FOMC preview: Still expecting three rate cuts in 2024?

The Federal Reserve is expected to keep its policy unchanged on Wednesday – data from Reuters shows a 99% chance of no change. Last week’s 25-basis-point rate cut from the ECB has done nothing to change market expectations, and why should it?

All price information and forecast data in this article are sourced from Reuters, FX street

The Federal Reserve is expected to keep its policy unchanged on Wednesday – data from Reuters shows a 99% chance of no change. Last week’s 25-basis-point rate cut from the ECB has done nothing to change market expectations, and why should it? The latest data released on Friday shows the US labour market remains tight; more jobs were added and wages rose again in May.

Alongside the labour market, the Federal Reserve has also been closely monitoring how inflation evolves to make its decision. Consumer prices (CPI) rose 3.4% in the 12 months to April, a marginal drop from 3.5% in the previous month. The May CPI will be released just hours before the FOMC meeting on Wednesday evening. Analysts estimate the reading to remain unchanged at 3.4%, and core inflation to drop slightly from 3.6% to 3.5%.

It is unlikely that this data will impact the decision. By then, FOMC members will already have made up their minds – which, according to markets, is to keep rates unchanged at the current range of 5.25%-5.5%. The fact that average hourly earnings for May came in higher than expected and above the previous month was enough to confirm that rates need to remain restrictive for longer. But markets want to know for how long. Current pricing shows a 47% chance that rates could be cut 25bps in September, but that could easily change. Jerome Powell’s press conference on Wednesday will be heavily scrutinised for any clues on timing, but he is unlikely to give any and just continues to reiterate that the Federal Reserve remains data-dependent, and so far it shows little signs of allowing a rate cut.

The meeting on Wednesday will be accompanied by an update to the economic projections and a dot plot chart of how FOMC members expect the Fed Funds Rate to evolve. The last time we saw updated projections was in March. Back then, the takeaway from the Fed meeting seemed dovish at first given the majority of the FOMC members continued to expect three rate cuts this year, but it told a different story upon closer examination.

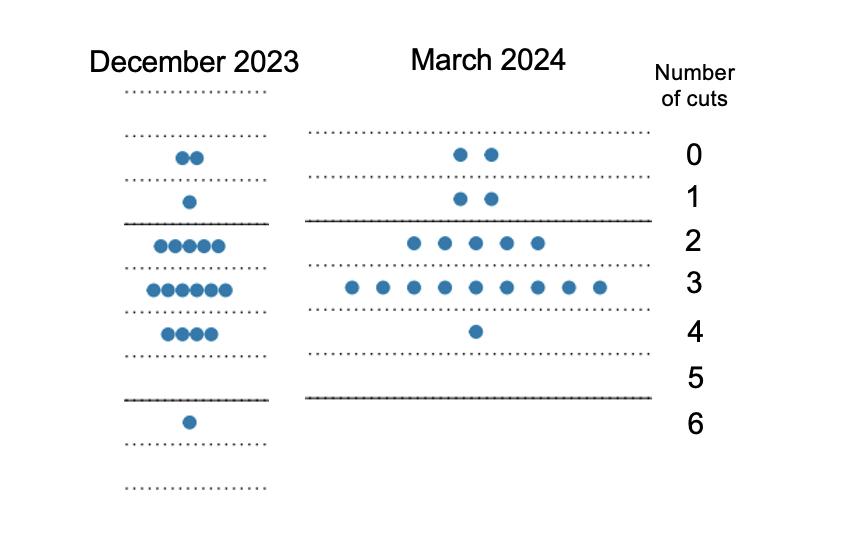

Dot-plot projections for March 2024 vs December 2023

(Past performance is not a reliable indicator of future results)

(Past performance is not a reliable indicator of future results)

As can be seen in the image above, whilst the median remained at three rate cuts, the March dot plot was more hawkish than the December one. In December, five FOMC members were expecting more than three cuts in 2024, and that was reduced to just one in March. Moreover, in the March reading four members expect fewer than two cuts in 2024, versus three members back in December. If, and how, the dots change in the June projections will likely impact markets. If more members expect two or fewer rate cuts in 2024, then we could see a hawkish reaction in markets; the dollar up and equities down.

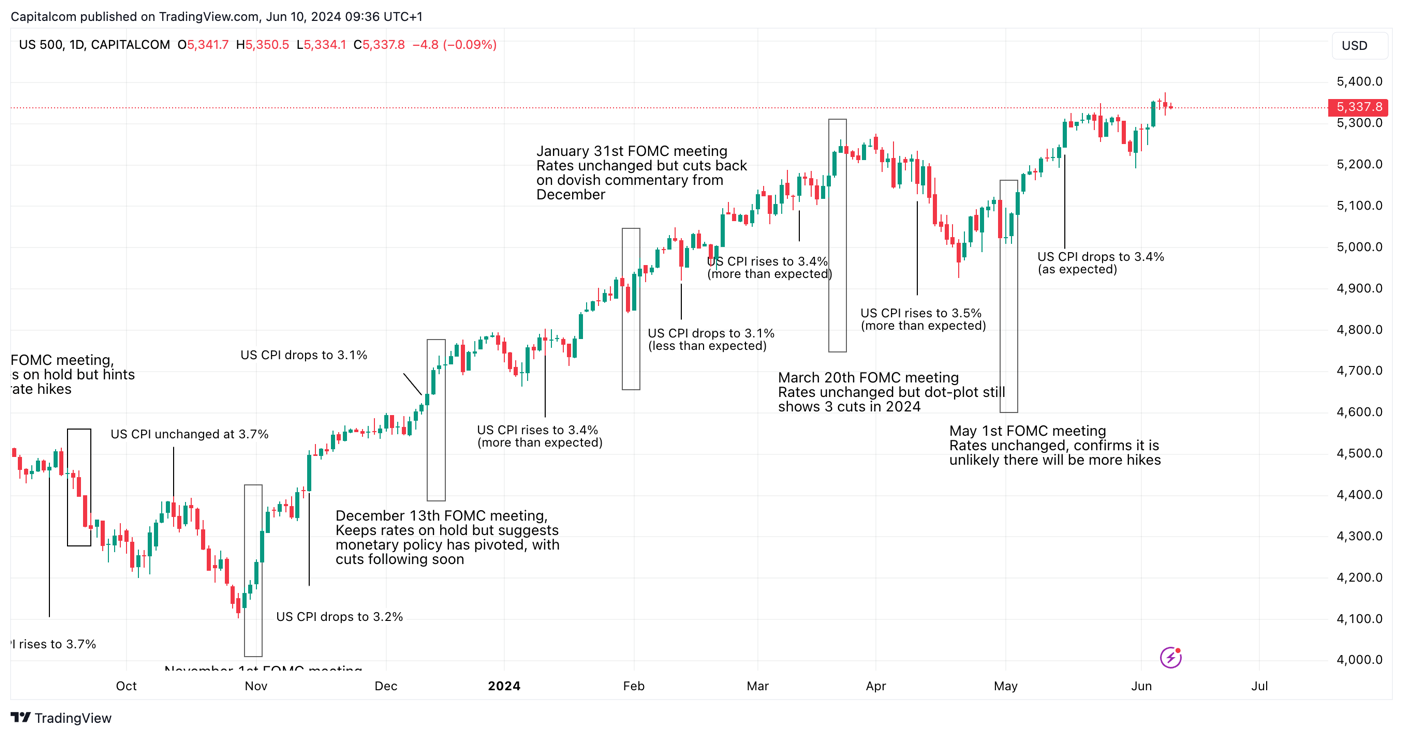

Furthermore, if the CPI comes in higher than expected, the market could already be prepped for a risk-off move before the meeting. The stronger jobs data on Friday has already caused US equities to pull back from recent highs. The S&P 500 is showing a bearish bias this week, but traders are being cautious not to take up big positions before the meeting just in case. A drop below 5,200 could be on the cards for this week if the CPI data and FOMC meeting cause markets to price in higher rates for (even) longer.

S&P 500 daily chart

(Past performance is not a reliable indicator of future results)

(Past performance is not a reliable indicator of future results)

Meanwhile, the US dollar jumped higher on Friday after the stronger jobs data, reinforcing the view that stronger economic data and a more hawkish Fed remain supportive of the US currency. The momentum has been mostly bearish in the past two months, but we could see a bullish reversal underway if the events play in favour of risk-off sentiment this week. The US dollar index could attempt to break above 105 for the first time since May 9th before consolidating higher.

Learn how to trade the US Dollar index (DXY)

US dollar index (DXY) daily chart

(Past performance is not a reliable indicator of future results)

(Past performance is not a reliable indicator of future results)