of $200* to make the Capital.com price $99,523/$99,723.

Shares

For our shares pricing, we take the underlying exchange sell and buy prices of each stock and then apply a markup to these prices. This means you’re trading on the ‘true’ prices from the underlying market with just a small adjustment for our fee. It also means our price will reflect fluctuations in the underlying market spread due to changes in liquidity.

Example

- Let’s say one physical stock in the underlying market has a sell price of $99.95 and a buy price of $100.05.

- When you trade the stock with us as a derivative (EG CFD), we’ll apply a fixed markup to this price of $0.05 either side, making our sell price $99.90 and our buy price $100.10. This means our spread is 0.20.

- If the underlying market widens to 99.80/100.20, our fixed markup of 0.05 makes our price 99.75/100.25. This means our spread is now 0.50.

Forex and spot metals

Unlike the rest of our offerings, spot forex and metals are not traded on a centralised exchange in the underlying market. This means there’s no central reference point for brokers to derive their price from and so typically prices are calculated through a range of OTC (over-the-counter) counterparties. These can range from investment banks to other brokers.

These prices are subject to variable spreads depending on market conditions. At Capital.com, we aggregate them and subsequently add a small additional spread (our transaction fee) depending on the market.

Example

- Let’s look at how we price EUR/USD at a given point.

- We aggregate pricing from three counterparties of 1.12345/1.12355, 1.12350/1.12360, and 1.12348/1.12358, for a consolidated price of 1.12348/1.12358.

- To this price, we apply a spread of (EG), 0.00006 to make the Capital.com price 1.12345/1.12361.

Indices

Our cash index pricing is derived from our price providers’ mid-price and subtracting/adding spread.

We fix our index spreads based on times throughout the day, usually to reflect changes in the underlying liquidity of the market. Our spread will typically be widest when the underlying futures market is closed, and tightest during the main share-trading session.

As cash indices are tradeable in the underlying market.Many price providers, including ours, will derive their cash price by taking the futures price and adjusting for fair value, which is expected dividends of the constituent stocks and the relevant market interest rates.

Fair value represents what the index should be worth in a perfect market without arbitrage opportunities.

Commodities and the VIX index

You can trade on both commodity spot prices (also sometimes called ‘undated commodities’) and commodity futures with us.

How we price commodity futures markets

We price our commodity futures by adding our spread to the underlying market price. The price you trade at already includes the spread.

Spreads can change. Please check individual market details in the app or web platform for the latest figures.

The exchanges that we source our commodity futures prices from are:

- Brent Oil: ICE Futures Europe

- Carbon Emissions: ICE Futures Europe

- Crude Oil: New York Mercantile Exchange (NYMEX)

- Cocoa US: ICE Futures US

- Natural Gas: New York Mercantile Exchange (NYMEX)

All contracts expire at specified future dates and are cash-settled, so you’ll never take delivery of a commodity.

How we price commodity spot markets

We determine prices for our spot commodity markets using the two nearest futures contracts of a commodity, as these are usually the most traded.

Over time, our undated price gradually shifts from the price of the nearest contract to the next one to avoid the need for an expiry date (sometimes called a rollover date).

In our system:

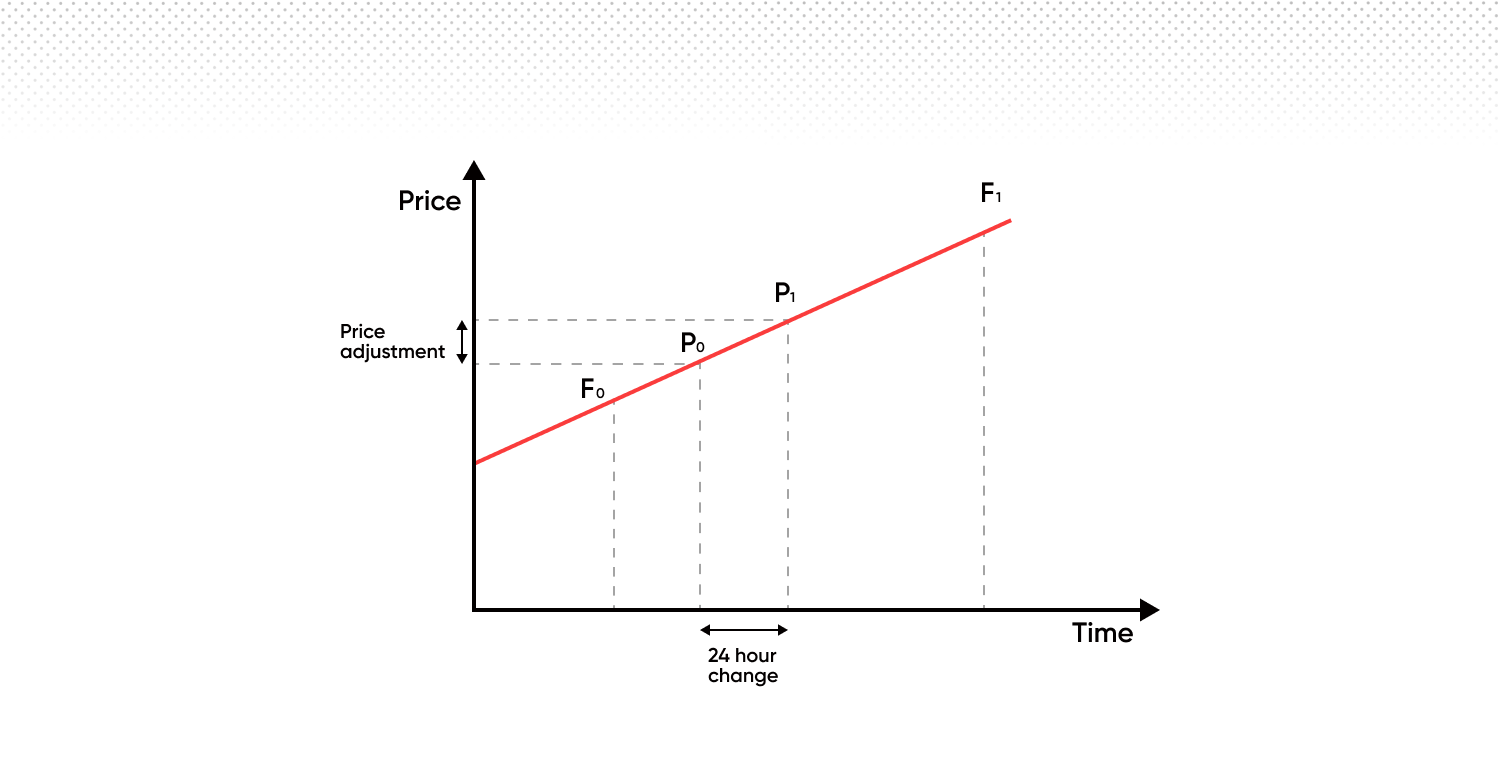

- The ‘front month contract’ (the one that expires soonest) is called ‘A’.

- The ‘back month contract’ (the one that expires second soonest) is called ‘B’.

- Our price (P0 and P1 in the diagram below) gradually moves from the price of ‘A’ towards the price of ‘B’ between these two expiry points.

- The price of ‘B’ can be higher or lower than the price of ‘A’, though in the example below, it’s higher.

When the front month contract ‘A’ expires, we transition to the next set of contracts. This means ‘B’ becomes the new ‘A’, and the contract that expires after the new ‘A’ becomes the new ‘B’. This process continues, so there is always a smooth transition from one contract to the next.

This means that when we transition, our pricing will be based 100% on the front month contract, and then move in a linear fashion towards the back month.

When holding positions overnight, the following applies:

Administrative fee (overnight holding fee)

This is a fixed fee of 0.01096% charged daily for maintaining an open position overnight.

Daily Premium Adjustment

The Daily Premium Adjustment applied to spot commodity positions is not a fee or charge, and exists independently of the administrative fee. It is a pricing adjustment that reflects the daily movement of our price from the front-month futures contract ('A') to the next contract ('B').

Its purpose is to ensure that the price of spot commodity instruments remains continuous over time by reflecting changes in the underlying futures curve, and has a neutral overall impact on your P&L.

Depending on the direction of your position, this adjustment may result in either a credit or a debit to your account.

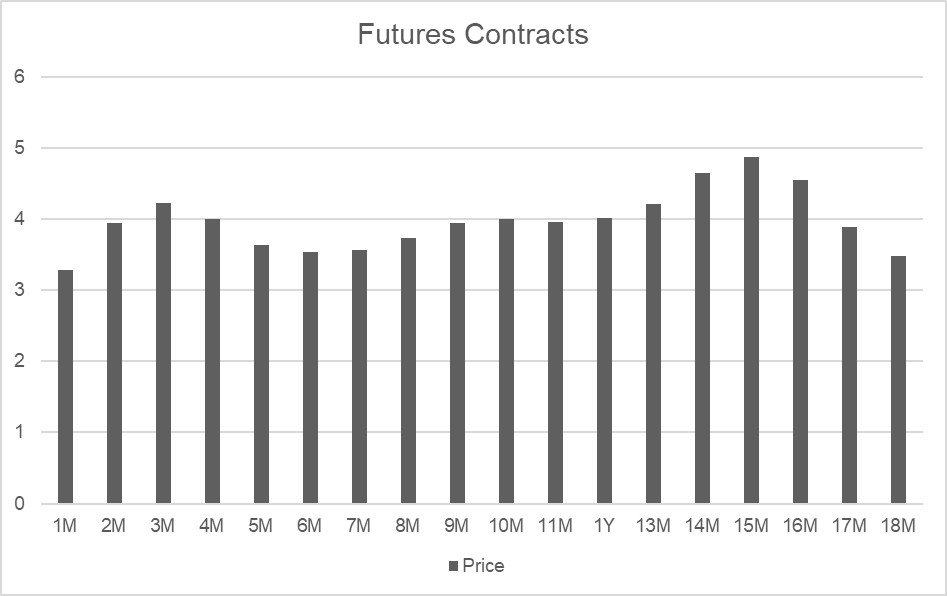

Here's an example using real prices for Natural Gas, a commodity with different prices for contracts expiring each month in the future. You can see a relative change in the value of each monthly contract in the second chart. These changes are due to seasonal supply and demand, not market expectations of future prices. In other words, Natural Gas typically costs more to buy in winter than in summer.

Comparing Month 2 and Month 3, we can see there is a large difference in prices (known as ‘fair value’):

| Expiry Date | Period | Price |

|---|---|---|

| 30 Days | 2M | 3.938 |

| 64 Days | 3M | 4.221 |

| Difference | 0.283 |

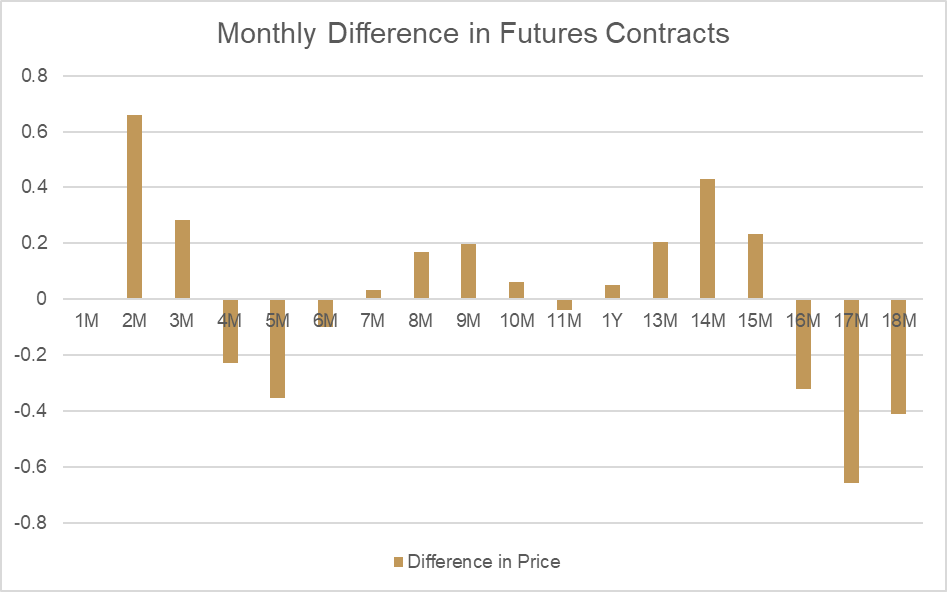

If we look at how this price changes per day between these two points, we can calculate the fair value adjustment that would be applied as a Daily Premium Adjustment. As Month 2 is lower than Month 3, the valuation price of the spot commodity will naturally rise each day in line with the change in fair value.

To offset this impact on open positions, an equivalent adjustment is subtracted from accounts holding long positions. For short positions, the same amount is credited. The overall effect of the fair value adjustment on both the valuation price and the account balance is zero.

| No. of Days | Change per Day |

|---|---|

| 34 | 0.00832 |

| Long Result | Amount |

|---|---|

| P/L | 0.00832 |

| Adjustment | -0.00832 |

| Net effect | 0 |

| Short Result | Amount |

|---|---|

| P/L | -0.00832 |

| Adjustment | 0.00832 |

| Net effect | 0 |

The Daily Premium Adjustment is necessary to reflect changes in fair value, and we apply the updated fair value each day just before the closing time for trading in each commodity. You can see the effect of the new fair value applied to a spot commodity directly on the platform charts, as shown in the example below.

The Daily Premium Adjustment is not a cost or fee – it’s an adjustment that keeps your P&L unaffected by day-to-day changes in fair value for spot commodity positions.